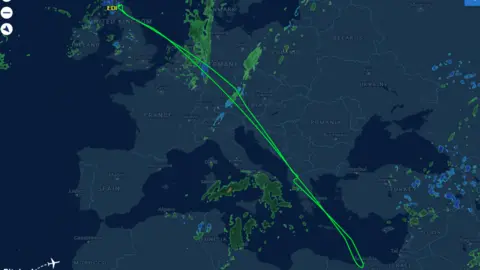

An Emirates flight (EK24) from Edinburgh was forced to return after spending 11 hours in the air when Dubai International suspended operations following an Iranian drone strike that ignited a fuel tank; no injuries were reported. Dubai later announced a gradual resumption of select flights and advised passengers to check with airlines; the airport handled nearly 90 million international travellers in 2025, underscoring the scale of disruption risk. The strike is part of sustained Iranian missile/drone attacks on the UAE (reported ~2,000 strikes), raising regional travel and insurance risk and posing downside pressure on Gulf carriers and aviation-linked service providers.

This incident is a reminder that concentrated hub risk (single-airport dependency) creates outsized knock-on costs across the transport stack: each diverted widebody leg adds meaningful fuel, crew and maintenance friction — on the order of 1–3 flight-hours of extra block time per round trip, which translates into $10k–$40k incremental variable cost per flight and forces capacity compression on peak long-haul flows for days. That friction cascades into airfreight: when Gulf hubs tighten or close temporarily, belly capacity evaporates first, pushing spot airfreight rates up 10–30% within 1–4 weeks and shifting volume to higher-cost integrators or slower sea lanes.

Insurance and risk-pricing change faster than schedules: underwriters and brokers will respond with route-specific surcharges and narrower war-risk corridors, likely raising premium loadings for Gulf-linked sectors by 20–50% within the next quarter absent de-escalation. Airports and carriers that can pivot volume to alternative East-West chokepoints (e.g., IST, DOH alternatives, or enhanced long-haul via Northern routings) will capture transient yield uplift; those tied to a single superhub face lasting revenue erosion if insurers or corporate travel policies restrict routes for months.

On timeframes, expect acute disruption over days–weeks with durable commercial effects for 2–9 months if attacks persist or if insurers revise standard terms; a credible diplomatic de-escalation that includes airspace guarantees would reverse most airline and cargo impacts within 30–90 days. The real optionality is in defense-capex and brokered insurance flows — both react with multi-quarter budget and pricing changes that create asymmetric opportunities for equities in defense, cargo integrators and risk brokers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35