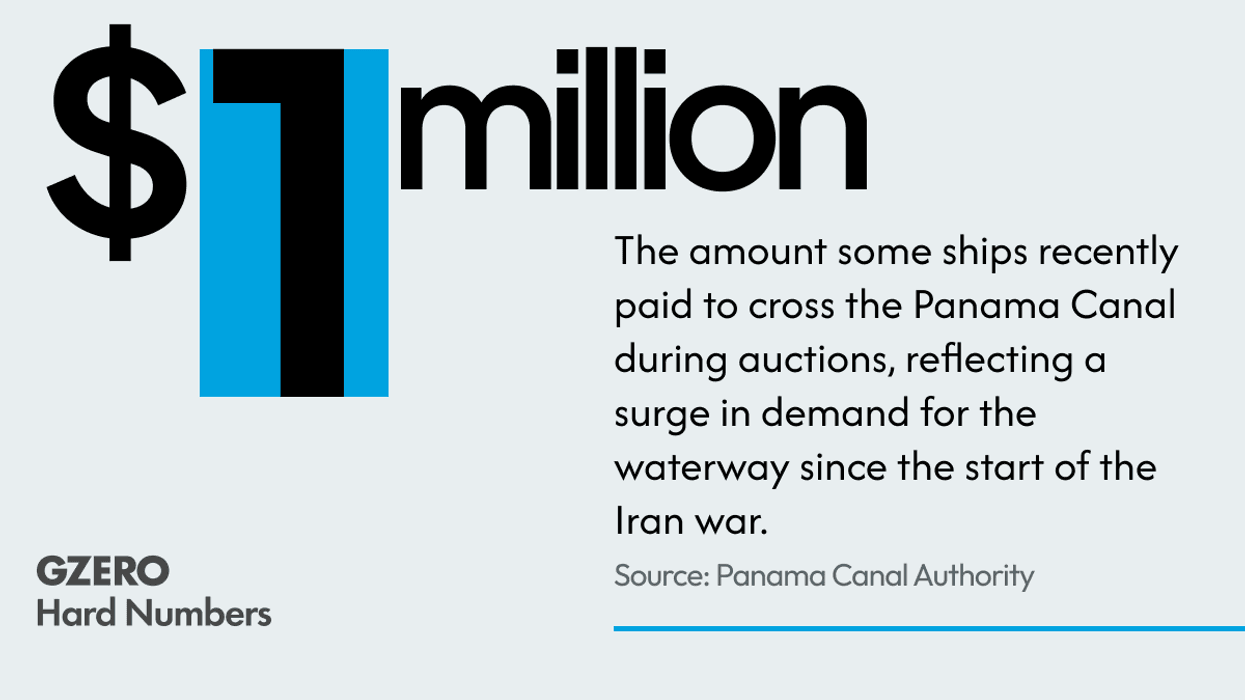

Costs to pass through the Panama Canal have hit record highs as the Iran war disrupts global oil shipping, with daily auctions attracting five times as many bids as before the conflict. The article also notes a surge in U.S. oil and fuel shipments through the canal, mainly from the Gulf Coast. The implications are broader freight and energy shipping cost pressure, with notable market-wide relevance for oil flows and logistics.

The key market signal is not just higher transit costs, but a forced re-pricing of routing optionality. When a chokepoint’s auction clears at a premium, the value migrates to whoever can shorten voyage time, hold inventory closer to end demand, or bypass the canal entirely. That creates a relative winner set in Gulf Coast exporters and tankers with flexible route exposure, while refinery systems dependent on just-in-time imported barrels face a margin squeeze as delivered costs rise faster than benchmark crude.

The second-order effect is a temporary boost to US Gulf Coast crude and product flows, which can tighten domestic logistics even if headline oil prices stay contained. If more barrels are pulled through one corridor, basis differentials can widen, rail/truck/storage economics improve in the interior, and marine transport bottlenecks become a larger part of the price signal than outright commodity moves. That matters because shipping stress tends to persist longer than the initial geopolitical shock; even if the conflict de-escalates, operators usually keep bidding aggressively until route reliability is proven for several weeks.

The contrarian risk is that the market may be overestimating the duration of the disruption while underestimating policy response. If insurance, naval protection, or diplomatic deconfliction improves transit reliability, the auction premium can compress quickly, hurting any crowded “shipping crisis” positioning. On the other hand, if the conflict broadens or the canal becomes a standing security risk, the real upside is in assets with alternative export routes and storage optionality, not in generalized energy beta.

From a trading perspective, this looks better expressed as a relative-value logistics trade than a pure long oil expression. The cleanest setup is to own beneficiaries of route scarcity and short names exposed to imported feedstock or freight inflation, with the trade horizon measured in days to a few months rather than quarters. The market is likely to chase headline energy futures first, but the more durable P&L comes from dislocations in transport, basis, and inventory carrying costs.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35