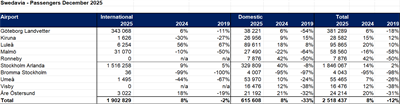

Swedavia reported continued recovery in air travel with December passenger volumes up 8% year‑on‑year to about 2.5 million and full‑year 2025 traffic rising 2% vs. 2024. Stockholm Arlanda led growth, with roughly 1.8 million December passengers (+14% y/y), full‑year passenger traffic up just under 7%, international traffic up ~3% and domestic at Arlanda up nearly 29% year‑on‑year; Göteborg Landvetter saw modest gains (~+2% full year). The network expanded with 37 new scheduled routes, eight new airlines and five charter destinations, while freight volumes rose ~5%, signaling strengthening demand toward pre‑2019 international levels and supporting near‑term revenue and capacity planning for airlines and airport operations.

Market structure: December +8% YoY (full-year +2%) with Arlanda driving most gains (Arlanda +7% FY, domestic +29% at Arlanda) shifts profits toward airport operators, lessors and premium long-haul carriers serving Stockholm. Winners: airports (stable fee streams, ancillary revenues) and lessors (higher utilization); losers: marginal regional carriers with weak pricing power. Cross-asset: higher jet-fuel demand implies modest upward pressure on crude (positive for energy equities/commodities), and a cyclical uplift that favors cyclicals vs long-duration sovereign bonds. Risk assessment: Tail risks include pandemic resurgence, strike/regulatory action (airport environmental limits/slot reallocations) and airline credit stress; each could reverse flows within weeks and hit airlines harder than airports. Short-term (days–months): volatility around monthly traffic prints and winter seasonality; medium/long-term (3–24 months): route network durability and macro growth. Hidden dependencies: route additions concentrate at Arlanda (concentration risk) and airline financials determine whether traffic converts to operator profit. Trade implications: Favor balance-sheet-strong, cash-generative airport operators and lessors over small carriers. Use ETF/lessor exposure for broad capture (lower idiosyncratic risk). Entry: scale into positions now, add on >5% pullback or if two consecutive monthly prints stay ≥+3% YoY; target horizon 6–18 months. Options: use call-spreads to limit premium spend around quarterly prints. Contrarian angle: Consensus will overweight airlines — missing that airports/lessors monetise traffic more defensibly and benefit from ancillary growth; airline margin squeeze from fuel/competition is underappreciated. Historically (post-2010 recoveries) airports outperformed carriers by 10–25% over 12 months; unintended consequence: capacity growth could depress fares, making airline equities the more fragile lever.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35