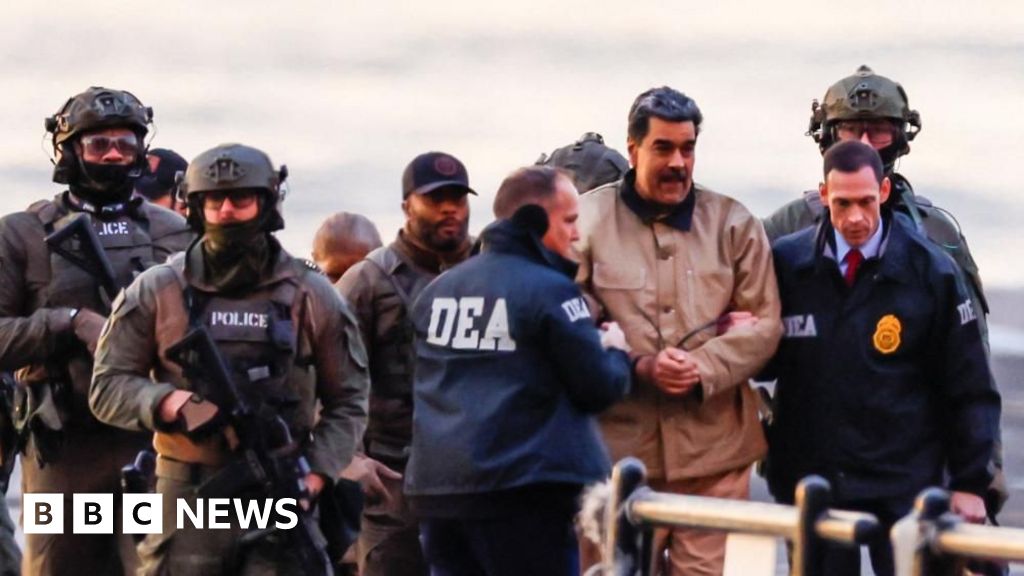

Nicolás Maduro and several close associates, including his wife and son, have been indicted in New York on four counts alleging a long-running cocaine‑trafficking conspiracy that partnered with groups the U.S. designated as terrorist organizations; prosecutors allege abuse of state institutions, bribes, use of machine guns and seek forfeiture of property and money. Maduro was taken to the U.S. by U.S. forces, pleaded not guilty, and faces a next hearing on March 17; legal experts say the seizure may violate international law even as U.S. courts likely retain jurisdiction, creating a high‑profile geopolitical and legal risk for Venezuela and regional markets.

Market structure: The immediate winners are defense/security suppliers and safe-haven assets; losers are high-beta Latin American sovereign credit and any corporate exposure tied to Venezuelan state economy. Venezuela’s crude output is small (roughly 0.5–0.8 mbpd), so direct global oil supply shock is limited, but risk-premium repricing can push Brent/WTI +$3–$8 temporarily and EM FX (COP, BRL) weaker by 1–4% in days. Financial plumbing (insurance, shipping, port services) sees higher margins and potential repricing for Venezuela-related routes. Risk assessment: Tail risks include cartel retaliation or regional destabilization that could disrupt an additional 100k–300k bpd or trigger cyber/terror strikes raising risk premia across commodities and defense; probability low (<15%) but impact high. Time horizons: immediate (days) for volatility spikes, short-term (weeks–3 months) for EM outflows/CDS widening, long-term (6–24 months) for sanctions, asset seizures, and persistent political realignment. Key hidden dependencies: shipping insurance clauses, counterparty exposure in correspondent banks, and oil offtake contracts that can be unilaterally re-routed. Trade implications: Tactical plays favor 1–3% portfolio-sized hedges: long gold/GLD and short selected EM sovereign credit or EEM exposure; consider buy 1–3 month Brent/WTI call spreads to capture a $3–8 move. Sector rotation into US defense primes (LMT, RTX) and security contractors is sensible on a 3–12 month view; trim Latin America consumer/financial exposure and raise cash if CDS on regional credits widens >75–100 bps. Contrarian angle: Consensus may overstate permanent oil disruption — historical parallels (Panama/Noriega) show short sharp risk-on/off moves then normalization over 3–9 months. If no broader regional escalation within 60–90 days, EM assets will likely mean-revert and present buying opportunities; conversely, legal/UN backlash could prolong sanctions and increase long-term risk to firms with Venezuela linkages.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35