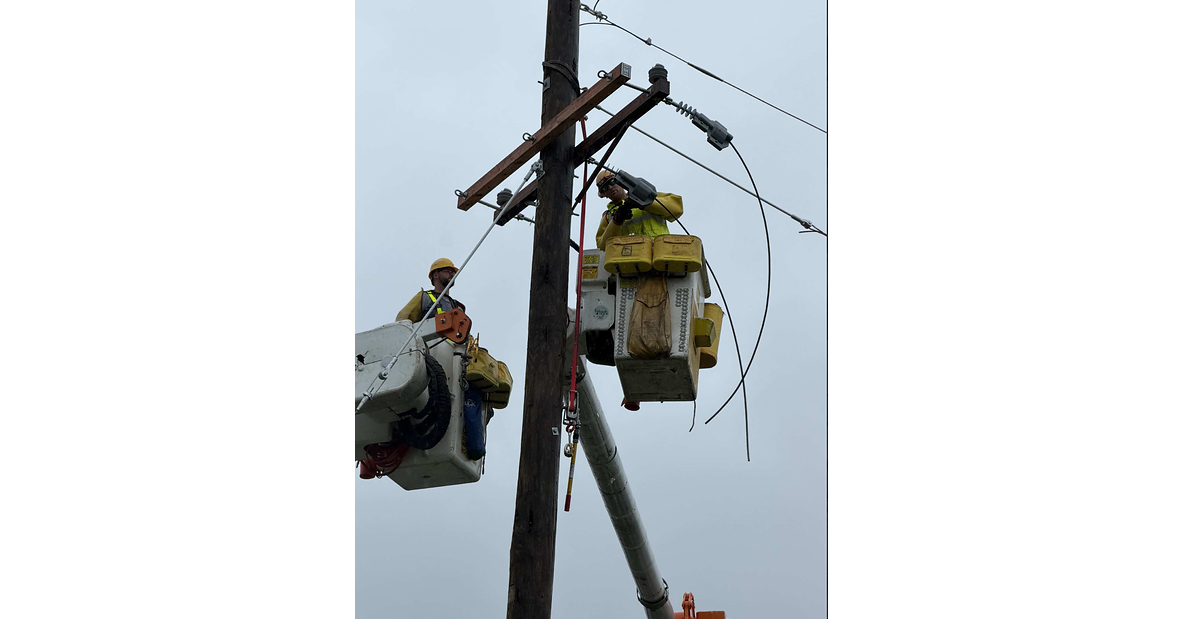

PSE&G restored power to more than 380,000 customers after a week of extreme weather (heat dome and winds over 70 mph), with nearly all customers back before midnight on July 7 and the last two restored at 2:00 a.m. on July 8. The restoration effort included replacing or repairing ~700 utility poles, clearing 1,500+ trees, completing 7,000+ A/C repairs, deploying 165 utility crews (including mutual aid), and sending 10M+ customer messages. The article frames the outcome as a successful operational response supported by prior system modernization, with no specific financial metrics cited.

This is not an earnings event so much as a credibility event. For PEG, the economic upside from a large storm is usually indirect: regulators and local officials see proof that the grid can be restored quickly, which strengthens the case for recovering storm-related spend and for more capital-intensive hardening programs later. The bigger financial lever is not this week’s restoration cost, but whether management can convert resilience into a larger authorized rate base over the next 1-3 rate cycles. The second-order winner is the utility ecosystem around emergency response, but the investable implication is mostly for PEG’s future capex path. If this storm becomes part of a broader pattern, PEG’s maintenance and replacement spend should rise faster than normalized load growth, which is mildly positive for earnings if regulators allow timely recovery and mildly negative if they push back on customer bills. In other words, the stock benefits more from constructive rate treatment than from the storm itself. Near term, the market should treat this as noise unless there is evidence of material asset damage, uninsured costs, or a slower-than-usual restoration tail. The real catalyst is the next rate-case or storm-recovery filing: that is where cost pass-through, allowed ROE, and depreciation treatment will matter. The contrarian risk is that investors overpay for the reliability narrative; if storms are becoming more frequent, the political debate can shift from ‘good operator’ to ‘why are bills rising,’ which caps multiple expansion for PEG and peers. I do not see a strong immediate short or long from the headline alone. The cleanest setup is to watch for a temporary dip in PEG if the market assumes higher storm costs without corresponding recovery. Falsifiers are simple: if management signals unrecoverable storm expense, delayed filings, or a regulator becomes more consumer-protective than expected, the thesis on constructive rate-base growth weakens quickly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.10

Ticker Sentiment