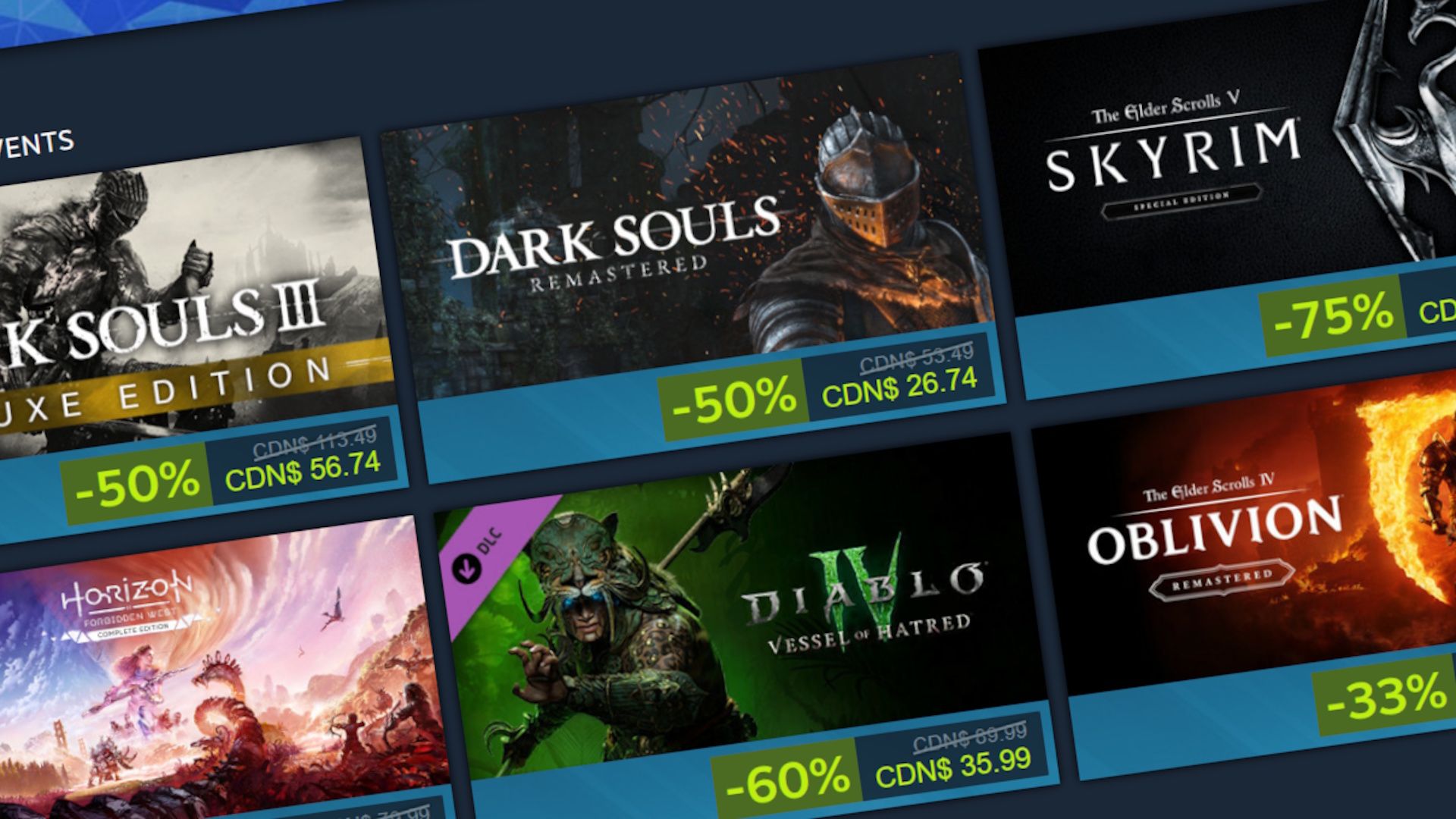

Valve launched its first-ever one-week Steam Black Friday sale running through December 1, featuring notable discounts such as Warhammer 40,000: Space Marine 2 at 60% off to $24/£22/€24, Battlefield 6 at 15% off to $59.49/£51/€59.49, Dying Light: The Beast at 20% off to $48/£40/€48, FEAR bundled at $2/£1.39/€1.79, and the 256GB LCD Steam Deck discounted 20% to $319/£279. The timing follows an earlier-than-usual Autumn Sale (moved to avoid proximity to the Winter Sale) and a Winter Sale start date of December 18, indicating a shift in Valve's seasonal promotional cadence that could modestly concentrate late-November consumer spend toward Valve's digital and hardware sales.

Market structure: Valve’s shift to more frequent, targeted mid-season promos raises take-rate leverage for its storefront and hardware, transferring incremental late-November spend away from physical retail and single-price new releases toward digital catalog and attach monetization (microtransactions/DLC). Winners are digital-native publishers and platform-layer suppliers (AMD exposure via Deck SOC), losers are brick‑and‑mortar gaming retail and margin‑sensitive console hardware incumbents facing ASP pressure. Pricing power for full‑price new releases erodes modestly (low‑double digit discount expectations during key windows), while recurring‑revenue models gain relative share over a 3–12 month horizon. Risk assessment: Tail risks include regulatory action on platform fees in the EU/US (probability low‑mid but high‑impact) and supply shocks for semi suppliers that could inflate component costs (+10–20% wafer prices scenario). Immediate effects (days) are user engagement spikes; short term (weeks–months) are revenue mix shifts and QoQ beat/miss noise; long term (1–2 years) is structural pricing normalization around recurring monetization. Hidden dependency: publishers’ lifetime value assumptions — a 5–15% jump in active users is needed to offset a typical 20–60% initial price cut. Trade implications: Prefer small, tactical allocations: buy AMD (AMD) exposure for 3–9 months to capture modest Deck volume and SoC refresh tailwinds, and buy EA (EA)/ATVI options to play live‑service upside; short/underweight GameStop (GME) and select retail ETFs (XRT) for 1–3 months to capture digital share shift. Use 3‑month call spreads to cap premium and 30–60 day put hedges on retail shorts; initiate within 2 weeks and trim if position outperforms benchmarks by >5% or user metrics disappoint by >3%. Contrarian angles: Markets may underprice long‑term benefit to live‑service publishers — back catalog monetization and larger user funnels can lift recurring revenue 5–10% annually if price erosion is offset by higher conversion. Conversely, the sell‑off in physical retail could be overdone given dedicated collector/used‑game demand; short sizes should be small and stop‑loss disciplined. Historical parallels: prior Steam sales depressed initial revenue but increased lifetime spend; expect temporary headline misses to create entry points over the next 1–3 quarters.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30