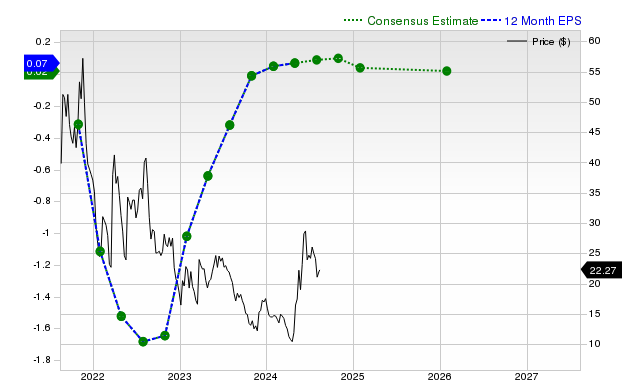

GameStop (GME) has seen notable investor attention, with shares returning +8.7% over the past month, outperforming the S&P 500's +2.3%. The company recently reported Q4 revenues of $972.2 million and EPS of $0.25, surpassing consensus estimates by +8.02% and +31.58% respectively. However, forward-looking consensus estimates project significant revenue declines of -6.3% for the current fiscal year and -17.7% for the next, alongside a -52% EPS decrease for the next fiscal year, leading to a Zacks Rank #3 (Hold) recommendation, suggesting the stock may perform in line with the broader market.

GameStop (GME) is exhibiting a significant disconnect between recent performance and its forward-looking fundamental outlook. The stock's +8.7% return over the past month, outperforming the S&P 500, reflects heightened investor interest likely fueled by a strong last reported quarter. The company posted a revenue of $972.2 million, a +21.8% year-over-year increase and an +8.02% surprise, while EPS of $0.25 massively beat consensus by +31.58%. However, this positive historical data is overshadowed by a deteriorating forecast from sell-side analysts. Consensus estimates project revenue to decline by -6.3% in the current fiscal year and a further -17.7% in the next. Similarly, after a projected +127.3% EPS jump in the current year, earnings are expected to fall by -52% in the next fiscal year. The fact that these estimates have remained unchanged over the last 30 days indicates a lack of positive catalysts to alter the bearish analyst sentiment. This conflict between past results and future projections underpins the stock's Zacks Rank #3 (Hold) and its 'C' grade for valuation, suggesting it is trading at par with peers and may perform in line with the broader market in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.10

Ticker Sentiment