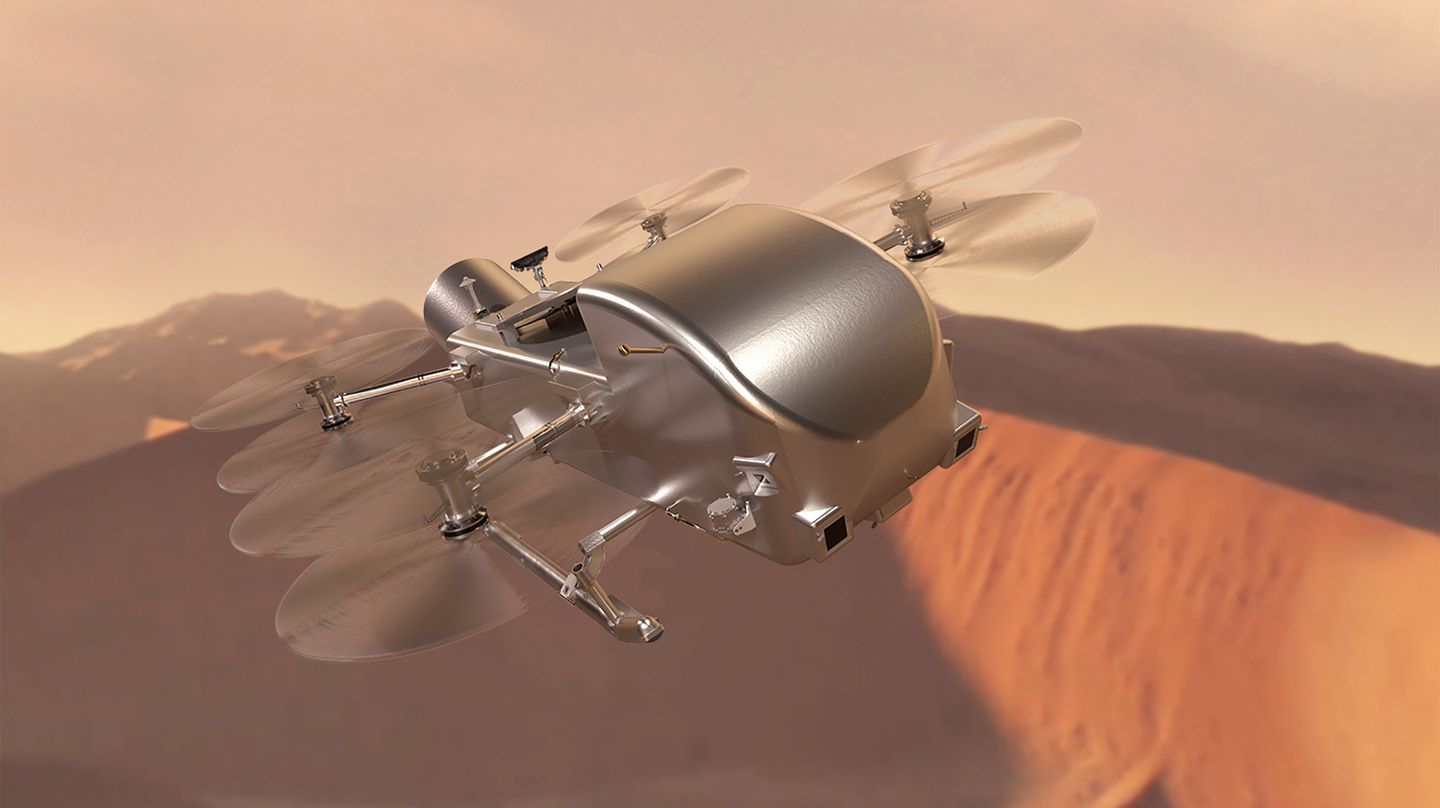

NASA/Johns Hopkins APL has begun building and testing the nuclear-powered Dragonfly rotorcraft, a car-sized mission to Saturn's moon Titan scheduled to launch in 2028. The mission budget is about $3.35 billion and will launch on a SpaceX Falcon Heavy no earlier than spring 2028, with integrated-electronics and power-switch testing continuing into early 2027 and subsequent systems tests at Lockheed Martin. This milestone reduces program technical risk by moving Dragonfly into hardware integration and environmental testing, though near-term market impact on suppliers or equities is likely limited.

A mission of this class functions as a concentrated multi-year procurement program that funnels predictable revenues into a narrow set of suppliers (integration houses, heavy‑lift launch capacity, specialty avionics and extreme‑environment materials). Expect multi-year backlog visibility for primes who win integration/testing work and for materials vendors supplying flight‑qualified foams, composites and thermal control; such contracts tend to be lumpy but high‑margin and carry outsized follow‑on services (testing, spares, firmware upgrades) over 3–5 years.

A second‑order supply effect is on strategic raw materials and niche fuels: increased utilization of radioisotope power systems and long‑duration deep‑space avionics tightens demand for Pu‑238 processing, radiation‑hardened electronics, and qualification facilities — bottlenecks that can drive supplier pricing power and create entry barriers for latecomers. Parallel demand for Falcon‑class heavy lifts compresses manifest availability for other large payloads, which should lift incremental launch pricing by low‑double-digit percentages in stressed manifest periods and reorganize commercial launch schedules.

Program schedule and regulatory risk are the dominant asymmetries. Cost growth, nuclear licensing, or a test anomaly can delay acceptance tests and push integration revenue into later accounting periods; conversely a clean qualification run materially de‑risking deep‑space rotorcraft architecture would catalyze follow‑on contracts across civil and defense agencies within 6–18 months. Insurance and indemnity markets are another nonlinear lever — a single mishap with a nuclear‑powered payload would sharply reprice mission insurance and raise program financing costs for years.

From a technology diffusion perspective, success revalidates powered in‑situ mobility (rotorcraft) in tenuous atmospheres, accelerating R&D spending by competitors and commercial partners in Arctic/Antarctic and subsea analog markets. That creates an investible sequenced opportunity: early wins for systems integrators and specialty materials suppliers, followed by a wave of smaller tactical suppliers and service providers around test and operations once flight heritage accumulates over 1–3 program cycles.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35