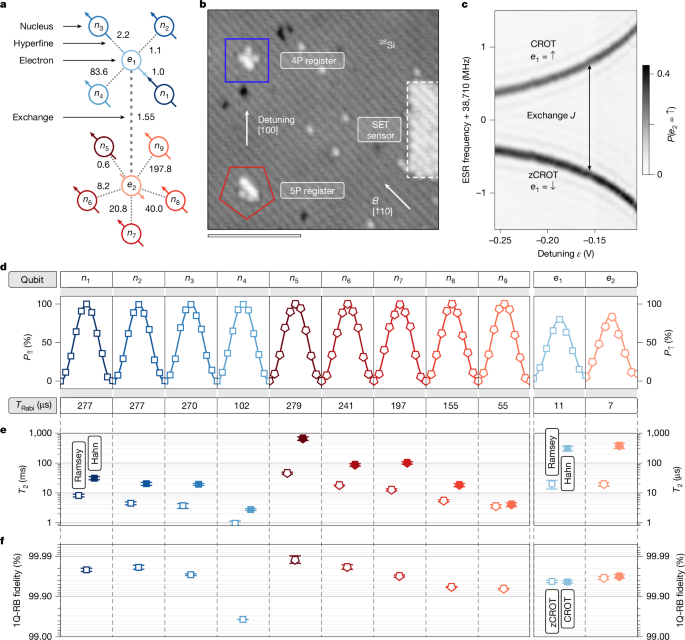

An 11-qubit atom processor in isotopically purified silicon-28, comprised of a 4P and 5P donor register linked by tunable electron exchange (J ≈ 1.55 MHz), achieves single- and multi-qubit gate fidelities ranging roughly 99.10%–99.99%, an electron–electron CROT fidelity of 99.64% and a nuclear CZ fidelity of 99.90%. The team reports local Bell-state fidelities up to 99.5%, non-local Bell fidelities up to 97.0%, and GHZ entanglement across up to eight nuclear spins — a technical milestone that strengthens the prospects and IP positioning of the Silicon Quantum Computing platform while representing incremental near-term commercial/market impact.

Market structure: The 11‑qubit silicon donor result strengthens the value chain around precision semiconductor fabrication and cryogenic control rather than immediately disrupting cloud/SaaS revenues. Equipment suppliers (ASML, AMAT, LRCX) and specialty materials (isotopically purified silicon producers, cryogenics vendors) are likely near‑term beneficiaries as customers plan pilot fabs; pure‑play quantum hardware equities (IONQ, RGTI) face idiosyncratic competition from platform diversity. Expect modest re‑rating in capital‑goods (5–15% rerating over 12–24 months if procurement timelines accelerate) while commercial revenue from quantum systems remains multi‑year out (3–7 years). Risk assessment: Tail risks include export controls/regulatory limits on advanced quantum tooling, a materials bottleneck (Si‑28 supply <100s kg/y) or fundamental scaling failures that push commercialization beyond 5 years; each would depress equipment orders by >30%. Immediate market impact is minimal (days), but watch weekly funding/partnership announcements (0–3 months) and government grant programs or procurement (3–18 months) which are high‑impact catalysts. Hidden dependencies: atomic‑placement tool capacity and foundry integration—if constrained, timelines slip even if physics is sound. Trade implications: Tactical trades favor suppliers to mini‑fabs and cloud integrators: constructive on ASML (ASML), AMAT (AMAT) and LRCX (LRCX) with a 6–18 month horizon; overweight MSFT (MSFT) for cloud quantum capture (12–36 months). Size positions modestly (1–3% NAV each) and hedge with short exposure to IONQ (IONQ) and RGTI, which rely on near‑term commercial narratives that may disappoint. Use options to cap downside: 9–15 month call spreads on ASML/AMAT and buy puts on IONQ/ RGTI for asymmetric risk/reward. Contrarian angles: The market underestimates the multi‑year procurement cycle for fabrication equipment—demand could be lumpy but durable, making equipment stocks underpriced relative to long‑run cash flows. Conversely, consensus may overprice near‑term revenue for pure quantum hardware; those valuations look vulnerable if error‑correction breakthroughs stall. Historical parallel: early photonics/semiconductor equipment cycles (late 1990s) where equipment vendors captured most value before turnkey system revenues materialized. Unintended consequence: fragmented platform standards could slow enterprise adoption and create a multi‑vendor winner‑take‑most dynamic that benefits large cap equipment/cloud names.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.28