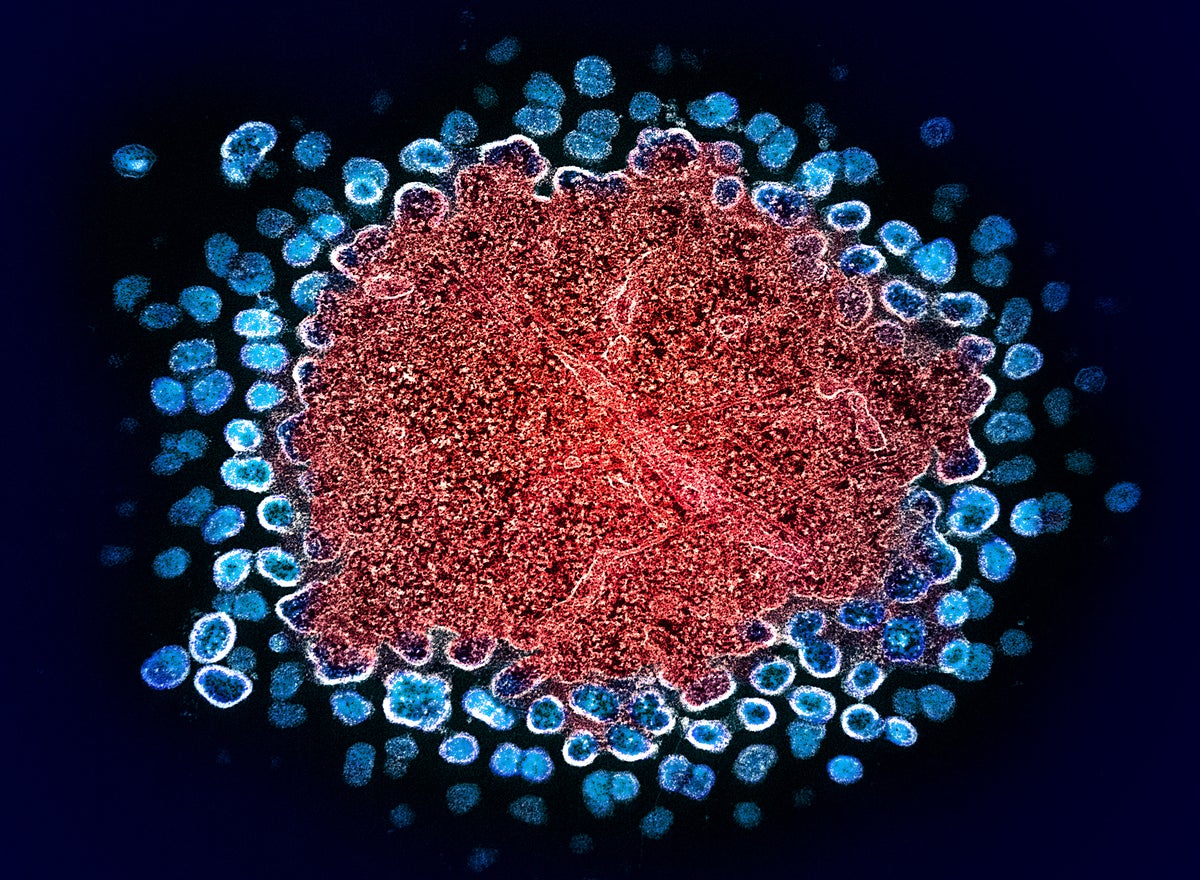

A 63-year-old man was functionally cured of HIV after a bone marrow transplant from his brother, whose CCR5Δ32 mutation confers resistance to HIV-1. Researchers found no detectable HIV in blood, gut tissue, or bone marrow after the transplant, and his healthy T-cell levels remained stable after stopping ART two years later. The result is a notable scientific advance, but it is not broadly applicable yet because bone marrow transplants remain high-risk and are generally reserved for patients needing them for other medical reasons.

This is directionally bullish for the gene-editing, cell-therapy, and transplant-enabling ecosystem, but the market should resist the temptation to extrapolate a one-off biologic cure into a near-term commercial HIV franchise. The real economic signal is not the cure itself; it is validation that complete immune-system replacement plus CCR5-pathway resistance can eliminate the reservoir when engraftment is sufficiently deep across blood, marrow, and gut. That strengthens the long-duration option value of ex vivo gene editing, in vivo delivery, and transplant conditioning technologies, especially any platform that can reduce the toxicity of myeloablation or improve homing/engraftment fidelity. Second-order, this reinforces a bifurcation in HIV care: curative interventions remain medically exceptional and procedure-intensive, while ART remains the dominant cash-flow engine. That is mildly negative for any investor narrative betting on a rapid erosion of chronic HIV drug sales; the adoption curve for curative transplant-like approaches will be constrained by oncology-style risk tolerance, specialized centers, and donor/conditioning limitations for years. The commercial upside is more likely to accrue to adjacent tools: diagnostics to detect ultra-low residual disease, immune monitoring, conditioning regimens, and cell-processing/manufacturing platforms. The main contrarian risk is that enthusiasm overstates addressable market timing. If a cure requires marrow ablation-level toxicity, payer willingness and physician adoption stay narrow unless safety drops dramatically or the procedure is reserved for patients with co-morbid malignancy. Any disappointment in durability, incomplete reservoir clearance, or graft-versus-host complications would quickly compress the halo effect around the space. Near term, this is a sentiment catalyst for biotech multiples rather than a fundamental earnings event; the actionable question is which enabling names get re-rated before clinical proof broadens.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.85