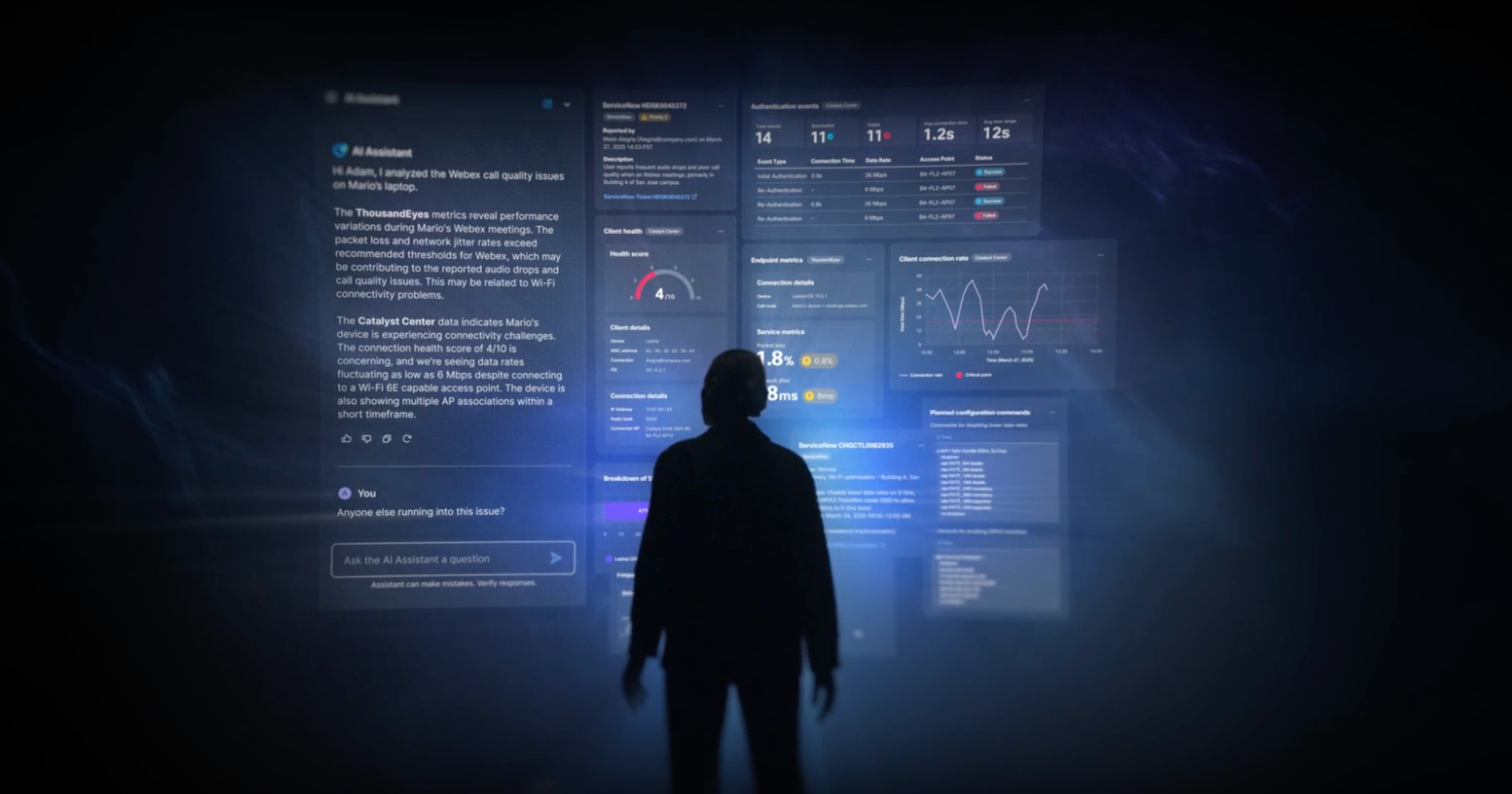

At Cisco Live EMEA, Cisco expanded its AI-Ready Secure Network Architecture by broadening AgenticOps across its networking portfolio, launching IOS XE 26 with full-stack post-quantum cryptography (NIST-approved), and introducing new hardware including the Cisco 8100 Series Secure Routers and a Campus Gateway for mid-sized sites. Collaboration and edge offerings were also upgraded — notably the Room Kit Pro G2 (with NVIDIA delivering ~25x more AI processing) and new Webex AI features (real-time Translator Agent, AI Routing, AI Forecasting) — alongside deployment options for sovereign and air-gapped environments via UCM 16, Webex Calling Hybrid, and Cisco AI Pod. These moves aim to drive enterprise upgrade cycles around AI-enabled networking and security, strengthen Cisco’s positioning in regulated/sovereign deployments, and could support incremental hardware and services demand, though no financial metrics were disclosed.

Market Structure: Cisco (CSCO) is the clear direct beneficiary — integrated, sovereign-capable networking and on‑prem AI services strengthen its pricing power in campus/branch and regulated verticals versus point vendors. Expect a 3–5% share shift in mid‑market campus/branch deployments toward integrated incumbents over 12–24 months as customers prioritize post‑quantum, sovereign, and AgenticOps capabilities. NVIDIA (NVDA) sees secondary upside (AV/accelerator content in devices) but not material immediate revenue from Cisco announcements. Risk Assessment: Tail risks include export/regulatory limits on post‑quantum cryptography or national procurement bans (low-probability, high-impact), failed field integrations that delay renewals, and semiconductor supply constraints that could push lead times 8–12+ weeks. Near term (days–weeks) price moves will track product certification/newsflow; medium term (3–12 months) adoption and enterprise capex govern revenue; long term (1–3 years) stickiness of software/AI workflows determines annuity expansion. Hidden dependency: Cisco’s rollouts rely on third‑party silicon (Broadcom/NVIDIA) and cloud integrations — supplier bottlenecks or partner disputes are second‑order risks. Trade Implications: Favor selective long CSCO exposure (dividend + software annuity optionality) and small tactical NVDA exposure to capture peripheral hardware demand. Consider relative-value trades: long integrated incumbents vs. short pure-play campus/networking vendors that lack sovereign or post‑quantum capabilities. Volatility profile suggests using call spreads (6–9 month) to lever upside while capping premium outlay and deploying pair trades for downside protection. Contrarian Angles: The market underestimates that sovereign/on‑prem demand will blunt cloud‑only narratives — this benefits hardware/software integrators (Cisco) more than hyperscalers or pure software vendors. The bullish story may be underdone for CSCO (durable annuity growth) and overdone for NVDA attribution from this release; adoption complexity and integration headaches could delay ROI, causing a 6–12 month lag versus current sentiment.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment