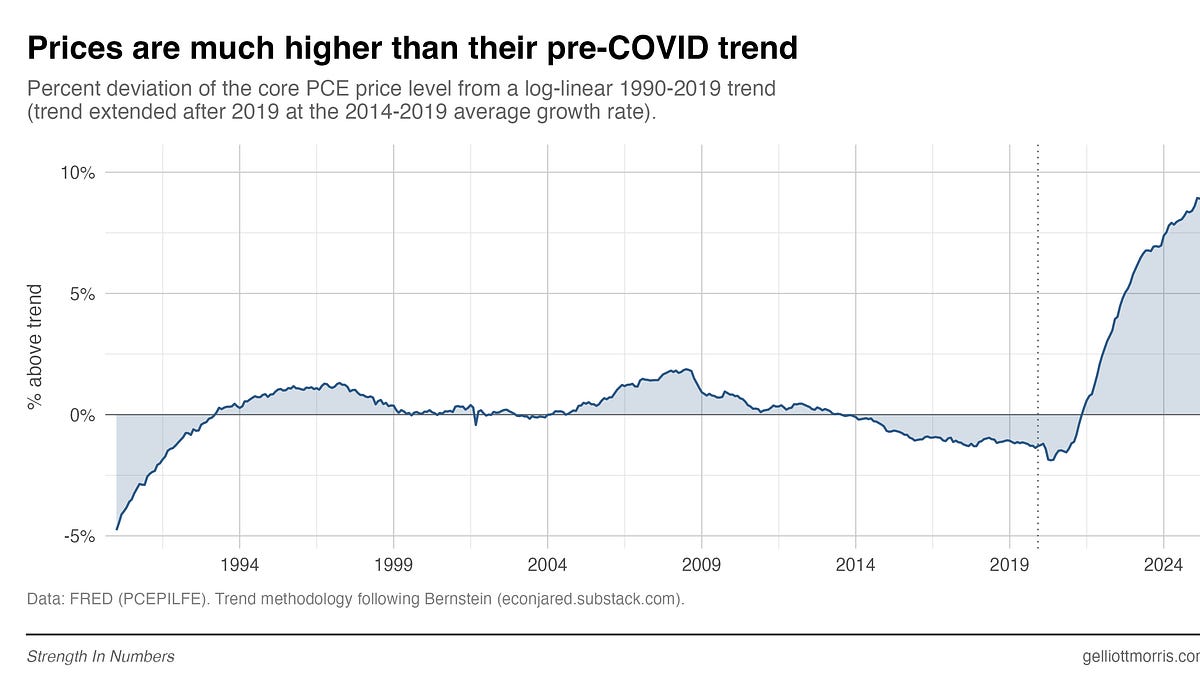

The article argues that the University of Michigan consumer sentiment collapse is driven primarily by persistently high price levels, not just news coverage or headline inflation. It says models using cumulative price shocks or survey-based price anxiety explain the post-2020 sentiment gap far better than unemployment, CPI, the S&P 500, or media sentiment, with mean absolute error falling to 4.7-5.8 index points versus much larger misses for standard macro models. The piece also frames the issue as politically relevant, suggesting high prices remain the key source of household frustration despite improving inflation rates.

The key investable takeaway is not simply that inflation matters, but that households anchor on the price level with a long memory. That implies the disinflation narrative can improve headline macro prints without repairing confidence, which is a bad setup for consumption-sensitive equities if wage gains are only offsetting elevated baskets rather than restoring purchasing power. The second-order effect is political: if voters are reacting to cumulative price pain, any asset tied to “soft landing” optimism may be more fragile than consensus assumes into the next earnings and election cycle.

This is most relevant for retailers, discretionary, autos, and consumer credit. Elevated sticker prices tend to force mix-down behavior first, then unit compression, then private-label/trading-down share gains; that sequence favors value grocers, off-price, discount chains, and essentials over premium brands and big-ticket cyclicals. The article also implies that firms with true pricing power may still report good nominal revenue while volume elasticity quietly deteriorates, so margin optics can stay okay until inventories and promotions expose demand weakness.

The contrarian point is that the market may already be partly pricing the sentiment damage, but not the duration. If price levels remain sticky, consumer confidence can stay depressed for quarters even if CPI looks benign, which matters more for election-year fiscal behavior, consumer lending, and guidance than for near-term inflation prints. The reversal trigger is not lower inflation; it is visible relief at the checkout counter and in recurring bills, meaning a broad-based drop in food, shelter, insurance, and utility inflation would matter more than another soft CPI headline.

For positioning, the asymmetry is better expressed as relative consumer exposure rather than outright market beta. The setup favors shorts or underweights in premium discretionary and credit-sensitive names versus longs in value/essential spend beneficiaries, with the risk that stronger nominal wage growth temporarily masks the volume decline. If consumer sentiment remains unanchored while rates stay elevated, lenders and retailers with weaker customer bases will likely see the first earnings downgrades.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.05