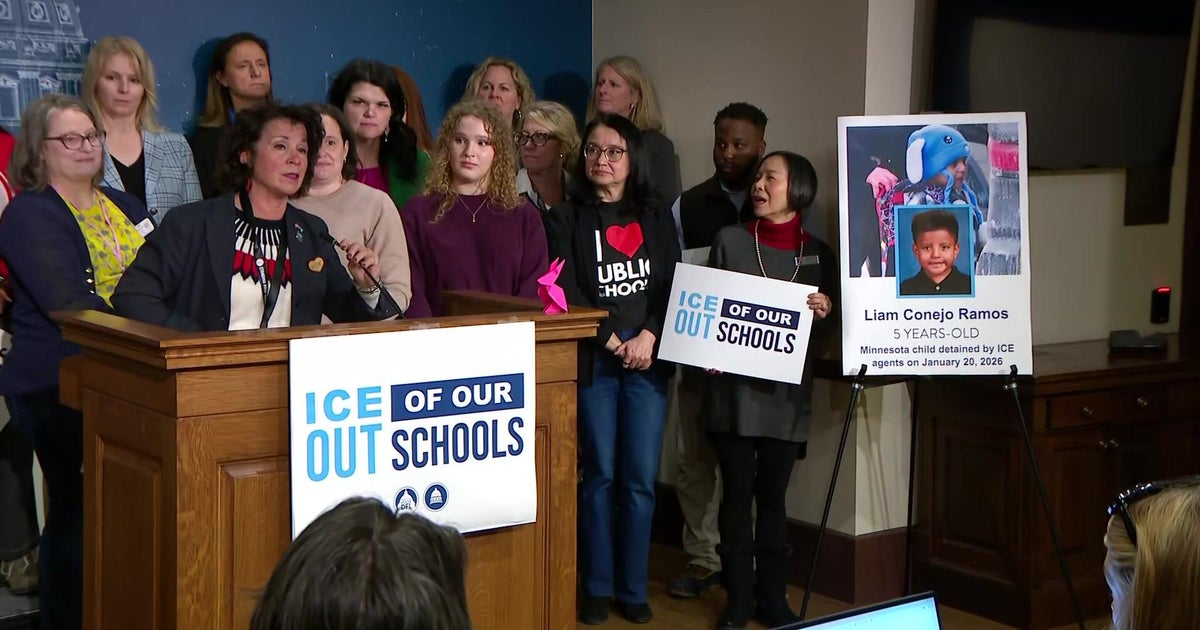

Minnesota school districts reporting increased ICE enforcement say fear and anxiety are driving students out of classrooms into virtual learning and prompting protests. Fridley Public Schools — 80% students of color — now has 16% of students enrolled virtually, and Rochester reported more than 530 additional absences between Jan. 9–22; students are demanding guaranteed safe busing, suspension of the policy that withdraws students after 15 consecutive absences, and a pause on standardized testing. The disruptions could strain district operations and attendance-linked funding and spur state-level policy responses.

Market structure: Localized ICE enforcement acts as a demand shock to in-person K–12 services — winners are providers of remote learning infrastructure (LRN, ZM), broadband carriers (CMCSA, CHTR) and device OEMs (AAPL); losers are attendance‑funded public districts, contractors tied to in‑person services (school transportation, testing firms). If absenteeism rises 1–5% in affected districts over a semester, attendance‑based state aid and per‑pupil revenues can fall materially (low single‑digit %), compressing budgets and vendor contract renewals. Risk assessment: Tail risks include statewide policy shifts (e.g., suspension of attendance rules or emergency funding) and large-scale ICE operations that could cause 5–15% transient enrollment shifts and force muni downgrades for small districts; expect immediate noise (days), material fiscal effects in 1–3 months, and credit consequences visible in 2–4 quarters. Hidden dependencies: vendor contract renewal timing and state emergency appropriations can reverse impacts quickly; muni spread widening of 10–50bp is plausible for small, illiquid district paper. Trade implications: Tactical longs: select ed‑tech (LRN) and broadband infrastructure (CMCSA) as 3–12 month plays; tactical shorts/put exposure on niche testing vendors (Pearson/PSO) and small‑muni funds that lack state backstops. Use pair trades (long LRN, short PSO) to isolate secular virtual‑learning upside vs testing headwinds; prefer defined‑risk option spreads to limit downside. Contrarian angle: Market consensus likely overstates systemic muni contagion — national muni ETFs unlikely to rerate much; conversely, underestimates stickiness of virtual enrollment, which can raise recurring SaaS revenue by 5–15% annually for dominant ed‑tech providers. Historical parallels (localized migration/enforcement spikes) show temporary attendance shocks often trigger policy relief rather than permanent demand destruction, so favor selective, asymmetric option structures over blanket shorts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40