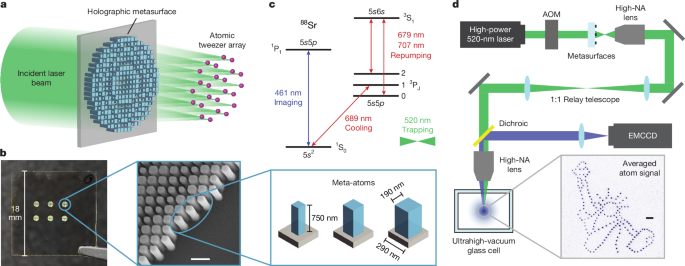

Researchers demonstrated trapping of single strontium atoms in holographic metasurface-generated optical tweezer arrays, achieving two-dimensional arrays with more than 100 single atoms and trap spacings down to 1.5 μm. Using high-refractive-index materials (silicon-rich silicon nitride and TiO2) they report high uniformity in trap depth, frequency and position and show scalability via simulations and experiments up to a 360,000-trap array, a development that lowers a major scaling barrier for neutral-atom quantum computing and could influence investment in quantum photonics, metasurface fabrication and related semiconductor-capable fabs.

Market structure: Metasurface-generated optical tweezer arrays shift value away from niche SLM/beam-steering integrators toward fabs, precision optics and specialty-material suppliers. Expect direct beneficiaries to be semiconductor-equipment and fab-service suppliers (equipment, etch/dep, metrology) and laser/optics vendors supplying imaging and trap lasers; initial incremental demand could be $200–500M over 2–3 years with potential to exceed $1B/year if neutral-atom platforms scale to commercial testbeds in 3–5 years. Broader winners include defense primes and national labs (R&D contracts) while incumbents tied exclusively to liquid-crystal SLMs risk margin erosion. Risk assessment: Key tail risks are (1) fabrication yield or uniformity failures at scale, (2) rapid emergence of IP disputes or restrictive export controls (US/China optics tech), and (3) slower-than-expected systems integration (vacuum, control electronics, lasers). Immediate market impact is minimal (days); watch for procurement orders and partner announcements in weeks–months; material constraints (high-index TiO2, SRN) and cleanroom capacity are hidden dependencies that can bottleneck adoption over 6–24 months. Catalysts: DARPA/AF contract awards, commercial demos showing >1,000 coherent qubits, or fab partnerships will accelerate adoption. Trade implications: Direct plays — establish 1.5–3% long exposure in precision-equipment makers (KLAC, AMAT, LRCX) over a 6–18 month horizon to capture increased nanofab spend; add 1–2% long in laser/optics names (IPGP, LITE) with 12-month call spreads (buy 12-mo ATM call, sell 12-mo +30% call). Pair trade — long KLAC (1.5%) vs short small-cap SLM/legacy-optics provider (select microdisplay/SLM name such as MVIS, 1%) to capture secular share shift. Sector tilt: increase semicap/photonic exposures by 200–300bps funded from cyclical consumer exposure; expect alpha realization as orders flow in 2–12 months. Contrarian angles: Consensus will overestimate near-term revenue; the market may underprice the long-term structural upside to fabs and materials suppliers if metasurfaces become standard in quantum stack — that favors equipment suppliers over platform integrators. Historical parallel: transition from bespoke optics to CMOS photonics (2010s) where toolmakers captured most value; unintended consequence is commoditization of tweezer modules, compressing ASPs for integrators but boosting recurring fab capital intensity. Monitor concrete metrics: announcements of multi-kilopixel production runs, >1,000-trap fault-tolerant demonstrations, and any export-control policy changes within 90–180 days.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30