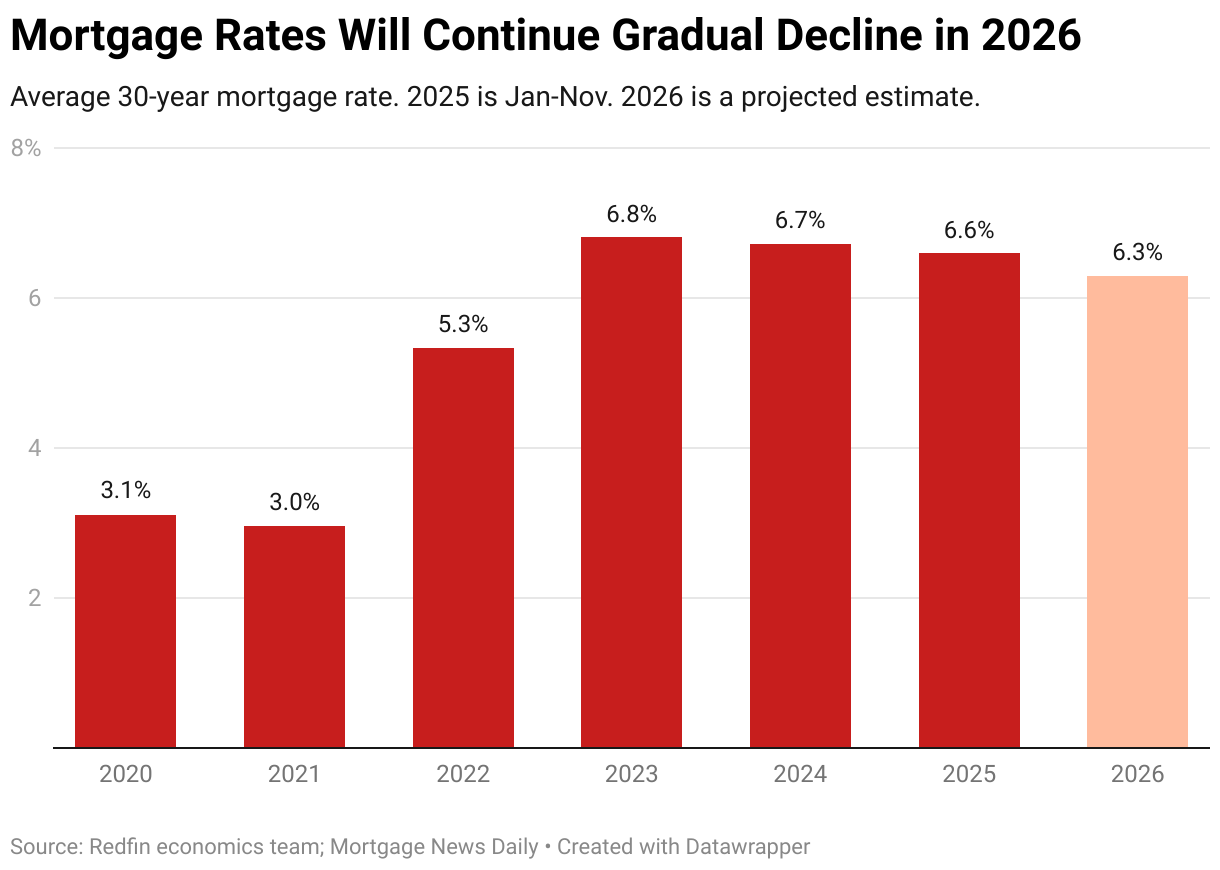

Mortgage rates are forecast to average 6.3% in 2026 (down from a 2025 average of 6.6%) while median U.S. home-sale prices are expected to rise just 1% year-over-year, producing a gradual affordability improvement as wages outpace price growth. Existing-home sales are predicted to rise 3% to a 4.2 million annualized pace, rents to increase about 2–3%, and refinance volume to jump over 30% to roughly $670 billion as ~20% of mortgaged homeowners carry rates above 6% and the typical mortgaged owner held $181,000 of untapped equity mid-2025. Policymakers are likely to advance YIMBY, ADU and manufactured-housing measures while climate risk and AI-driven labor shifts will reshape regional demand, implying a slow multi-year normalization rather than a sharp price correction.

Market structure: The 2026 ‘Great Housing Reset’ favors incumbents that collect fees and carry rate sensitivity—mortgage originators/servicers, agency MBS holders, and multifamily/SFR landlords—while large homebuilders and Sunbelt coastal sellers face pricing pressure. Slow price growth (+1% median price) with wages outpacing prices and a modest sales rebound (+3% to ~4.2M) implies demand recovery is supply-constrained (fewer listings, slower new construction) and will preserve pricing power for well-capitalized holders of existing assets. Risk assessment: Key tail risks are a sharper-than-expected Fed cut cycle (driving a boom and overheating construction) or a macro shock (recession, AI-driven job losses) causing distressed listings; both would upend valuations. Near-term (days–months) drivers: CPI prints, weekly mortgage apps, 10y yield moves; medium-term (Q1–Q3 2026) catalysts: Fed cuts, spring homebuying season, refi volumes; long-term (3–5 years) is gradual affordability normalization. Hidden dependency: municipal zoning reforms (YIMBY) could rapidly increase supply locally and cap homebuilder margins. Trade implications: Favor long agency MBS (relative value to Treasuries), cash-flowing mortgage REITs (AGNC, NLY) and multifamily/SFR REITs (AVB, EQR, AMH) into 2026; underweight national homebuilders (LEN, DHI, PHM) and coastal-exposed REITs in FL/TX. Use option structures around volatility: buy-call spreads on mortgage REITs and buy-put spreads on ITB to capture a slow recovery with rate downside risk. Contrarian angles: Consensus underestimates the refinance/refi-activity uplift (+30% to $670B) that boosts originator servicing income and MBS convexity—this is not a home-price-led recovery but a rate-driven cash-flow story. Homebuilders are priced for a normalizing market; if local zoning reforms stall, builder earnings could surprise down; conversely, rapid YIMBY wins would be a catalyst to short duration MBS and rotate into builders.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25