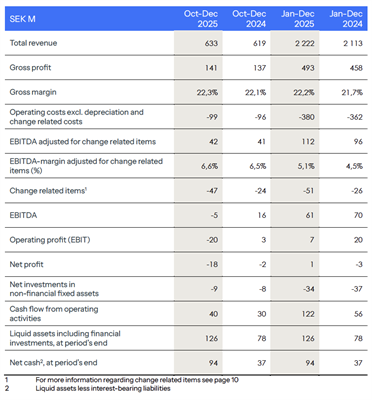

Tradedoubler reported 2025 revenue of SEK 2,222M (up 5% reported; +8% FX-adjusted) and gross profit SEK 493M (+8% reported; +11% FX-adjusted), with adjusted EBITDA of SEK 112M (up 17% reported; +23% FX-adjusted). Q4 revenue was SEK 633M (+2% reported; +7% FX-adjusted) and adjusted EBITDA SEK 42M; reported EBITDA was depressed by a SEK 44M revaluation of a performance-based purchase price related to the KAHA GmbH acquisition. Cash flow from operations strengthened to SEK 122M for the year, net cash ended at SEK 94M, and full-year EPS was SEK 0.02; management highlights strong Metapic growth, AI integration and an app launch planned H1 2026 while reiterating medium-term targets (25% EBITDA margin, 10% revenue growth).

Market structure: Tradedoubler (per release) is a direct beneficiary of the secular shift to performance-based and influencer marketing via Metapic (order value +50% y/y). Winners include creator platforms, merchants paying on performance, and technology-enabled affiliate networks; losers are legacy display/ad-agency models facing CPM pressure and clients cutting brand budgets. Gross margin steady ~22% limits immediate pricing power, so scale (Metapic app H1 2026) is the primary lever for improved unit economics. Risk assessment: Key tail risks are regulatory scrutiny of influencer disclosures in the EU/US, a reversal in ad budgets that reduces order value growth below 20% q/q, and FX volatility (quarterly FX swings altered reported EBITDA by ~SEK 2.5M). Short-term (days-weeks) risk centers on Q&A/market reaction; medium-term (1–6 months) on Metapic app execution and client churn; long-term (12–36 months) on whether adjusted EBITDA can sustainably approach management’s 25% margin target. Hidden dependencies: Metapic growth relies on creator adoption and low-cost moderation; earnout revaluation signals potential future cash outflows. Trade implications: Tactically, favorable asymmetric risk/reward exists into H1 2026 catalysts (app launch, client wins) given net cash SEK 94M and improving adjusted EBITDA (112M FY). Direct plays: size modest long exposure to Tradedoubler ahead of app launch; hedge execution risk with options. Sector rotation: trim legacy agencies and reallocate to high-ROAS adtech/SaaS names; monitor cash and quarterly Metapic KPIs for rebalancing. Contrarian view: The market likely underprices scalable Metapic upside — consensus may ignore cross-vertical expansion (finance/apps) and network effects from an app-driven link share increase. Conversely, consensus may be too optimistic on margin expansion if the app increases moderation/customer acquisition costs. Watch for re-rating parallels to past adtech platform IPOs where >30% topline growth triggered >2x multiples, but also for profit cannibalization scenarios if low-margin volumes dominate.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment