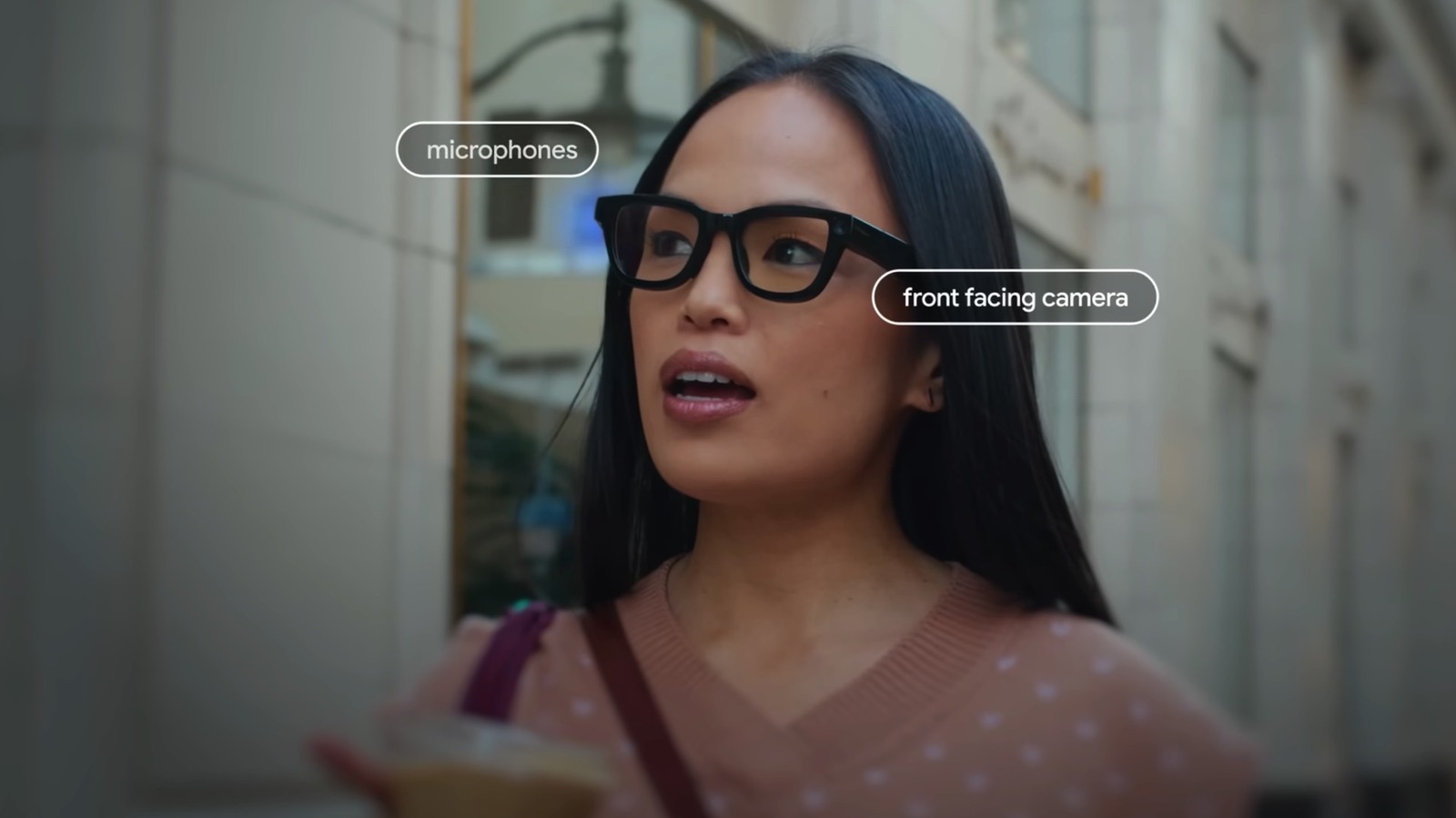

Google's first commercial AI smart glasses appear increasingly likely to launch around I/O 2026, with Android XR positioned as the core platform for voice-first wearable computing. The article highlights multiple product paths, including display-less and display-equipped glasses, plus partners such as Warby Parker, Gentle Monster, Kering, and Samsung. No pricing or launch date is official yet, but the report reinforces Google's push into wearable AI and intensifies competition with Meta, Apple, and OpenAI.

This is less a one-off device story than an attempt to turn Android XR into a platform tax on the next wearable cycle. If Google gets even a credible launch window, the first-order beneficiaries are the component and distribution layers, but the second-order winner is Google’s own search/assistant monetization: glasses increase query frequency, context richness, and default-utility capture in a way phones no longer can. That matters because a voice-first wearable shifts the battle from app icons to ambient intent, where Google is structurally stronger than point-solution competitors.

The biggest near-term read-through is for WRBY, not because eyewear fashion suddenly becomes secular tech beta, but because brand distribution and lens manufacturing become the gating factor for consumer adoption. If Google wants scale, it needs trusted retail/channel partners to lower return rates and normalize a category that still feels experimental; that creates real option value for Warby if Google chooses co-marketing and exclusive early SKUs. QCOM also benefits asymmetrically: even modest success in AI glasses validates a low-power edge compute stack and extends the life of AR1-class silicon into a multi-year refresh cycle.

META is the most exposed to a widening of the product roadmap. The market already assumes Meta owns consumer smart glasses momentum, but a Google launch compresses that narrative from “category leader” to “category duopoly,” which can cap multiple expansion if the hardware thesis is re-rated as platform competition rather than a single-vendor land grab. Apple is the longer-dated risk: if Google establishes a habituated daily-use form factor before Apple ships, Apple’s entry will face higher switching friction and lower novelty premium, especially if Google’s integration with Maps, Translate, and messaging proves sticky.

The contrarian angle is that the setup may still be too early for headline revenue impact, so the stock reaction could be more about option value than EPS. The real tell will be whether Google frames glasses as a distribution endpoint for Gemini rather than a hardware margin story; if so, market enthusiasm can persist even on low initial volumes. The main reversal risk is execution failure on comfort, battery life, and privacy perception—if those issues dominate demos, the launch becomes a platform tease rather than a demand inflection, and the benefit shifts back to incumbents with already proven form factors.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment