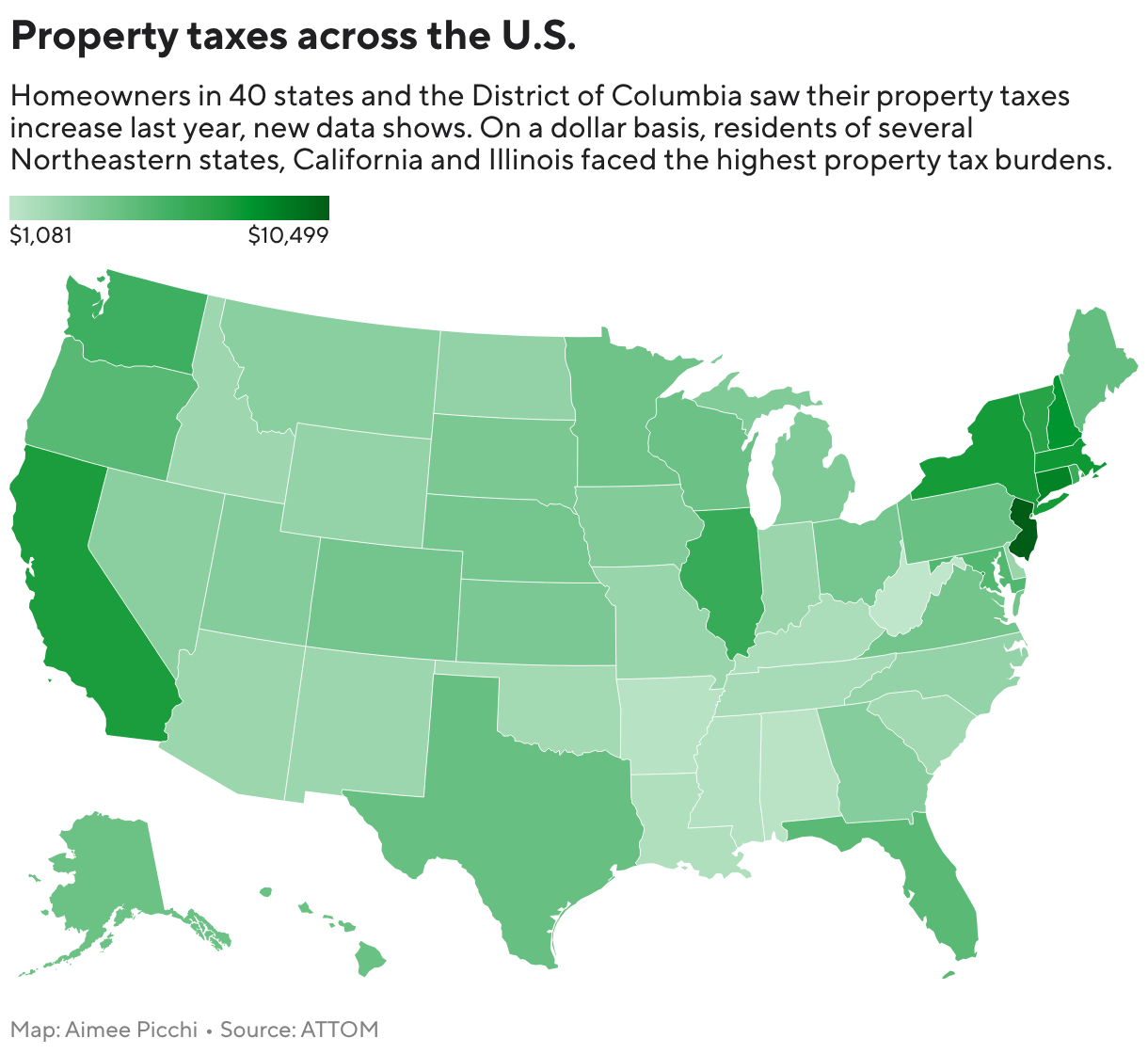

Average US homeowner paid $4,427 in property taxes last year, up 3.7% from 2024, outpacing CPI inflation of 2.7%. Some states saw much larger increases (Delaware +18%, Maryland +11.6%); 40 states plus DC had tax rises while 10 states — largely in the West — saw declines driven by policy (e.g., Wyoming approved a 25% cut for properties ≤ $1M, Montana enacted rebates/tiered system). Average single-family home value dropped 1.7% to $494,231, indicating tax growth is driven by local budget needs and legislative actions rather than uniform assessment gains; highest average taxes in New Jersey (~$10,500) and lowest in West Virginia (~$1,081).

Municipal budgets are the proximate driver here, not home-price inflation: jurisdictions are increasing effective tax rates or levies to cover structurally higher recurring costs (pensions, wages, public-safety overtime). That dynamic compresses housing turnover—higher carrying costs reduce move propensity—so expect lower transaction volumes and a multi-quarter drag on mortgage origination, title, and brokerage fee pools even if headline home values stabilize. Geography matters more than aggregate averages. States that both tax heavily and are losing net migration (Northeast, parts of the Midwest) face compound downside: population outflows amplify the tax burden on remaining homeowners and create a feedback loop that weakens local housing demand and rental growth. Conversely, low-tax energy/tourism upswings (WY, MT, ID) can create outsized fiscal slack and become tactical beneficiaries when commodity or tourism cycles re-accelerate. Credit and rates channel: rising property taxes reduce near-term fiscal default risk for munis (more revenue), but they also raise political risk of ballot-driven caps or state preemption in off-years. That makes muni spreads sensitive to state legislative calendars and midterm elections; expect volatility spikes around those events rather than steady compression. From a corporate angle, lower transaction volumes hit mortgage lenders, title insurers, and regional brokerages before national builders and national retailers, creating a staggered earnings hit across the housing ecosystem.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

0.00