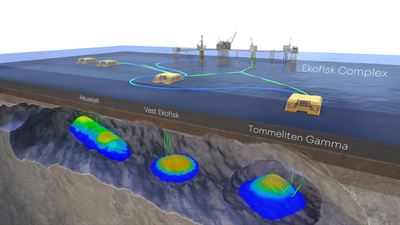

Vår Energi and partners, with ConocoPhillips Skandinavia as operator, have sanctioned the PPF re‑development in the Greater Ekofisk Area with Vår Energi’s net capital commitment of about USD 0.7bn; the project is expected to add ~55 mmboe in net 2P reserves and start production towards the end of 2028. The redevelopment—four new subsea templates and 11 horizontal production wells tied back to the Ekofisk complex—targets materially higher recovery from Albuskjell, Vest Ekofisk and Tommeliten Gamma, and is presented with a breakeven below USD 35/boe, expected ROI >25% and a rapid payback, supporting Vår Energi’s plan to sustain 350–400 kboepd to 2030. Vår Energi has also boosted its ownership in licences PL018B/F to ~52.28% (transaction closing Dec 2025) while holding 9.13% in PL044/D, strengthening its low‑cost reserve base and upside exposure in the area.

Vår Energi and licence partners, with ConocoPhillips Skandinavia as operator, sanctioned the Previously Produced Fields (PPF) re‑development in the Greater Ekofisk Area on 16 December 2025, with Vår Energi’s net capital commitment of approximately USD 0.7 billion and first production targeted towards the end of 2028. The sanction converts into an expected 55 million boe of net proved plus probable (2P) reserves tied to three fields (Albuskjell, Vest Ekofisk, Tommeliten Gamma) and a programme of four new subsea templates and 11 production wells using horizontal‑well technology. The company reports a competitive breakeven below USD 35/boe, an expected return on investment above 25% and a rapid payback profile, metrics that support Vår Energi’s stated objective to sustain 350–400 kboepd to 2030 and beyond. Technology and drilling design are presented as the drivers of materially increased recoverable reserves and production rates from mature reservoirs, which should improve unit economics if delivered on schedule and budget. Vår Energi also increased its ownership in licences PL018B/F to 52.28% (transaction expected to complete December 2025) and holds 9.13% in PL044/D, concentrating upside and reserve exposure while raising its capex and execution risk. Market signals show a moderately positive sentiment score (0.55) and a market impact score of 0.5, implying modest investor enthusiasm; primary risks remain execution, schedule slippage to 2028 and potential cost overruns against the stated USD 0.7 billion net commitment.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55