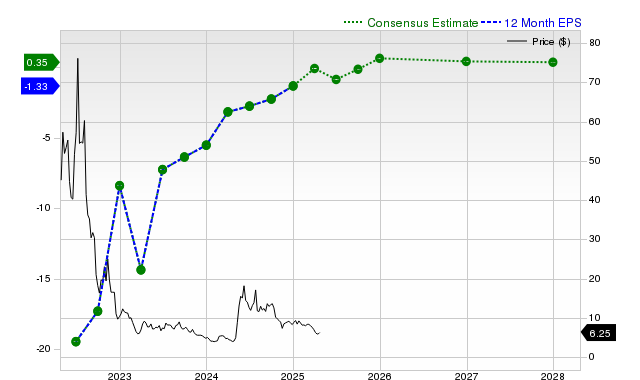

Novavax (NVAX) has recently trended, outperforming the S&P 500 with a 7% gain over the past month. While the company has consistently beaten recent earnings and revenue estimates and is projected for significant current fiscal year EPS growth to $2.66 (+316.3% Y/Y), analysts anticipate a sharp decline in the next fiscal year's EPS to $0.27 (-89.9% Y/Y) alongside a projected 46.9% revenue drop. Despite a 'B' valuation score suggesting it trades at a discount to peers, Zacks maintains a 'Hold' (#3) rank, implying near-term performance in line with the broader market.

Novavax (NVAX) has exhibited significant near-term strength, with its shares returning +7% over the past month, substantially outperforming both the S&P 500 composite's +1.3% gain and its own industry's +2% rise. This momentum is supported by a history of substantial outperformance against consensus, including a +102.74% revenue surprise and a +985.71% EPS surprise in its last reported quarter. The outlook for the current fiscal year remains robust, with analysts forecasting a +51.2% revenue increase to $1.03 billion and a +316.3% surge in EPS to $2.66, an estimate that has been revised upward by 7.3% in the last 30 days. However, this positive trajectory faces a sharp reversal in the next fiscal year, for which consensus estimates project a -46.9% revenue decline to $547.58 million and a dramatic -89.9% collapse in EPS to $0.27. This negative outlook is reinforced by a recent -5.3% downward revision to next year's EPS estimate. Despite a 'B' grade for valuation suggesting a discount relative to peers, the Zacks Rank #3 (Hold) indicates that the stock is expected to perform in line with the broader market, reflecting a balance between its current-year growth and the severe contraction anticipated thereafter.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.15

Ticker Sentiment