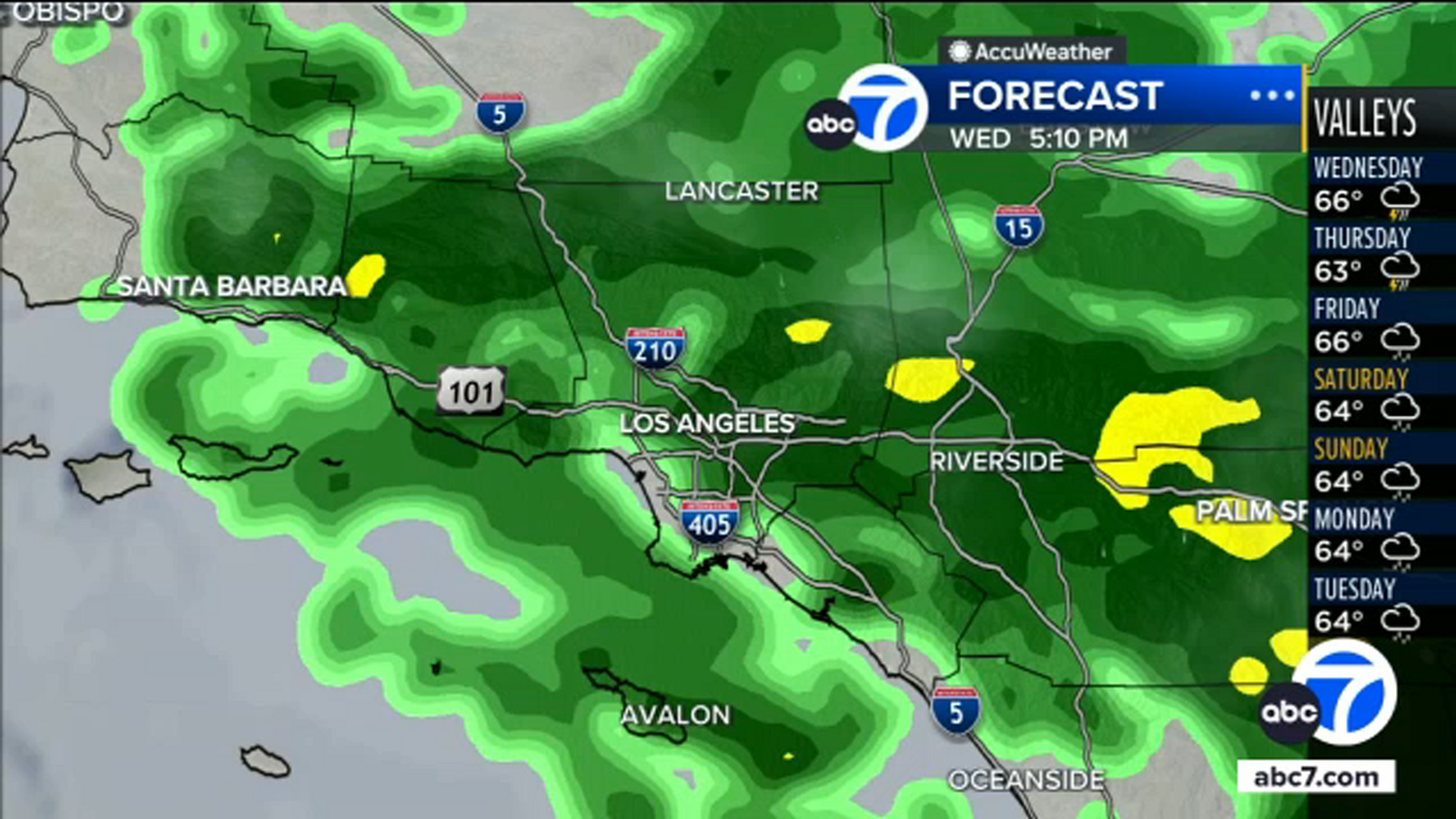

Southern California first responders are preparing for a New Year's Eve storm expected to produce roughly 1–3 inches of precipitation in lowlands and up to 5 inches in mountain areas, with the worst conditions overnight through the afternoon. Los Angeles Fire Department officials are urging motorists to avoid travel and exercise caution, implying potential localized disruptions to transportation, emergency services demand and short-term operational impacts for businesses in affected areas, though the event is unlikely to have meaningful market-wide effects.

Market structure: Short-duration storms in SoCal create clear winners (regional ski/resort operator MTN; short-term snow/road-maintenance contractors; natural gas demand beneficiaries) and losers (airlines serving LAX/SNA/SAN—LUV, DAL, AAL, UAL—and ground carriers FDX, UPS). Expect 24–72 hour travel/ground-disruption windows, meaning transient revenue loss (airline RPKs down an estimated 1–3% on NYE) and small but concentrated logistics bottlenecks that can propagate nationally through hub-and-spoke networks. Risk assessment: Tail risks include a heavier-than-forecast storm or infrastructure failure (power loss at a major CA DC) causing multi-week fulfillment delays and 1–3% quarterly revenue hits for exposed retailers; regulatory risk is low. Time horizons split: immediate (0–7 days) travel disruption, short-term (2–8 weeks) logistics backlog and spot pricing moves in nat gas, long-term (quarters) only if repeated weather events compound capacity constraints. Key hidden dependency: holiday peak travel amplifies otherwise modest storms. Trade implications: Tactical direct plays include short-dated (7–10 day) 5–10% OTM puts on LUV and DAL sized 1–2% of portfolio each to capture elevated IV and cancellation risk; buy 1% notional 2–6 week UNG exposure or short winter-hedged call spreads on FDX/UPS for 3–10 day disruption risk. Rotate 1–3% from airlines/airports into energy/utilities (XLU or nat-gas producers) for 1–6 week resilience. Enter options 48–72 hours before storm peak and exit within 7–14 days unless new data emerges. Contrarian angles: Market tends to oversell airline/logistics names after holiday storms; set buy triggers: if LUV/DAL fall >6% intraday, accumulate a 2–4% mean-reversion long for 3–6 months. Conversely, avoid overpaying for insurers—single mild storm rarely justifies premium re-rating. Monitor BTS cancellation counts (>1k/day in CA) and airline IV spikes (>30% relative to 30-day avg) as concrete trade signals.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.15