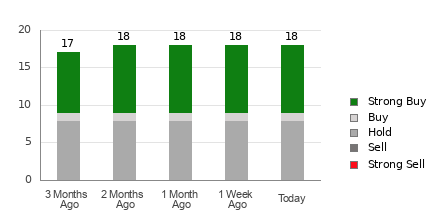

Duolingo (DUOL) currently holds an Average Brokerage Recommendation (ABR) of 1.94, approximating a 'Buy' consensus from 18 firms. However, the article advises investors to exercise caution, noting that ABRs often exhibit a significant positive bias due to brokerage firms' vested interests, making them less reliable for predicting stock movements. Conversely, Duolingo's Zacks Consensus Estimate for the current year recently declined 0.9% to $2.9, resulting in a Zacks Rank #4 (Sell), a quantitative measure based on earnings estimate revisions. This divergence suggests that despite the favorable ABR, the downward revision in earnings estimates indicates potential near-term price weakness for DUOL, underscoring the importance of scrutinizing such recommendations.

A significant divergence exists between Wall Street's qualitative recommendations and quantitative earnings-based indicators for Duolingo, Inc. (DUOL). While the company holds a 'Buy'-equivalent Average Brokerage Recommendation (ABR) of 1.94, derived from 18 firms where over 55% rate it as a 'Strong Buy' or 'Buy', this positive sentiment is directly challenged by deteriorating earnings prospects. Specifically, the Zacks Consensus Estimate for DUOL's current-year earnings has declined by 0.9% over the past month to $2.9 per share. This downward revision, reflecting a strong agreement among analysts, has triggered a Zacks Rank of #4 ('Sell'). The analysis highlights that such earnings estimate revisions have historically shown a stronger correlation with near-term stock price movements than ABRs, which are often subject to an inherent positive bias. Therefore, the recent negative trend in earnings expectations suggests a tangible risk of underperformance for DUOL in the near term, despite the favorable sell-side ratings.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately negative

Sentiment Score

-0.60

Ticker Sentiment