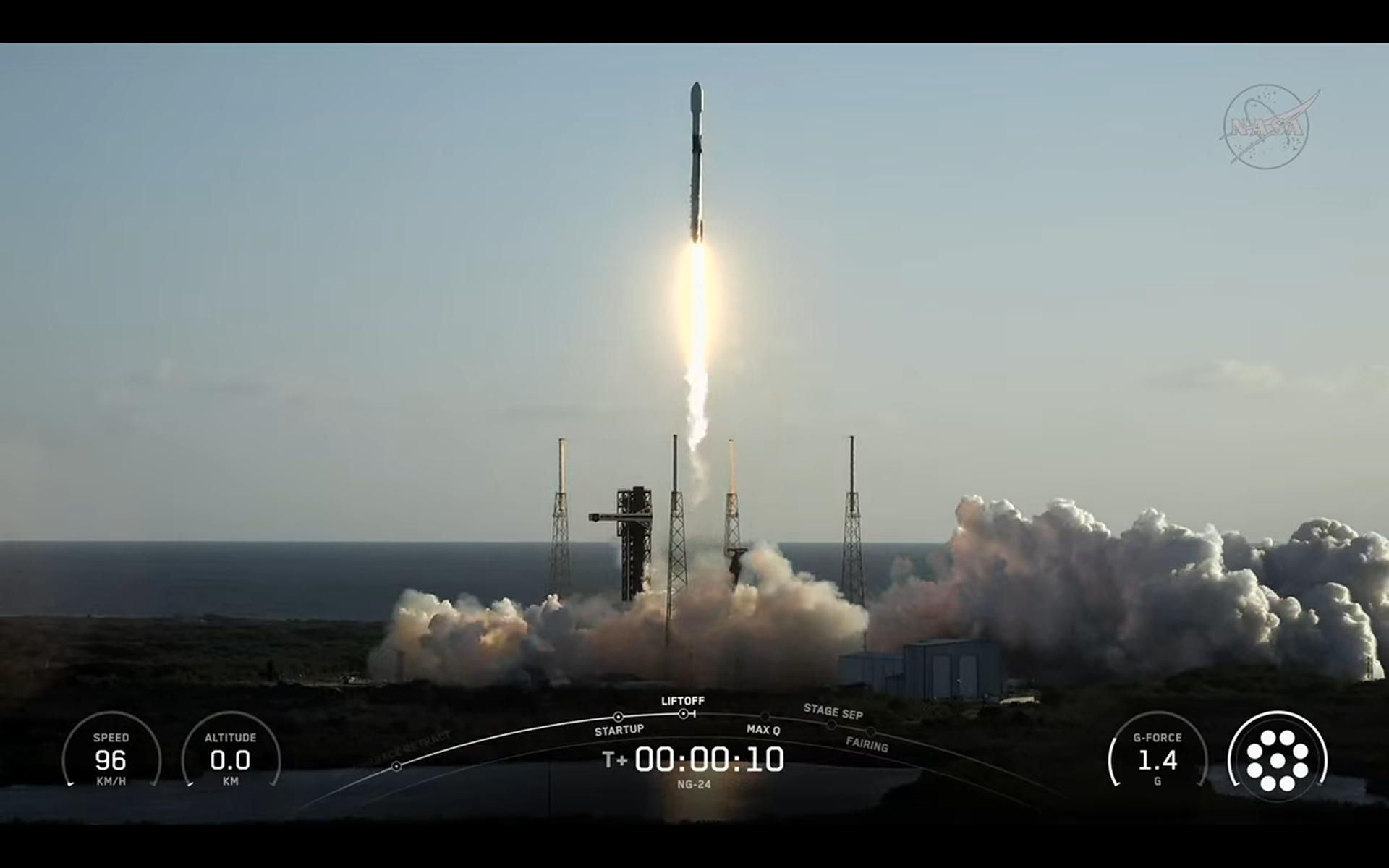

SpaceX successfully launched Northrop Grumman's NG-24 Cygnus XL cargo mission to the ISS carrying about 11,000 pounds (4,990 kilograms) of science equipment and supplies. The Falcon 9 first stage landed safely about eight minutes after liftoff, marking its seventh flight, while the Cygnus XL is scheduled to be captured by the ISS on April 13. The article is operationally positive for SpaceX and Northrop Grumman but largely routine and unlikely to move markets.

This is a quiet but positive data point for NOC: the market usually underappreciates how much ISS logistics functions as a recurring, operationally sticky service business rather than a one-off launch event. The larger cargo variant expands payload economics, which should improve mission efficiency and reduce the probability of schedule slippage tied to frequent top-up flights. That matters because reliability, not just launch volume, is what preserves Northrop’s position in NASA-linked logistics procurement. The second-order beneficiary is the broader space-support ecosystem: larger cargo capacity raises the value of each launch slot and should increase demand for downstream integration, payload prep, and ground support services. For SpaceX, the Falcon 9 reuse cadence remains a margin flywheel; for Northrop, the key is that a higher-capacity vehicle helps defend relevance against reusable alternatives by making the service package more competitive on cost per delivered pound. The risk is that if this larger platform proves operationally smooth, it sets up a gradual procurement shift toward fewer, bigger cargo runs—good for mission success, but potentially compressive for future flight count growth. Near term, there is little direct earnings sensitivity for NOC, but the catalyst path is cumulative: successful missions reduce perceived technical risk and support backlog durability over months, not days. The main tail risk is any deployment anomaly or delayed rendezvous, which would revive questions about the economics of scaling the vehicle. Contrarian read: the upside is likely more in confidence-building than near-term revenue, so the move may be underappreciated by investors who focus only on defense hardware and miss the recurring services angle.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

0.12

Ticker Sentiment