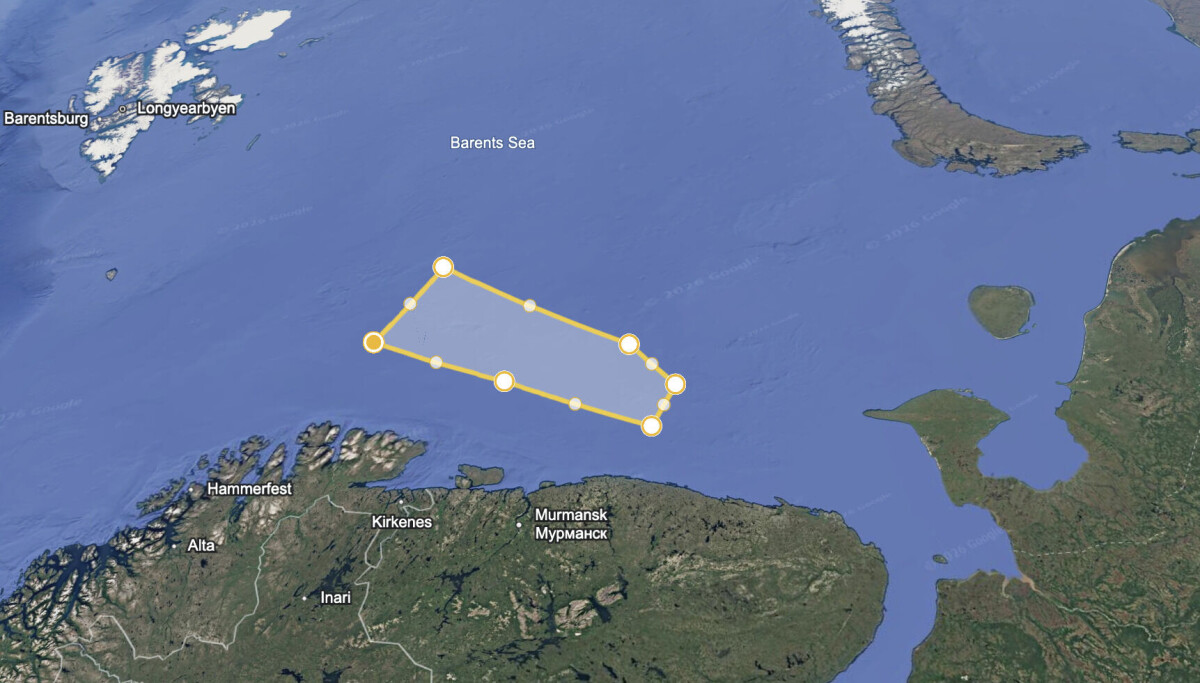

Russia’s Northern Fleet has notified civilian aviation and maritime authorities of planned missile firings in a Barents Sea danger area that spans the Russian–Norwegian maritime border, active from 01:00 on Feb 24 until 14:00 on Feb 26 (Moscow time), with the westernmost edge north of Norway’s Varanger Peninsula and inside Norway’s EEZ/international waters. The fleet did not specify missile type or participating vessels; the notice echoes a February 2022 Tsirkon launch and is seen as possible signaling to Norway and NATO rather than necessarily indicating an imminent strike. The warning raises localized security risk for shipping and Arctic energy logistics and keeps regional defense readiness elevated ahead of NATO’s Cold Response exercises, warranting monitoring of defense-sector exposures and Arctic transport routes for potential second-order market impacts.

Market structure: Near-term winners are large defense primes (Lockheed LMT, Raytheon RTX, Northrop NOC) and Arctic-capable energy producers (Equinor EQNR, Shell RDS.A) that gain pricing power on higher NATO/sovereign capex and risk premia in upstream projects; losers include Arctic logistics/shipping, insurers and regional tourism/airlines (DAL, UAL). Supply/demand: a transient demand shock for missile systems, surveillance and Arctic logistics services will lift order visibility for 6–18 months and compress supply of specialized naval munitions and ship-escort capacity, implying 5–15% margin expansion for niche defense contractors. Cross-asset: expect a 2–5% knee-jerk rally in Brent/TTF gas, a 1–3% rise in gold (GLD), safe-haven flows into USTs and USD, and a VIX spike +20–40% intraday if launches occur near NATO exercises. Risk assessment: Tail risks include mis-fired missiles or collision causing NATO escalation and sanctions widening — low probability (5–10%) but >20% equity drawdowns in regional operators; a blockade or insurance shock for Arctic routes is lower probability (<5%) but could spike shipping rates 30–50%. Timing: immediate (days) = volatility and bid/ask widening; short-term (weeks–months) = defense order re-rates and energy risk premia; long-term (quarters–years) = sustained Arctic militarization driving multi-year capex. Hidden deps: European gas prices depend on LNG tanker availability and port ice conditions; defense wins depend on fiscal approvals (NATO budget cycles) not just headlines. Catalysts: NATO policy statements, Cold Response exercise outcomes, or a verified launch will accelerate repricing. Trade implications: Direct plays — establish 2–3% long positions in LMT and RTX (split) with 6–12 month targets +10–18% and 12% stop-loss; add 1–2% long EQNR for energy/Arctic optionality with 6–18 month horizon. Hedging — buy 30-day at-the-money VIX calls equal to 0.5% portfolio notional to protect against a 20–40% vol spike; alternatively buy GLD (1–2%) if geopolitical risk persists >2 weeks. Pair trades — long LMT / short DAL 1:1 (1–2% net exposure) to capture defense upside vs travel downside; use 3–6 month call spreads on primes rather than outright equity to limit downside. Entry/exit — enter VIX/gold immediately, stagger defense buys over next 4–8 weeks on pullbacks >5%; trim positions if volatility normalizes 20% below peak or if no escalation within 30 days. Contrarian angles: The market may overprice persistent escalation; historical parallels (Feb 2022 Barents launches) produced short-lived commodity and defense rallies that mean-reverted within 3–6 months once no further escalation occurred, so favor option-defined upside (call spreads) over levered longs. The consensus ignores higher insurance/shipping cost drag on Arctic energy projects — a crowded long in EQNR could be vulnerable if insurance premiums rise >25% and delay projects by >6 months. Unintended consequence: a spike in defense stocks could prompt political pushback on procurement budgets in some NATO countries; cap gains within 6–12 months are plausible but payout risk exists if fiscal approvals stall, so size positions accordingly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35