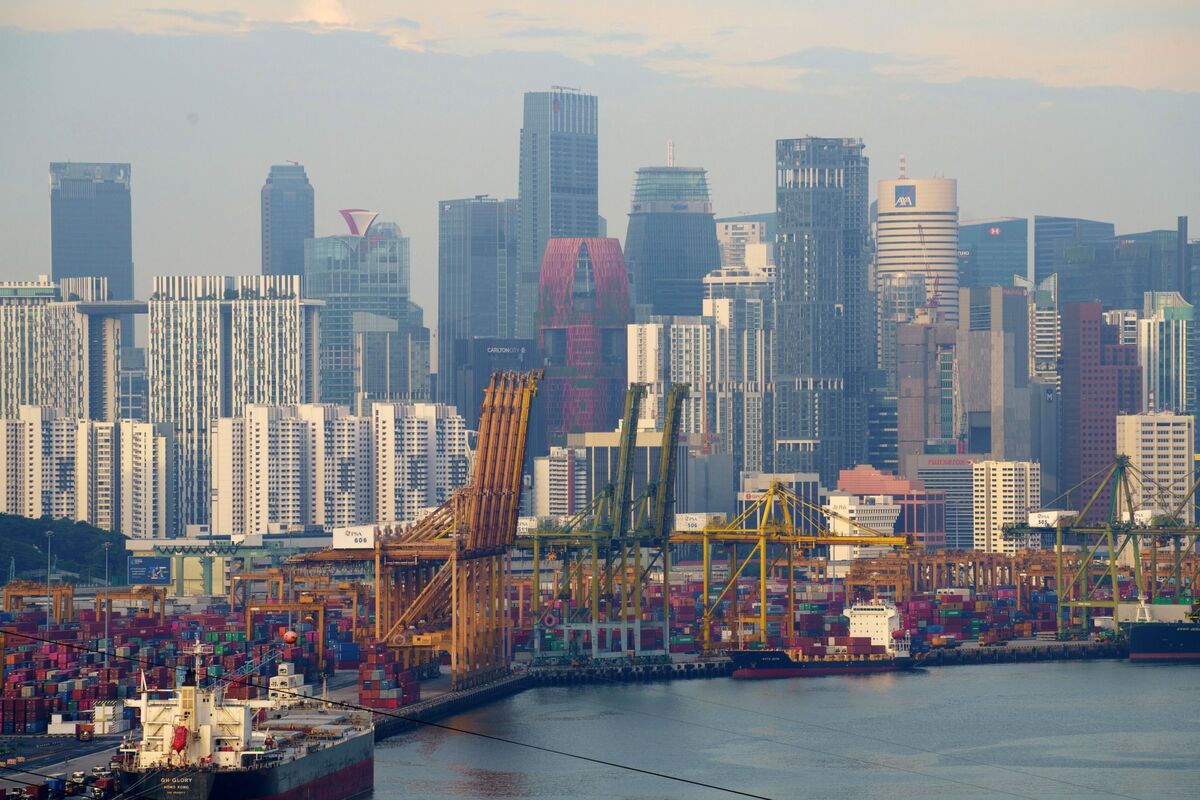

Singapore and its business lobby are formally pushing back against a U.S. trade probe that alleges manufacturing overcapacity and failures to enforce bans on imports tied to forced labor. The dispute centers on trade-policy compliance and could raise scrutiny of Singapore’s export regime, but the article reports no immediate policy changes or market-specific financial impact. Overall tone is defensive and cautious as authorities defend alignment with international standards.

This is less about Singapore’s direct exposure and more about the precedent risk for Asia’s “low-friction” trade hubs. If US trade enforcement starts treating transshipment, documentation gaps, or supplier-chain opacity as a tariff/forced-labor issue, the first-order damage will fall on intermediaries with thin margins and high import turnover, not just on Singapore itself. That would shift sourcing toward jurisdictions with cleaner provenance data and away from networks that rely on speed and regulatory arbitrage.

The second-order winner is compliance infrastructure: customs software, supply-chain traceability, audit, and trade-finance providers that can monetize provenance verification. In contrast, regional manufacturers and distributors with mixed-origin inputs face higher working-capital needs, slower clearance times, and a greater chance of shipment holds. Over the next 1-3 months, the key market reaction is likely not outright tariff impact but risk premium expansion for firms with complex APAC routing and weak ESG/labor disclosure.

The contrarian angle is that this may be more signaling than escalation. US probes often create short-lived headline risk unless they uncover a clear enforcement case; Singapore’s institutional response reduces the probability of a broad punitive outcome. If the issue remains framed as documentation and enforcement rather than intentional evasion, the long-run damage to Singapore’s logistics franchise could be modest, while the real beneficiaries are vendors selling compliance as a service.

Catalyst-wise, watch for follow-on requests for information, expanded country coverage, or a named-company enforcement action; those would convert this from a policy nuisance into a supply-chain rerouting event. Absent that, the overreaction risk is in pricing a durable trade barrier where the more likely outcome is higher compliance cost and slower processing, not a structural shift in trade flows.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.15