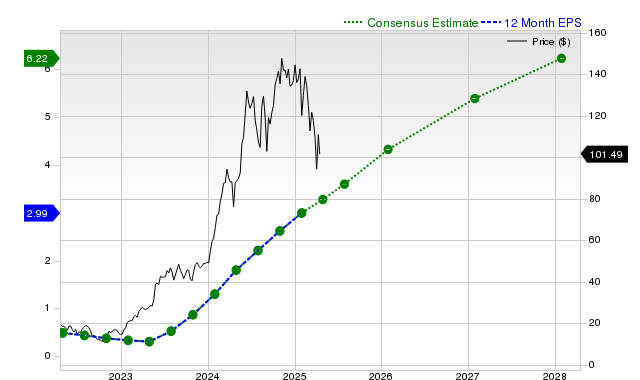

Nvidia reported $57.01 billion in revenue last quarter (+62.5% YoY) and EPS of $1.30 versus $0.81 a year ago, beating revenue consensus by 4.14% and EPS by 4.84%. Zacks' updated consensus places quarterly EPS at $1.47 (+65.2% YoY) and sales at $65.47 billion (+66.5% YoY), with fiscal‑year EPS forecasts of $4.61 (+54.2%) and $6.65 (+44.3%) for the following year and revenue forecasts of $209.61 billion and $293 billion, respectively. The stock carries a Zacks Rank #2 (Buy) but a Value Style Score of D (trading at a premium), and has returned -4% over the past month versus -1.8% for the S&P 500.

Winners are hyperscalers, cloud/software vendors and foundries that capture AI GPU volumes; losers are smaller AI-infrastructure vendors and legacy CPU vendors whose pricing and backlog are being squeezed. The competitive dynamic further concentrates share with NVDA reinforcing a tollbooth position—expect sustained ASP leverage and multi-quarter order books that allow 10–20%+ pricing premiums versus peers in tight capacity windows. Supply/demand appears tighter for advanced GPU wafers and HBM memory with meaningful lead times; that implies persistent upside to NVDA margins but also higher volatility around capacity signals. Cross-asset: stronger NVDA-led AI demand supports industrial capex cyclical trades, steepens tech credit spreads slightly (spread compression for high-grade, widening for lower-rated OEMs), lifts semiconductor equipment stocks and increases equity option IV on NVDA while modestly pressuring safe-haven bonds and USD on risk-on flows. Key tail risks: export controls or China restrictions, a sudden hyperscaler inventory drawdown, or a supply shock at TSMC/TSMC-equivalents; any of these could move stock ±20–40% in 1–3 months. Near-term (days-weeks) expect headline-driven IV swings; medium-term (1–6 months) depends on order cadence and product availability; long-term (12–36 months) is exposure to model adoption saturation and competitive architectures. Consensus underestimates concentration risk and margin cyclicality—growth is real but highly lumpy and correlated to a few buyers. The market may underprice regulatory or geopolitical interruptions; watch for 200–300bp margin misses and hyperscaler capex slowdowns as triggers to re-evaluate positions. Historical parallel: rapid re-rating episodes in semis (2016–18) ended with sharp mean reversion after order-cycle peaks.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment