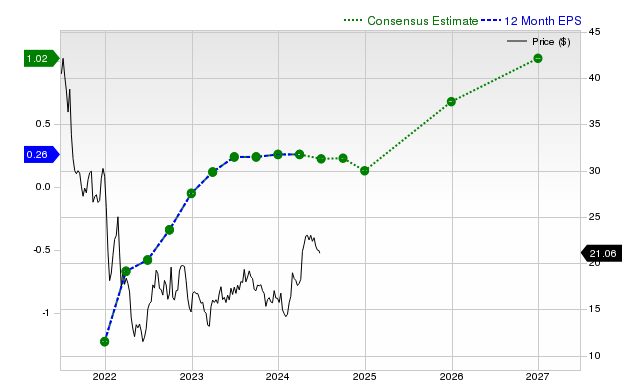

Coupang reported last-quarter revenue of $9.27 billion (+17.8% YoY) and EPS of $0.05 (versus $0.06 a year ago), beating revenue consensus by 2.31% and delivering a 25% EPS surprise. Zacks shows an expected current-quarter EPS of $0.05 (+25% YoY) but consensus estimates have moved unevenly (current-quarter estimate down 10% in 30 days; current fiscal year EPS $0.17, -22.7% YoY; next fiscal year $0.57, +237.3%). The stock has lagged peers (-6.8% past month) and is assigned a Zacks Rank #4 (Sell) with a Value Style Score of D, indicating it trades at a premium to peers and prompting a cautious near-term outlook for investors.

Market structure: Coupang’s numbers (Q rev +17.8% y/y to $9.27B; Q EPS $0.05; FY est $0.17, next FY $0.57) show healthy top-line growth but compressed near-term earnings power. Winners are scale players and third‑party logistics providers that can monetize fulfillment (Amazon AMZN, local 3PLs); losers are low‑margin domestic sellers and any capital‑intensive smaller e‑commerce platforms. Pricing power remains weak — expect continued promo-led volume growth and margin pressure over the next 2–6 quarters unless SG&A intensity is cut by >200–300 bps. Risk assessment: Tail risks include Korea regulatory action (antitrust/marketplace rules) and logistics capex overruns; a KRW move of ±5% would meaningfully change USD EPS translation and could swing consensus by >10% within a quarter. Near term (days–weeks) volatility is driven by earnings revisions and FX; medium term (3–12 months) by margin recovery or continued promotional spend; long term (12–36 months) by unit economics of same‑day logistics and market share consolidation. Hidden dependency: fulfillment cost per order and fuel/wage inflation are non‑linear and can erase expected FY+237% EPS gains if they rise >10% y/y. Trade implications: Near term (60–90 days) favor tactical downside: defined‑risk put spreads or short exposure to CPNG to capture further estimate cuts (Zacks rank 4). Over 12–24 months, consider asymmetric long exposure sized small (1–3% portfolio) if price retraces 25–35% — next‑FY EPS recovery is priced into forward estimates but not guaranteed. Pair trade: short CPNG vs long AMZN (equal dollar) for 3–6 months to capture scale/margin dispersion; options: buy 3‑month puts 10–20% OTM or put spreads to limit cost. Contrarian angle: Consensus focuses on short‑term EPS downgrades and labels valuation rich (Value D), but it understates Coupang’s logistics moat and potential margin inflection if promotions and last‑mile density improve — a 200–400 bps margin rebound would re-rate the stock materially. Reaction may be overdone in the next 1–3 months; however, upside is binary and contingent on execution — use small, defined‑risk positions rather than full conviction longs until you observe two consecutive quarters of margin improvement and positive EPS revisions (>+10%).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment