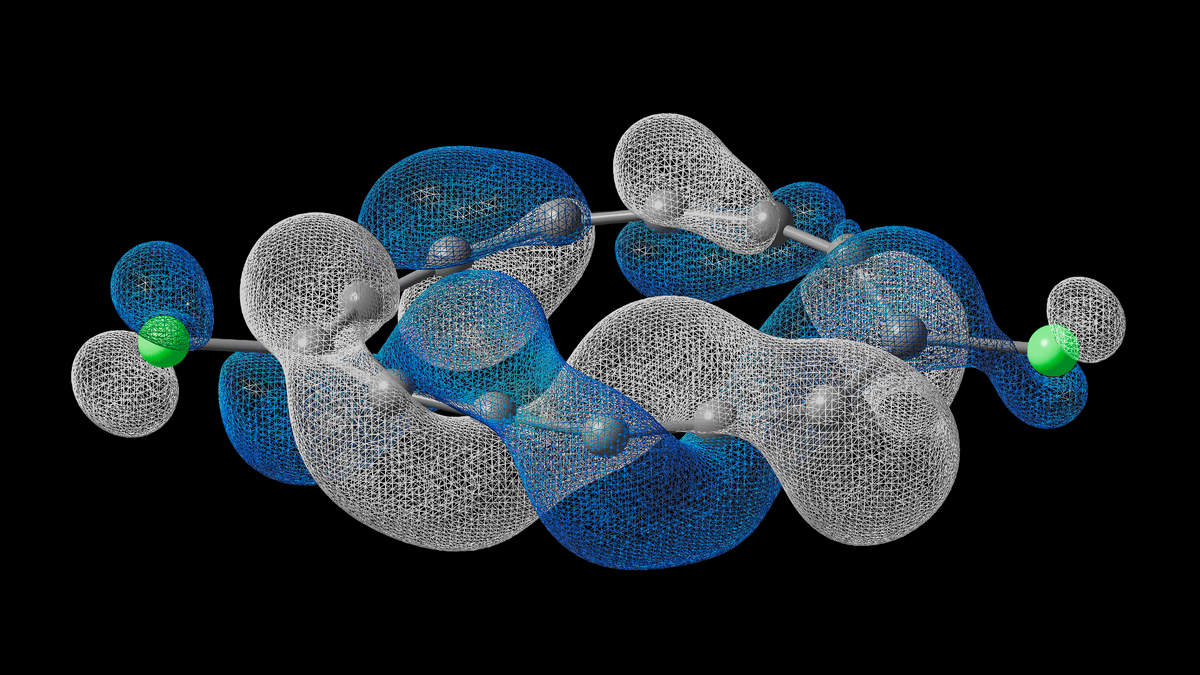

IBM Research has synthesized a novel 'half‑Möbius' molecule by manipulating individual atomic bonds and imaged it with advanced microscopy, then validated the structure using IBM's quantum computers and classical simulations; the work was published in Science. The experiment demonstrates a practical application of quantum simulation for complex topological chemistry and highlights IBM's progress in scaling qubit capacity, signaling incremental strategic and technological value rather than immediate financial impact.

Market structure: IBM (IBM) is the direct beneficiary of positive narrative and IP/branding lift; expect a modest re-rating opportunity—potential 3–7% relative outperformance vs. large-cap tech over 1–6 months if IBM ties this to product/roadmap milestones. Downstream winners include quantum software partners and microscopy/IP licensing buyers, while classical HPC incumbents see only marginal competitive threat because the molecule is non-commercial and lab-bound. Cross-asset: expect short-term bump in IBM equity vols (+10–25% IV) and a 5–15bp tightening potential in IBM credit spreads if the story persists, negligible FX/commodity impact.

Risk assessment: Tail risks: reproducibility failure, quantum hardware setbacks, or a PR-driven funding pullback could erase narrative gains (>20% downside for momentum positions). Time horizons split: immediate (days) = IV/PR spike; short-term (weeks–months) = investor re-rating tied to IBM Q announcements; long-term (years) = IP commercialization if error-correction and qubit scale reach commercial thresholds (e.g., >1,000 logical qubits). Hidden dependency: this is lab-only chemistry; commercial scale requires separate materials, manufacturing and stable error-corrected QPUs.

Trade implications: Constructive but size-limited exposure to IBM: primary trade is a small equities core position (2–3% portfolio) plus convex LEAPS via call spreads to cap cost (12–24 month expiries). Consider pair trade: long IBM vs short traditional IT services (e.g., Accenture ACN) to isolate quantum/innovation premium. Use options tactically around catalysts: buy 3–6 month call spreads ahead of IBM quantum roadmap updates and sell 30–60 day covered calls to harvest IV after rallies.

Contrarian angles: Consensus will overestimate near-term commercial impact—this is likely under-monetizable for 3–5 years—so pure story plays may be overdone. Conversely, the market underprices strategic/defensive value: IBM could monetize IP/licensing and talent capture, producing steady EPS lift of low single digits over 2–4 years if roadmaps progress. Historical parallel: IBM Watson drove PR but limited revenue; use that to size positions and demand measurable product/margin inflection before adding risk size.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment