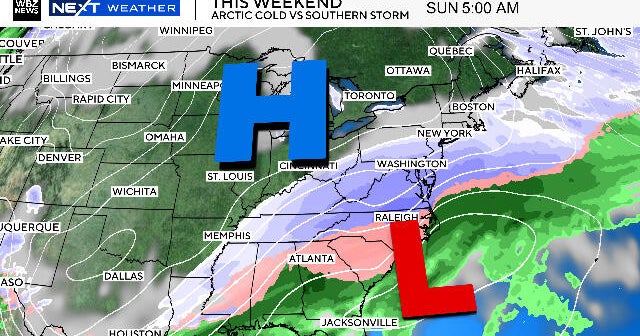

A potent winter storm forming in the deep South is forecast to clash with a surge of Arctic air this weekend, creating an 'atmospheric battle' that will determine whether New England sees extreme cold or a major coastal winter storm. Current model guidance favors Arctic air pushing the storm south of New England, leaving Boston to experience plunging temperatures (single digits overnight into Wednesday) and gusty winds, while parts of the South and Mid-Atlantic face the risk of a foot-plus of snow and ice across a roughly 1,000-mile corridor. Implications are primarily operational—potential disruptions to regional travel, energy demand and local services—rather than broad market-moving financial data.

Market structure: A cold-dominant outcome favors energy and retail convenience plays (heating fuels, propane, utility generation, home-improvement) while a southward storm track favors insurers, road/rail logistics, and regional fuel retailers in the Mid-Atlantic/South. Expect near-term demand shock for natural gas and electricity over the next 3–14 days (potentially +15–40% call for incremental loads vs. baseline), while transportation and perishable-supply chains face localized capex and delay risk. Pricing power will be transitory—suppliers with tight storage/pipeline access gain, spot markets and winter-forward contango should widen. Risk assessment: Tail risks include a northward storm producing major insured losses in New England (>$1bn regional insured loss) or a prolonged multi-week pipeline constraint that sustains gas prices into spring. Immediate window: 0–14 days for fuel/transport shocks; short-term: 1–3 months for insurer/residual demand effects; long-term: seasonal weather pattern could shift capex decisions for utilities and fuel hedging through 2026. Hidden dependencies: pipeline nominations, LNG feedgas flows, and utility take-or-pay contracts can amplify or mute price moves. Trade implications: Favor short-dated, directional energy exposure and tactical hedges for travel/logistics. Volatility will spike in regional airline and natural-gas options; use spreads to cap downside. Retailers with strong supply chains and DIY exposure should get a near-term bump in discretionary kit (generators, heaters, shovels) over 1–6 weeks. Monitor implied vol and open interest as catalysts for option entry. Contrarian angles: Consensus expects the cold to “win”; markets may underprice the northward-storm tail that would crush travel and boost insurers—this is a low-probability, high-payoff scenario to buy protection on regional insurers or airline puts. Conversely, if cold holds, energy longs (NG) are underowned by funds focused on green transition, so a measured long in short-dated gas exposure could be underpriced. Historical parallels (2013–2014 polar outbreaks) show 2–6 week commodity repricing followed by mean reversion, arguing for time-limited trades rather than structural positions.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.10