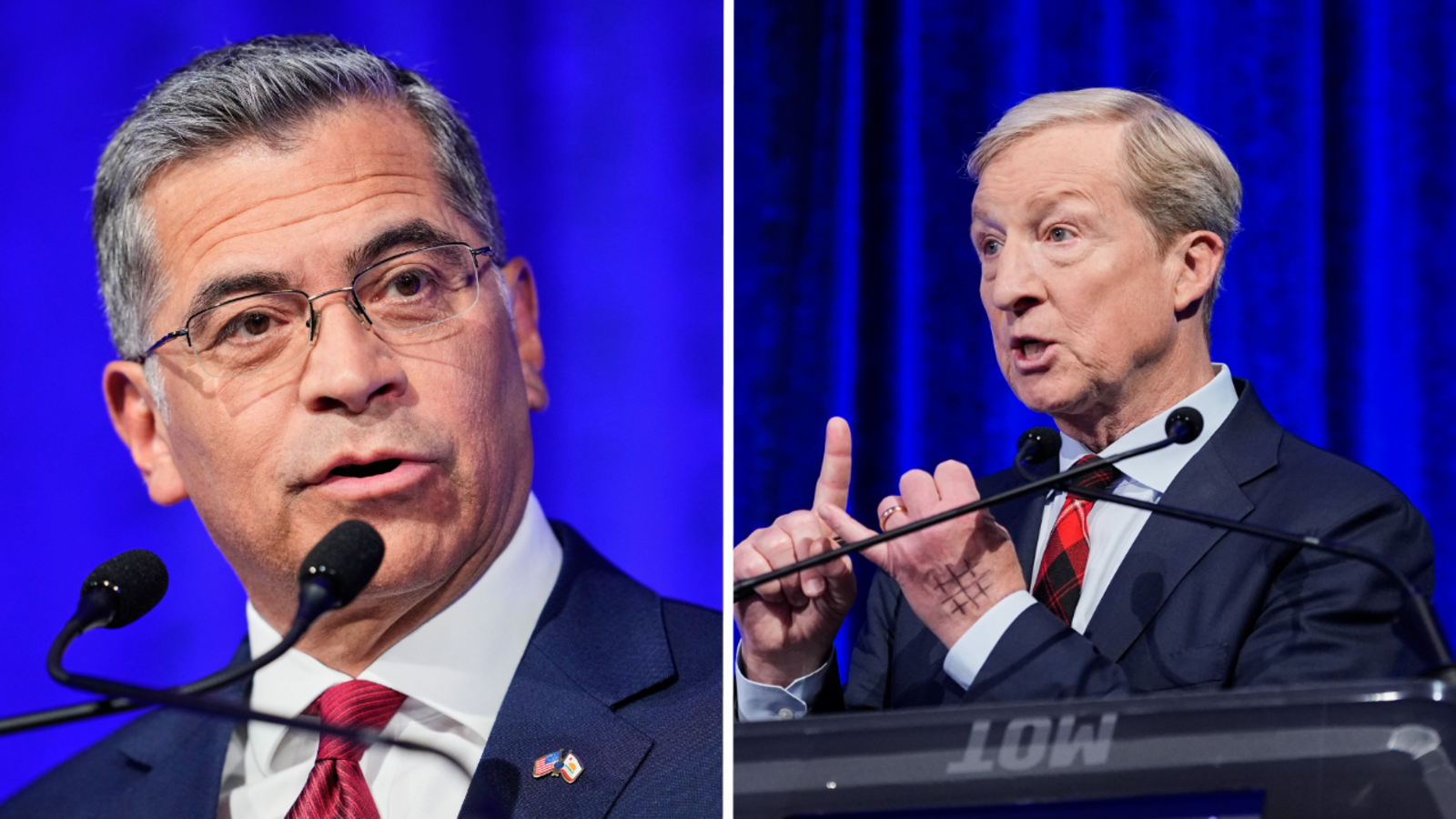

New California governor polling shows Xavier Becerra leading with 25%, followed by Steve Hilton at 21%, Tom Steyer at 19%, Chad Bianco at 16% and Katie Porter at 13%. The race remains fluid, but the latest polls suggest the field is narrowing around Becerra, Hilton and Steyer, with two candidates set to advance to the November general election. The article is primarily political reporting with no direct market or corporate impact.

The market read-through is not about California politics per se; it is about which policy regime gets priced into utilities, housing, labor, and tax-sensitive names for the next 12-18 months. A tighter-than-expected contest raises the odds of a less ideologically pure governor and a more fragmented mandate, which usually reduces near-term policy surprise but increases post-primary coalition risk. That matters for anything levered to California regulation or state spending, because the first-order winner is whoever can keep the anti-incumbent vote from consolidating, while the second-order loser is the candidate pool that depends on turnout enthusiasm rather than strategic voting.

The key second-order effect is on positioning: if investors were leaning into a clean two-Republican or two-Democrat outcome, that hedge can now unwind quickly as “top-two” incentives compress the field. In practice, that means the trade is not a directional bet on one candidate winning, but on volatility around utility regulation, climate capex, and state tax rhetoric fading after the primary. The clearest catalyst window is the next 72 hours; after that, attention shifts from polling to ballot mechanics and coalition math, which should lower headline risk unless late movement in turnout shifts one side materially.

The contrarian angle is that the consensus may be overestimating how much a single primary reshapes investable policy. California governance is usually constrained by budget math, municipal resistance, and legal process, so even a sharp swing in the nominee mix often translates into incremental rather than regime-level changes. That argues for fading knee-jerk sector reactions unless one candidate’s path implies a credible tax or regulatory shock with a 6-12 month implementation window.

Net: this is a low-conviction event for broad indices, but it can matter tactically for California-exposed utilities, renewables, REITs, and select financials with heavy state exposure. The tradable edge is in relative value and event-volatility, not outright market direction.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00