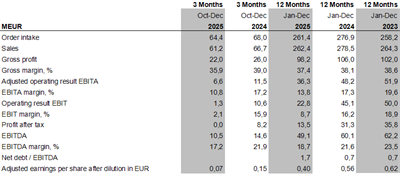

Troax reported weaker demand and lower profitability in Q4 and FY 2025: Q4 order intake fell 5% y/y to EUR 64.4m and sales fell 8% to EUR 61.2m, with Q4 EBITA down to EUR 6.6m (EBITA margin 10.8% vs 17.2% prior year) and profit after tax at EUR 0.0m (EUR 8.2m prior). For full-year 2025, order intake was EUR 261.4m (-6%), sales EUR 262.4m (-6%), EBITA EUR 36.3m (margin 13.8%) and profit after tax EUR 13.5m (vs EUR 31.3m prior); adjusted EPS diluted EUR 0.40 (0.56) and reported EPS diluted EUR 0.23 (0.52). Management flagged EUR 4.2m of Q4 one-off costs (including EUR 1.7m non-cash impairments) and ~EUR 2.2m additional non-recurring costs expected in H1 2026 related to factory relocations; the board proposes a lower dividend of EUR 0.24 (0.34).

Market structure: Troax is a niche industrial-safety supplier with growing Asia exposure from the Vichnet deal and a US factory move that should lower unit costs long-term. Near-term winners are specialist warehouse/automation suppliers and Asian mesh/cable-tray producers; losers are low-margin commercial partitioning incumbents and under-utilized North American plants. Expect modest market-share gains in Asia over 12–24 months if integration succeeds; pricing power remains limited until volumes recover (need +5–10% y/y to restore FY margins). Risk assessment: Key tail risks are execution delays on the US factory relocation (additional >€2–5m hit), failed China integration (customer churn), and a deeper cyclical shock in automotive leading to another ~10% organic order decline. Time horizons: immediate (days) — market reaction to impairment headlines; short-term (weeks–months) — Q1 order intake and recognition of €2.2m H1 one-offs; long-term (quarters) — margin recovery if volumes and synergies materialize by H2 2026. Hidden dependency: FX (USD/SEK/EUR) and working-capital tied to relocations could stress cash if orders fall >10%. Trade implications: Tactical long-biased exposure to Troax (Stockholm-listed Troax Group AB) is warranted on selective dips because one-offs (~€6.4m across Q4+H1) materially depress reported EBITA but are non-recurring; target a margin reversion to 16–18% to justify 30–50% upside in 12–18 months. Use options to define risk: buy 9–12 month call spreads or protective puts rather than outright leverage given operational risk. Rotate away from pure automotive suppliers into warehouse/automation plays (e.g., KION) over the next 6–12 months. Contrarian angle: The market appears to price permanent margin deterioration despite management guidance that re-shoring and a new US plant will lower unit costs; normalize earnings by stripping one-offs (≈€6.4m = ~2.4% of sales) and you get materially higher adjusted margins. If Troax can achieve modest volume recovery (+3–6% y/y) by Q3 2026 and integrate Vichnet, downside is limited relative to potential upside — a classic post-restructuring small-cap opportunity where timing of recovery (Q2–Q4 2026) is the primary risk.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45