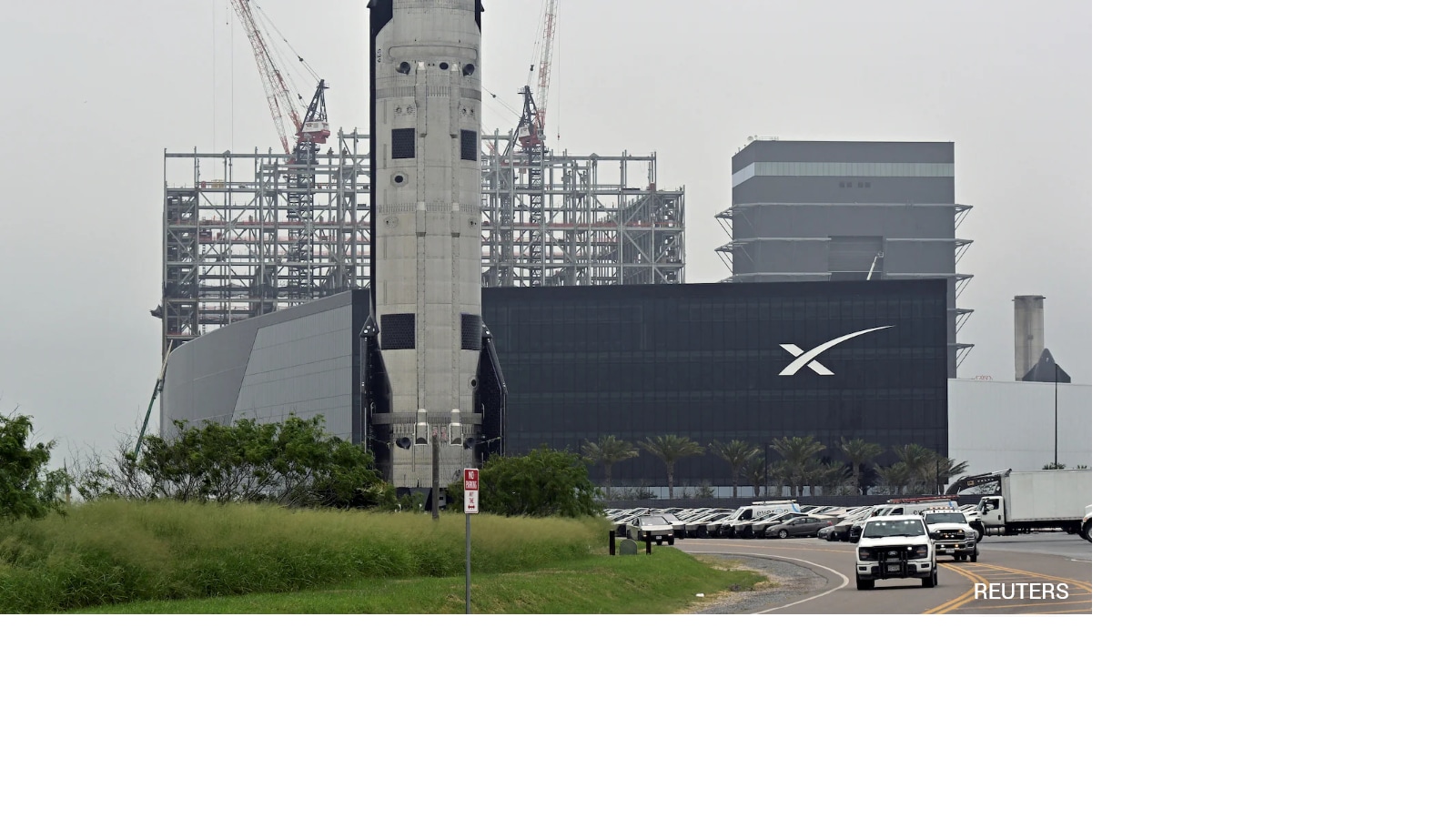

The article explains the IPO process and highlights that SpaceX has taken a key regulatory step by filing its public S-1, with plans to list on Nasdaq under ticker "SPCX." It also notes potential future public listings for OpenAI and Anthropic, underscoring continued momentum in high-profile tech and AI-related IPO candidates. The piece is largely educational and procedural, with limited near-term market impact beyond signaling activity in private-market unicorns.

A deep IPO pipeline is bullish for the underwriting complex, but the more important second-order effect is on private-market mark-to-market discipline. A credible path to public exits tends to reset late-stage venture pricing, compressing the spread between private rounds and public comps; that is a headwind for continuation funds, crossover managers, and firms reliant on evergreen NAV marks. In other words, the next 12-18 months may be less about one headline listing and more about whether the exit window reopens enough to revive deal velocity across venture and growth equity. The primary listed beneficiary is the exchange layer, not the issuer. Higher IPO throughput lifts recurring revenue for listing, data, and market-services franchises while also increasing secondary trading activity, options volume, and index inclusion demand after lock-up expiries. Banks benefit only if issuance breadth returns; a concentrated mega-cap debut cycle can actually be less attractive than a steady stream of mid-sized deals because it improves fee durability and reduces underwriting inventory risk. The main risk is timing: if rates reprice higher or tech risk appetite rolls over, the IPO window can shut quickly even after a successful filing. That creates a reflexive downside for names leveraged to first-day performance and a larger overhang from post-listing supply once insider lockups expire. For the mega-private AI names, the market may be underestimating how much public comparables will force margin accountability; once listed, “growth at any cost” narratives usually compress over 2-4 quarters as investors demand evidence of monetization and capital intensity discipline.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

0.12

Ticker Sentiment