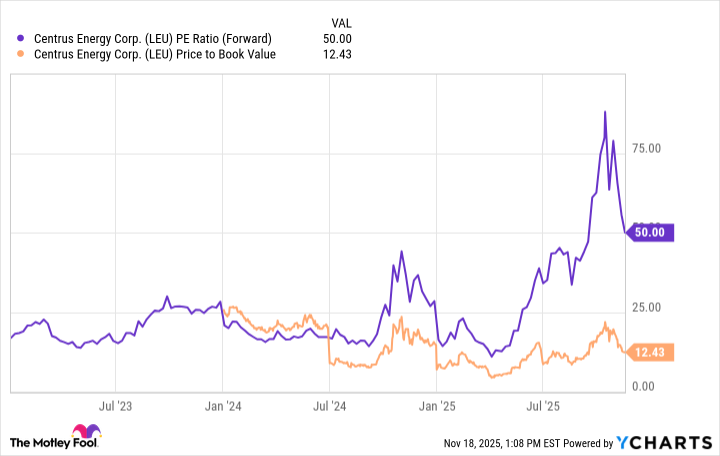

Centrus Energy, one of the few U.S. firms licensed to enrich HALEU, has seen its stock fall roughly 14% over the past five trading days and more than 45% from a mid-October high near $436. The company has begun HALEU production under a cost-shared DOE contract, earning about $7.3 million on a 900 kg delivery in June (roughly 10% of Q3 revenue) and is expected to deliver another 900 kg by June 2026. Despite a unique regulatory position and technical moat, the shares trade at about 12x book and a forward P/E north of 60, implying investor expectations of a smooth production ramp; any major delays could materially disappoint. For risk-tolerant investors this may present a long-term opportunity, while conservative investors may prefer diversified nuclear exposure.

Market structure: U.S. nuclear fuel-service providers and reactor OEMs stand to capture a premium as domestic HALEU capacity tightens, while non-U.S. enrichers lose near-term pricing leverage. Expect spot and term SWU pricing sensitivity; uranium miners and ETFs (e.g., URA, CCJ, DNN) will track commodity moves but avoid single-name operational execution risk. Cross-asset: a delayed ramp would pressure LEU equity vols and widen credit spreads for capex-dependent suppliers; a smooth ramp would lift miners and push modestly higher long-dated yields on project finance while FX moves (USD strength) could mute dollar-denominated commodity returns. Risk assessment: Key tail risks include DOE funding shifts, an operational contamination or license setback, or a multi-quarter ramp delay — any of which could cause >30–50% downside to execution-sensitive equities. Near-term (days) noise will be volatility spikes around DOE announcements; medium-term (3–12 months) hinges on on-time subsequent deliveries and profit cadence; long-term (2–5 years) depends on commercial HALEU offtakes and new reactor build schedules. Hidden dependencies: supply-chain bottlenecks (centrifuge spares, feedstock) and covenant-driven financing that could force equity raises and dilute book value. Trade implications: For growth/volatility seekers, use limited-size LEU LEAP call exposure (12–24 month maturity) to capture upside if DOE milestones are met, with a fixed loss defined at 30–40% of premium. Conservative route: overweight diversified uranium exposure via URA or CCJ (2–4% portfolio) instead of single-firm LEU to capture commodity upside without execution risk. Short/hedge ideas: buy LEU puts or long-vol calendar spreads into the next DOE milestone window; consider a pair trade long URA + short LEU to express commodity appreciation vs. execution risk. Contrarian angles: Market consensus underestimates the strategic value of a U.S. HALEU licensing moat — if Centrus converts licensing into multi-year DOE and utility contracts, upside could be >2x over 18–36 months. Conversely, the market may be underpricing dilution risk and political scrutiny; historical analog: early-stage nuclear supply dislocations have produced both rapid rallies and multi-year drawdowns depending on execution. Watch for insider buying/selling, DOE technical reports, and any equity raises as early signals that will materially re-rate the name.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

0.05

Ticker Sentiment