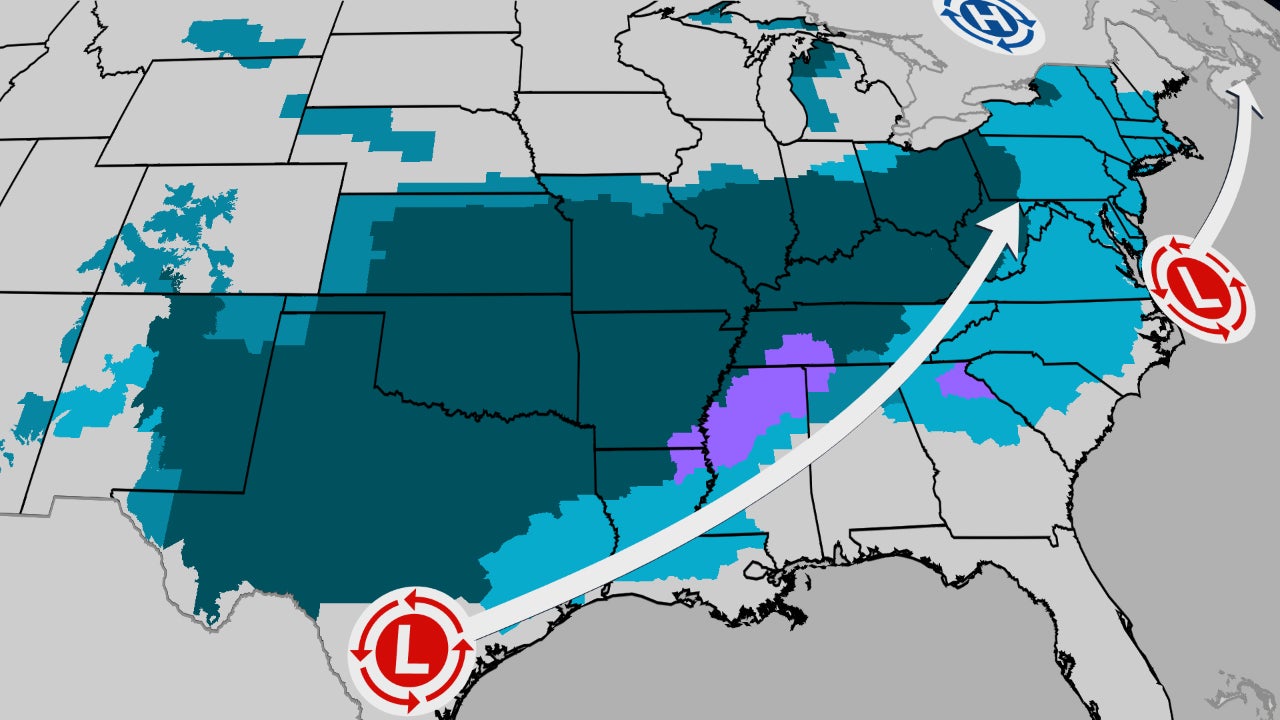

A historic winter storm, named Fern, will impact roughly 230 million people across 34 states with widespread heavy snow and 'catastrophic' ice from the southern Plains through the Northeast, producing foot-plus snow in many areas and widespread power outage risk in parts of 12 states. Anticipated effects include multi-day power outages, major East Coast flight delays and cancellations, hazardous and potentially impassable roads, and a nor’easter-driven continuation of snow and coastal rain — risks that could pressure regional energy demand/pricing, disrupt airlines and logistics, and spur elevated insurance and infrastructure repair costs.

Market structure: Immediate winners are short-term natural gas and power sellers, utilities (Duke DUK, Southern SO, NextEra NEE) that can lean on wholesale price spikes, and retail chains selling generators/heaters (HD, LOW). Losers are airlines/airports (AAL, DAL, UAL) and time-sensitive logistics (UPS, FedEx) facing multi-day cancellations and reroute costs; regional retailers and restaurants suffer foot-traffic drops. Expect regional power forwards to widen 100–500% in constrained zones and Henry Hub volatility to rise by 20–40% intraday in the first 7–14 days. Risk assessment: Tail risks include a prolonged multi-day grid failure in the Southeast/central US driving insured losses >$1bn and fast-tracked regulatory rate caps or accelerated capex mandates for utilities (negative margin pressure if forced below cost recovery). Time horizons: immediate (0–7 days) travel/operation shocks and gas/power spikes; short-term (weeks–quarters) claims/reserving and earnings revisions for insurers/utilities; long-term (quarters–years) utility capex and grid modernization regulatory outcomes. Hidden dependencies include pipeline bottlenecks, LNG flows, and spare-transformer inventories that can amplify outages. Trade implications: Tactical plays: buy short-dated NG exposure (1–3% portfolio via UNG or 2–6 week HH call spreads) and purchase 1–2 week ATM to 15% OTM puts on AAL/DAL (0.5–1% each) ahead of weekend travel. Establish 2–3% long utility exposure (DUK/NEE) for rate-base defensive yield and write 3-month covered calls to monetize elevated implied vol. Consider pair: long HD (2%) for consumer generator demand vs short UAL (1%) for travel disruption exposure. Contrarian angles: Consensus may overvalue permanent demand uplift for utilities — once temperatures moderate and outages resolve, nat gas and spot power should mean-revert 20–50% within 2–6 weeks; therefore sell strength in NG and avoid adding large multi-quarter longs in utilities until regulatory clarity (rate cases) is visible. Historical parallels: 2021 Texas freeze produced sharp spikes then partial mean reversion; worst equity losses concentrated in firms exposed to market settlements, not broad utilities.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60