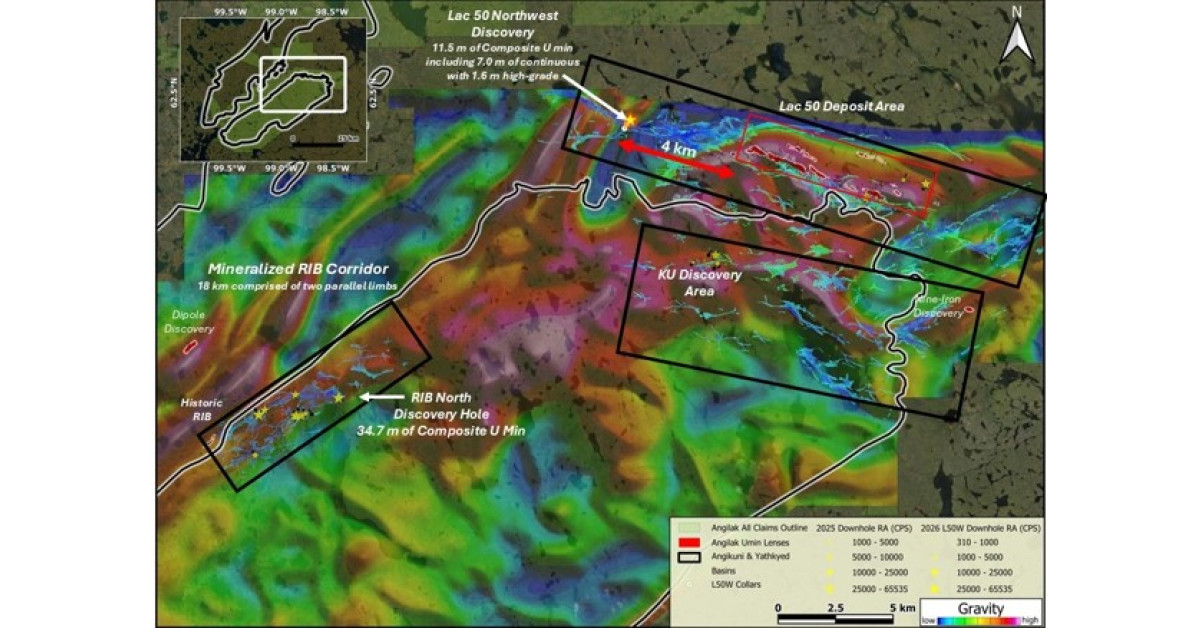

ATHA Energy reported the widest uranium intercept at Rib North to date: drillhole RIBN-DD-003 returned 37.0 m of total composite uranium mineralization over 15 zones from 541.7 m to 652.0 m, including a 4.5 m highest-grade interval (571.7–576.2 m). Across the first eight 2026 program holes, 6/8 intersected uranium and continuity was outlined along strike by 300+ m, plus a secondary east-west mineralized horizon ~1 km away. The company is also advancing a large 2026 Angilak program targeting ~20,000 m of drilling (three rigs) through September and continued follow-up across the broader 18 km Mineralized RIB Corridor, which remains open in all directions.

This is incrementally positive for ATHA, but the value inflection is still geological optionality, not economics. The real mechanism is de-risking: repeated step-outs that keep hitting mineralization increase the odds of a future resource estimate and improve financing leverage, yet they do not change NAV much until assays, thickness, continuity, and tonnage are demonstrated. The biggest near-term beneficiary is ATHA’s equity tape; the bigger medium-term beneficiary could be the company’s ability to raise capital on less punitive terms if the next assay batch confirms the gamma data. The second-order loser is not a named competitor but the exploration funding stack: every “successful” follow-up tends to pull more capital toward ATHA at the expense of other Canadian uranium juniors with weaker drill cadence. That said, the market may be overpricing the signal because these are radiometric intercepts, not assayed widths, and the program is still a large spend with dilution risk over the next 1-3 months. If uranium spot softens or risk capital rotates out of small caps, the stock can give back the move quickly even if drill chatter stays constructive. Contrarian view: the consensus may be extrapolating a deposit-scale story from sparse spacing and gamma counts before true thickness is known. The setup becomes materially more bullish only if assays validate grade continuity across multiple holes and if geophysics turns the corridor into a repeatable target set; absent that, this is a financing catalyst more than a fundamental one. Over 6-18 months, the key falsifier is a weak assay conversion rate from the reported radiometric hits or a follow-on capital raise at a discount that wipes out the exploration premium.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment