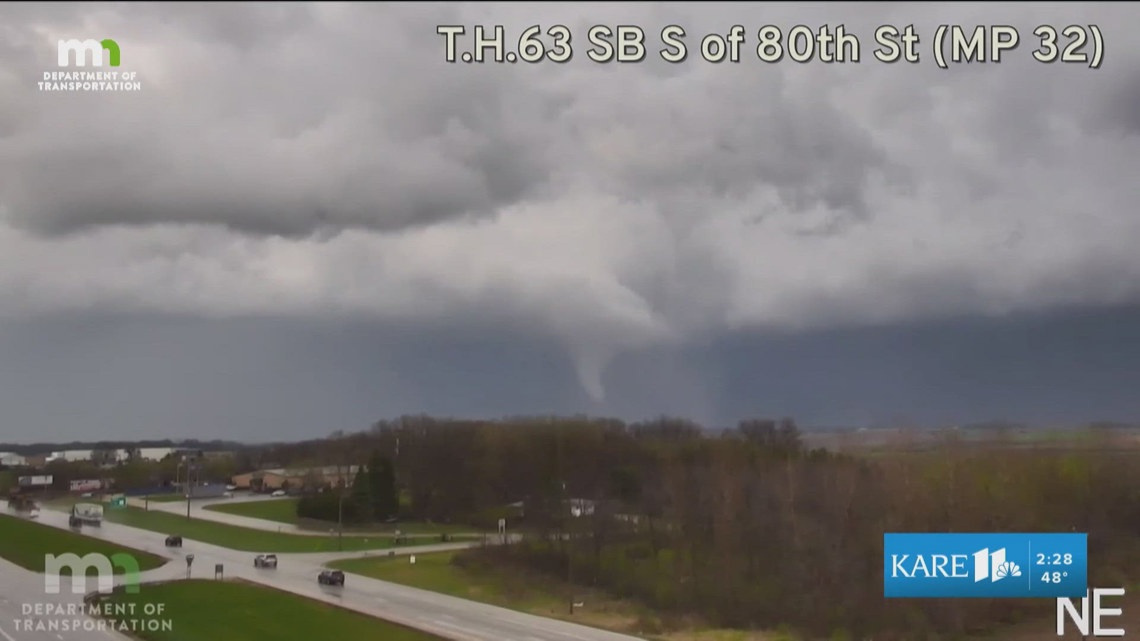

Multiple reported tornadoes caused damage across southeast Minnesota and western Wisconsin, including about 30 homes damaged in Marion Township and nearly 2,500 People's Energy Cooperative members left without power. The Olmsted County board issued a disaster declaration, and the National Weather Service reported a tornado north of Elgin that flipped a semi and damaged two farmsteads. The event is likely to pressure local utilities, insurers, and property owners, with broader regional disruption from tree, power line, and structural damage.

The immediate market impact is less about the storm itself and more about the sequencing of cash-flow stress: utilities absorb restoration capex first, then insurers, then local landlords and small contractors. For listed utilities with regional exposure, the near-term risk is not revenue loss but working-capital drag and elevated outage-related operating costs, which can compress margins for one to two quarters before any eventual true-up through rate cases. The bigger second-order beneficiary is often the restoration ecosystem—electrical equipment, temporary power, debris removal, roofing, and building materials—where demand can spike within days and persist for months.

The housing angle is more nuanced than a simple rebuild trade. In smaller markets, a concentrated damage event can tighten already thin contractor availability and push labor/material pricing higher, creating an inflationary pocket that helps revenue but hurts gross margins for builders and insurers. If the disaster declaration unlocks federal assistance, the first wave of spend tends to be emergency stabilization; the larger follow-on spend shows up only after claim adjustment and permitting, which means public-market beneficiaries may lag the headline by 30-90 days.

Energy is the most underappreciated transmission channel: localized outages can modestly lift diesel demand, backup generation usage, and short-term power price volatility, but the move is usually too geographically contained to matter for national power markets unless outages widen materially. The contrarian view is that the selloff in regionally exposed insurers or utilities may be overdone if damage is concentrated and largely insured, because catastrophe losses are typically manageable versus the market’s knee-jerk reaction to any tornado cluster. The real tail risk is a broader severe-weather pattern extending into summer, which would compound claim severity, strain repair supply chains, and turn a one-off event into a sector-wide reserve reset.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60