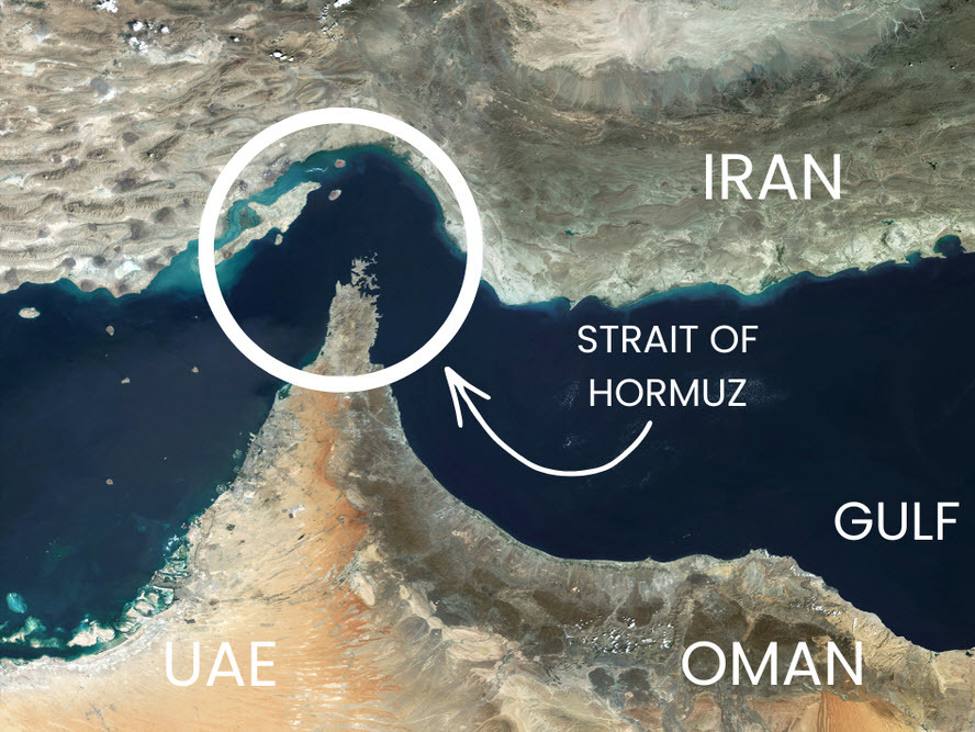

WTI crude jumped to $107.70 (up $16.80 on the April contract), roughly a 55–65% year-over-year rise and nearly double February levels. Risk assets are under pressure: the S&P 500 fell 1.3% on Friday with futures down ~1.4% at the open, gold flipped and is down about $25, while 10-year Treasury futures are down 10 ticks and 30s down 19 ticks. Iraq signaled a production cut of ~3 million barrels per day and ~20% of global flows through the Strait of Hormuz are effectively offline, pushing retail gasoline toward $4/gal and contributing an estimated 0.3–0.5 percentage points to year-over-year headline CPI, creating immediate inflation headaches for the Fed and other central banks.

The immediate transmission is not just higher headline inflation but a re-pricing of margin capture across the hydrocarbon value chain: upstream producers economically capture most incremental dollars while downstream users — airlines, container shipping, and petrochemical processors — face margin compression and pass-through lags that amplify demand destruction risks. Refiners with advantaged access to inland crudes or export parity positions will arbitrage global dislocations and can see near-term windfalls, while coastal refiners dependent on seaborne crude may face input squeezes and volatile crack spreads.

From a macro-market perspective, this is a classic stagflation shock in miniature: breakeven inflation expectations can jump quickly, but nominal yields may not climb enough to fully price in higher real rates, leaving real yields volatile and central banks between a rock (inflation overshoot) and a hard place (growth hit). Expect two distinct decision windows: the first 0–8 weeks dominated by tactical positioning, volatility and policy signaling; the 2–9 month window where supply responses (U.S. shale reactivation, non-OPEC flows) and demand elasticity (industrial cutbacks, modal shifts) materially change the supply/demand balance.

Catalysts that would reverse the current move are political/diplomatic de-escalation, coordinated emergency releases from strategic inventories, or a sharp global growth downdraft that erodes oil demand faster than supply normalizes. Conversely, protracted chokepoints or secondary producer outages keep a higher-for-longer regime. Position sizing should treat current moves as information-rich but mean-reverting over quarters — trade volatility and policy outcomes, not an unbounded structural regime change without monitoring clear catalyst thresholds.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.70