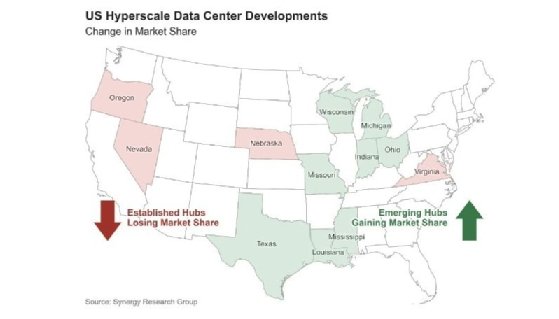

US datacentre construction is shifting toward central states, with Synergy citing 437 proposed US sites and Texas emerging as the main beneficiary of abundant power and faster grid connections. Virginia is expected to retain its lead as 'datacentre alley,' while Oregon and Nevada are likely to lose share due to grid constraints, tax changes and environmental restrictions. The article points to a broader move toward gigawatt-scale AI campuses, especially in Texas and the Midwest.

The key trade is not “more datacentres” but a regional re-rating of the entire compute supply chain. Capital is migrating toward places where power interconnection, land, and permitting can support faster time-to-capacity, which should favor utilities, transmission owners, gas-fired generation, switchgear, cooling, and fiber buildout in the central US over coastal infrastructure names. The second-order effect is that the bottleneck shifts from silicon demand to site-level execution: whoever can secure grid access and water-light cooling wins, while everyone else gets pushed into longer-dated projects and lower utilization.

The market is likely underappreciating how uneven the beneficiary set is. Hyperscalers with balance-sheet flexibility can arbitrage geography; smaller operators and pure-play datacentre REITs without embedded power relationships risk margin compression as customers increasingly demand delivered megawatt capacity rather than rack space. For the listed names here, the clearest upside is in the operators that can monetise AI demand via owned infrastructure and long-duration contracts, while the biggest hidden loser may be any platform forced to lease into congested legacy hubs at rising power costs.

The contrarian angle is that this is less a broad “AI is bullish” signal than a dispersion trade within infrastructure. If Texas and the Midwest become the default build zones, grid and cooling equipment shortages could create 12-24 month delays, making near-term revenue recognition volatile even as multi-year demand remains intact. Conversely, policy resistance in coastal states could accelerate relocations faster than consensus expects, pulling forward capex for the large cloud platforms and delaying returns for dependent local landlords.

Tail risk: any step change in utility interconnection timelines, water regulation, or a regional power price spike could pause the migration for 6-18 months; the bullish thesis only holds if low-latency power access remains the binding constraint. Near term, the move is more supportive for capital goods and power than for pure datacentre occupancy economics.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.10

Ticker Sentiment