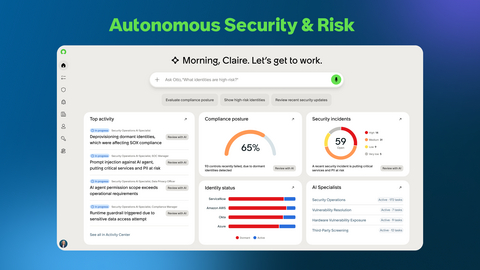

ServiceNow launched Autonomous Security & Risk and said security and risk has surpassed $1 billion in annual contract value, highlighting strong demand for its AI platform. The company is integrating Armis for continuous asset intelligence and Veza for identity governance to create a more complete security, risk, and compliance stack. Customer examples cited include a 97% reduction in threat containment time, a 96% elimination of dormant non-human identities, and a 75% faster control attestation process.

This is less about a single product launch and more about ServiceNow attempting to become the control plane for AI-era enterprise security. The key second-order effect is that NOW is moving up the stack from workflow automation into a higher-switching-cost risk graph that spans identity, asset, and remediation data; if adopted, that deepens platform lock-in and raises the cost of ripping out adjacent security vendors over the next 12-24 months. The monetization vector is not just seat expansion but module attach across risk, compliance, SecOps, CMDB, and AI governance, which should support ACV durability even if core ITSM growth normalizes.

For the ecosystem, Armis is strategically more important than the press release suggests: feeding passive asset discovery into CMDB turns opaque OT/IoT exposure into an actionable workflow, which is precisely where point solutions lose pricing power. That creates a headwind for standalone asset visibility vendors and some mid-market vulnerability management names because the buyer now gets “good enough” context bundled into a broader platform. Veza integration is similarly threatening to niche identity-governance players, especially where the buying center is converging on CISO-led platform consolidation rather than IAM-led best-of-breed.

FTNT is the subtle loser/winner mix: the collaboration framing implies Fortinet remains relevant as an enforcement and telemetry layer, but also signals that core control is shifting to NOW. That can compress wallet share over time if customers use ServiceNow as the orchestration layer and leave networking/security hardware as a lower-margin execution backend. Near term, the catalyst is procurement conversion; the risk is that enterprise deployments take longer than the narrative, so the stock may outrun realized ARR by 2-4 quarters, while regulatory scrutiny around autonomous agents could delay budgets in highly regulated verticals.

The contrarian view is that the market may be underestimating how hard it is to unify identity, asset, and response data across heterogeneous environments; if implementation friction is high, this remains a story stock until evidence appears in renewal rates and net new security ACV. But if ServiceNow shows even modest incremental attach in the next two quarters, the revenue mix shift could re-rate the multiple because security/risk becomes a structurally larger growth engine than the market currently models.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.70

Ticker Sentiment