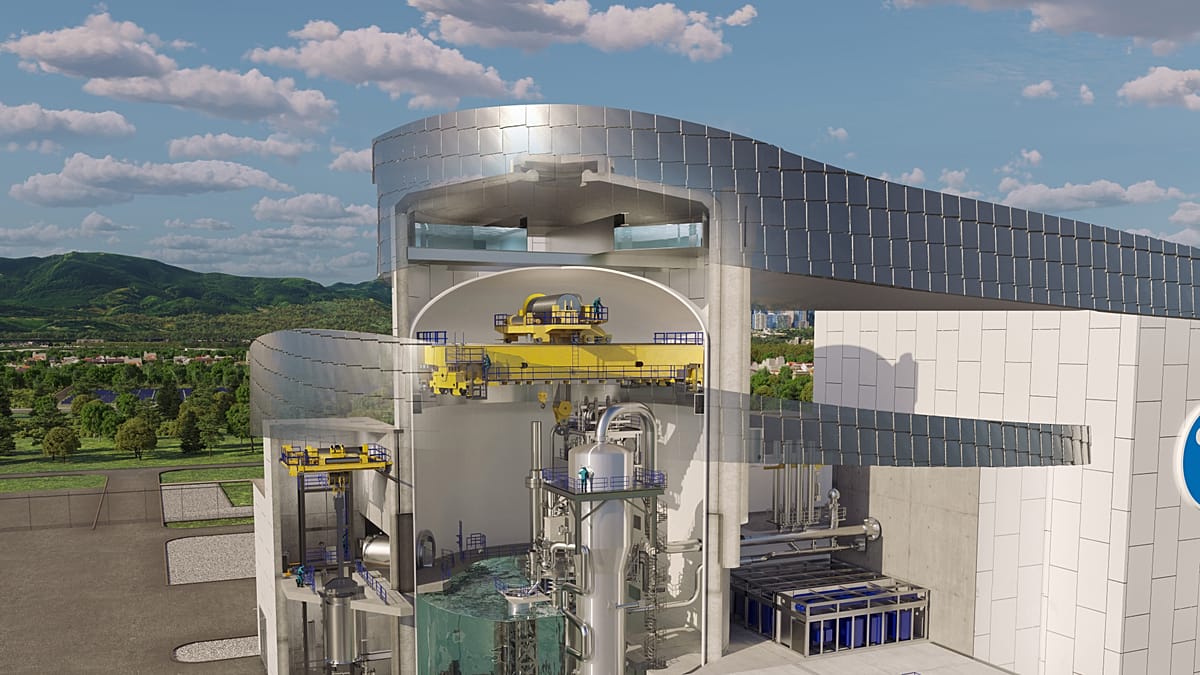

The European Commission unveiled a €200 million guarantee to de-risk private investment in small modular reactors (SMRs) as part of a push to roll out SMRs by the early 2030s; nuclear’s share of EU electricity has fallen from ~33% in 1990 to ~15% today. Eleven EU countries backed a 2024 declaration and several commercial partnerships (CEZ–Rolls‑Royce SMR; Orlen–Synthos) are already under way, signaling potential sector-level investment and industrial activity. Significant political and NGO opposition, legal bans in countries like Ireland, and calls that the plan is vague introduce implementation risk and the possibility resources could be diverted from cheaper renewables and storage solutions.

The shift toward modular nuclear is more an industrial policy program than a short-term power-market event. Serialised factory production will create multi-year capacity bottlenecks in reactor-grade forgings, specialty steel, and modular assembly yards; suppliers who secure early certification and tool-up will enjoy 3–5 year pricing power and multi-decade annuity-like revenues, while late entrants face multi-year lead times to catch up.

Finance is the linchpin: higher-for-longer rates make large, up-front capex unattractive absent government guarantees or long-term contracts. Public de-risking signals shorten the financing runway for bidders but are unlikely to cover the full funding gap; therefore winners will be those with utility balance sheets or access to export-credit / ECA-type facilities, not pure-project developers or firms reliant on merchant power sales.

Policy fragmentation and export nationalism will concentrate value in a few engineering and fabrication hubs, creating clear winners among certified OEMs and chronic underutilisation risk for some national supply chains. Near-term market-moving catalysts are regulatory design certification, first-of-a-kind construction starts, and named long-term industrial offtakes; absence of those milestones inside 12–36 months materially raises execution risk and downside for equities exposed to SMR buildout expectations.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.05