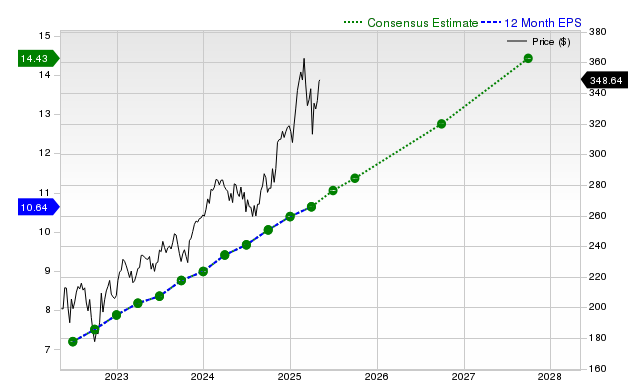

Despite underperforming the S&P 500 and its industry over the past month with a -1.4% return, Visa (V) remains a highly searched stock with strong fundamental projections. The global payments processor is forecast for robust earnings growth, with current quarter EPS expected to rise 17.4% to $2.84 and current fiscal year EPS up 12.9% to $11.35, complemented by over 10% revenue growth projections for both current and next fiscal years, consistent with recent quarterly beats. Zacks has assigned Visa a Rank #2 (Buy), suggesting potential near-term market outperformance, although its 'D' valuation grade indicates it trades at a premium relative to peers.

Visa (V) presents a dichotomy between its recent market performance and its strong underlying financial outlook. The stock has underperformed, returning -1.4% over the past month against a +5% gain for the S&P 500 composite. However, fundamental projections remain robust, with consensus estimates pointing to significant growth. For the current quarter, EPS is forecast to increase by 17.4% to $2.84 on a 10.7% rise in revenue. This growth trajectory is expected to continue, with full-year EPS projected to grow by 12.9% and 12.5% for the current and next fiscal years, respectively, on sustained double-digit revenue growth. This outlook is supported by a strong track record of execution, including beating consensus EPS estimates in each of the last four quarters. Despite these positive indicators and a Zacks Rank #2 (Buy) suggesting potential near-term outperformance, a key consideration is the stock's valuation. Visa receives a 'D' grade for value, indicating it trades at a premium to its peers, a factor that likely contributes to its recent price sensitivity.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment