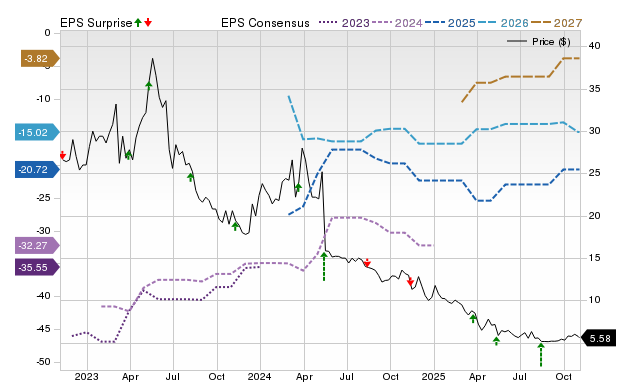

Bolt Biotherapeutics (BOLT) is anticipated to report a quarterly loss of $5.07 per share, a 36.6% year-over-year increase, despite an expected 32.5% revenue decline to $0.77 million. However, a positive Zacks Earnings ESP of +0.33% combined with a Zacks Rank #3 suggests BOLT is likely to beat consensus EPS estimates, which could influence its near-term stock performance. In the same sector, Protagonist Therapeutics (PTGX) is also projected to surpass its consensus loss estimate of $0.59 per share, driven by an expected 113.7% revenue increase to $10 million and a strong Earnings ESP of +29.92%.

Bolt Biotherapeutics (BOLT) is projected to report a narrower loss of $5.07 per share for Q3 2025, representing a 36.6% year-over-year improvement in earnings, despite an anticipated 32.5% decline in revenues to $0.77 million. The positive Zacks Earnings ESP of +0.33%, coupled with a Zacks Rank #3, strongly suggests BOLT will likely surpass its consensus EPS estimate. This potential beat is further supported by a history of beating estimates in two of the last four quarters, including a significant 30.31% surprise in the prior quarter. However, the 0.83% downward revision of the consensus EPS estimate over the past 30 days introduces a degree of uncertainty regarding analyst sentiment leading into the report. While an earnings beat is predicted, the substantial year-over-year revenue contraction remains a key concern, indicating potential underlying business challenges that could overshadow a positive EPS surprise. The sustainability of any stock price movement will heavily depend on management's forward-looking commentary. In contrast, industry peer Protagonist Therapeutics (PTGX) presents a more robust outlook, with an expected loss of $0.59 per share for Q3 2025, a 9.3% improvement year-over-year. PTGX is also forecasting significant revenue growth of 113.7% to $10 million, alongside a higher Earnings ESP of +29.92% and a Zacks Rank #3, making it a strong candidate for an earnings beat. PTGX has a stronger track record, having surpassed EPS estimates in three of the last four quarters. The overall market sentiment for these biotech firms is moderately positive and speculative, with a low to moderate market impact expected from these individual reports. Investors should recognize that while an earnings beat can provide a short-term catalyst, the underlying revenue trends and future guidance are critical for long-term valuation in this sector.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.50

Ticker Sentiment