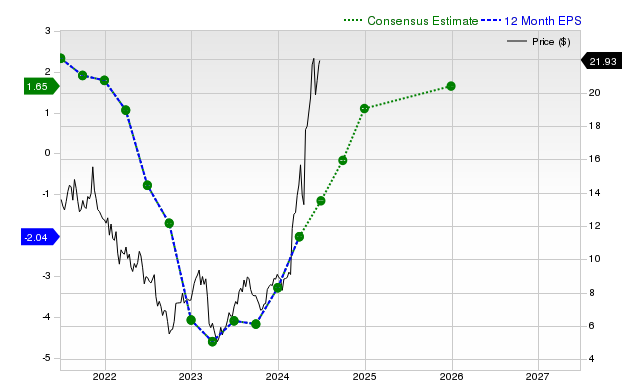

Tutor Perini reported revenue of $1.42 billion in the last quarter, up 30.7% year‑over‑year, and EPS of $1.15 versus -$1.92 a year earlier, beating the Zacks consensus revenue of $1.34 billion (+5.34% surprise) and delivering an EPS surprise of +19.79%. Zacks consensus now forecasts current‑quarter EPS of $0.92 (+160.9% YoY), FY EPS of $4.01 (+228.1%) and next‑fiscal EPS of $4.72 (+17.7%), with revenue estimates of $1.28 billion for the quarter and $5.32 billion / $5.98 billion for the current and next fiscal years; the stock carries a Zacks Rank #2 (Buy) and an A value style score, suggesting perceived upside relative to peers.

Market structure: Tutor Perini (TPC) is positioned to capture near-term share in large civil/infrastructure work as consensus revenue estimates imply +22.8% FY growth and backlog conversion accelerating; direct beneficiaries are Tier‑1 contractors with healthy balance sheets and specialty subcontractors (concrete, heavy civil). Losers are regional/low‑margin contractors and private real‑estate developers squeezed by higher financing costs. Cross‑asset: stronger TPC fundamentals should tighten credit spreads for mid‑credit contractor paper, lift sector implied vols into earnings, and push modest upside pressure on steel/cement prices over quarters as project demand ramps. Risk assessment: Tail risks include a single large program loss or change‑order reversal (> $100–200m) that would swing EPS by multiple dollars, government funding pauses from budget delays, or a liquidity shock if receivables/retentions lengthen; these are highest-probability within the next 3–9 months around contract settlements. Hidden dependencies: earnings upside depends on mix (public vs private), working‑capital release, and margin capture on fixed‑price blocks. Catalysts to watch in 30–90 days: quarterly results, backlog re‑state, and new award announcements tied to federal infrastructure funding. Trade implications: Base case — modest long exposure to TPC to capture re‑rating as consensus EPS rises from $4.01 to $4.72 next fiscal year. Prefer capital‑efficient options to lever conviction: 9–15 month call spreads to capture re‑rating while capping downside; pair trades (long TPC vs short FLR or J) exploit relative estimate revision divergence. Entry/exit: scale in on pullbacks ≤5%, take profits at +30% or if consensus EPS falls >10% vs current. Contrarian angle: Consensus underrates backlog quality and working‑cap tailwinds if change orders remain favorable — upside if TPC converts 60–80% of incremental backlog within 12 months. Conversely, market may be underpricing clawbacks on fixed‑price projects; historical parallels (contractor re‑rates followed by margin compression) argue position sizes should be measured and contingent on near‑term FCF and backlog disclosures.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment