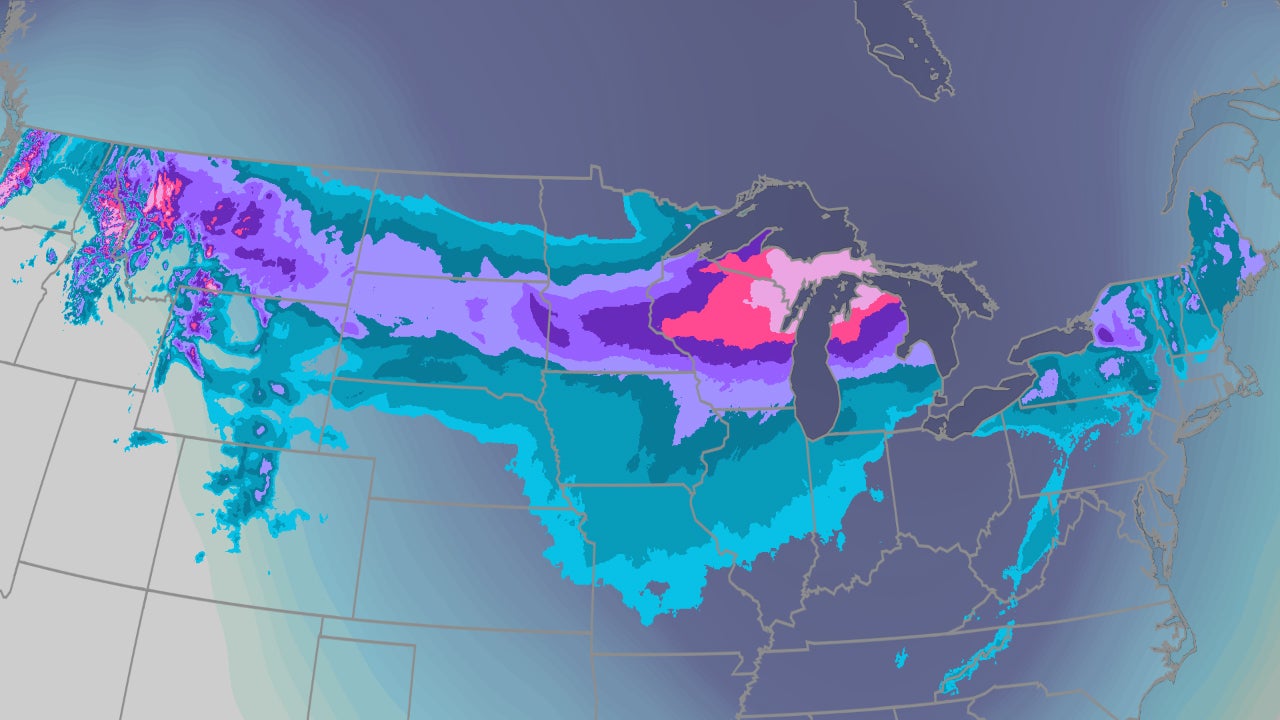

Expect 18–24 inches of snow in parts of southern Minnesota into central/northern Wisconsin and Upper Michigan this weekend, with snow rates of 1–3 in/hr and possible blizzard conditions. Strong winds (gusts up to 123 mph observed in the Tetons; widespread 55+ mph gusts expected) plus heavy snow could cause severe travel disruptions and power outages, raising near-term heating/electricity demand. Arctic air will follow, with subzero lows possible in ND, MN, WI and MI and freezing temps into parts of the Deep South and Florida through midweek; conditions may moderate by mid‑next week but some models hint at a chill returning around Mar 21–22.

Logistics and regional supply chains will see asymmetric friction: Chicago-area rail and distribution hubs and Great Lakes barge traffic face concentrated delays that ripple to outbound refrigerated freight and time-sensitive industrial inputs. Expect spot truckload rates in affected corridors to gap higher for 7–14 days (we model a 5–15% bump) while inventory-sensitive shippers accelerate modal substitution to air/overnight lanes, increasing short-term yields for express carriers but pressuring margins for parcel networks with fixed route density.

Energy and power markets are the more durable story: an abrupt, regionally focused demand shock into a thin storage/flow window amplifies front-month natural gas and day-ahead power volatility in MISO/PJM and Gulf hubs. A 10–25% move in the Henry Hub front-month is plausible inside two weeks if weather-driven withdrawals exceed market expectations; concurrently, merchant gas-fired generators and peaking assets will earn elevated dark spread dollars during outage-induced price spikes.

Transportation equities with concentrated Midwest exposure (airlines with hub operations and Class I rails serving the Great Lakes grain corridor) will see tactical revenue leakage and operational cost adds; this is a transient hit but one that can generate headline-driven share moves in the next 5–10 trading days. Conversely, equipment and services tied to outage mitigation (backup generators, rental power, emergency road services) will see a sharp, short-dated revenue pop that is easily missed by consensus focused on passenger disruption.

The market consensus underweights commodity and infrastructure basis moves versus headline travel disruption. The higher-probability path is a fast, concentrated economic reallocation — elevated gas/power spreads and short-lived freight price dislocations — rather than persistent demand destruction. Trade implementation should therefore prioritize short-dated option structures and basis trades that monetize volatility and localized price dislocations, not long-duration directional bets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35