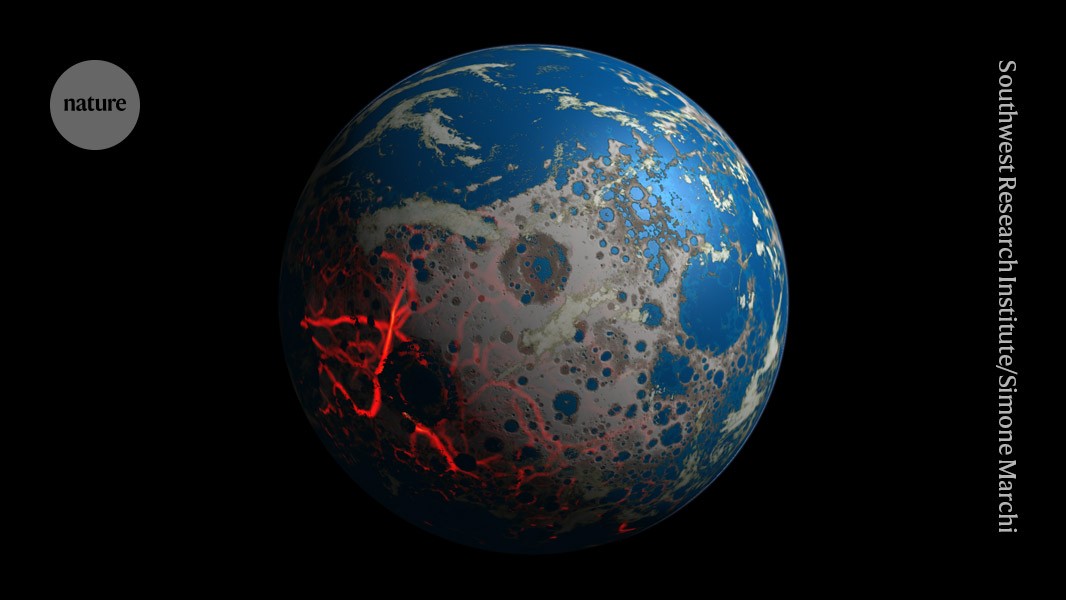

Researchers led by Shane Houchin analyzed zircon crystals from the Jack Hills (Western Australia) using advanced X‑ray techniques at Argonne’s Advanced Photon Source and report more oxidized uranium in crystal rims, which the authors interpret as evidence for higher oxygen levels and active plate tectonics by at least ~3.3 billion years ago. The finding, published in PNAS, suggests earlier redox conditions and potential for greater habitability on early Earth, though other geochemists caution that alternative magmatic processes could produce the observed uranium oxidation.

Market structure: This paper mostly benefits makers of high-end analytical instruments (X‑ray, mass spec, detectors), national lab operators and specialist geoscience service firms because it validates demand for more high-resolution rock chemistry work; incumbents with unique IP (Thermo Fisher TMO, Bruker BRKR, Agilent A) can sustain 5–10% pricing power on premium services for 12–36 months. Miners/explorers (small-cap juniors) are neutral-to-negative because academic advances reduce speculative ‘new model’ narratives that drive exploration speculation; no meaningful immediate change to commodity supply/demand is signaled.

Risk assessment: Tail risks include a methodological refutation or major budget cuts to DOE/NSF (low probability, high impact) — a 20–30% cut to user‑facility funding would materially reduce instrument order flow. Immediate (days) market effect: none; short term (3–6 months): increased interest from research customers and modest revenue reacceleration for instrument makers (+3–7% rev growth vs. baseline if follow‑on studies materialize); long term (12–36 months): structural uplift in capital spending on lab upgrades if governments/industry allocate >$200–$500M to geoscience programs.

Trade implications: Favor small, conviction-weighted long exposure to instrument leaders and services (see decisions) with tight stops; avoid/trim small-cap exploration miners (GDXJ) by ~30% within 30 days. Use 6–12 month call spreads on BRKR/TMO to capture catalytic earnings beat risk while limiting premium outlay; hedge with 6–9 month puts if R&D funding headlines turn negative.

Contrarian angles: Consensus will underprice the incremental recurring revenue from service/consumable sales attached to advanced analyses — this is more durable than one‑off grants. Risk of overreaction is moderate: if Chinese OEMs gain share and compress margins by >150–200 bps over 12 months, upside will be capped; monitor gross margin moves (trigger: >100 bps decline QoQ).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00