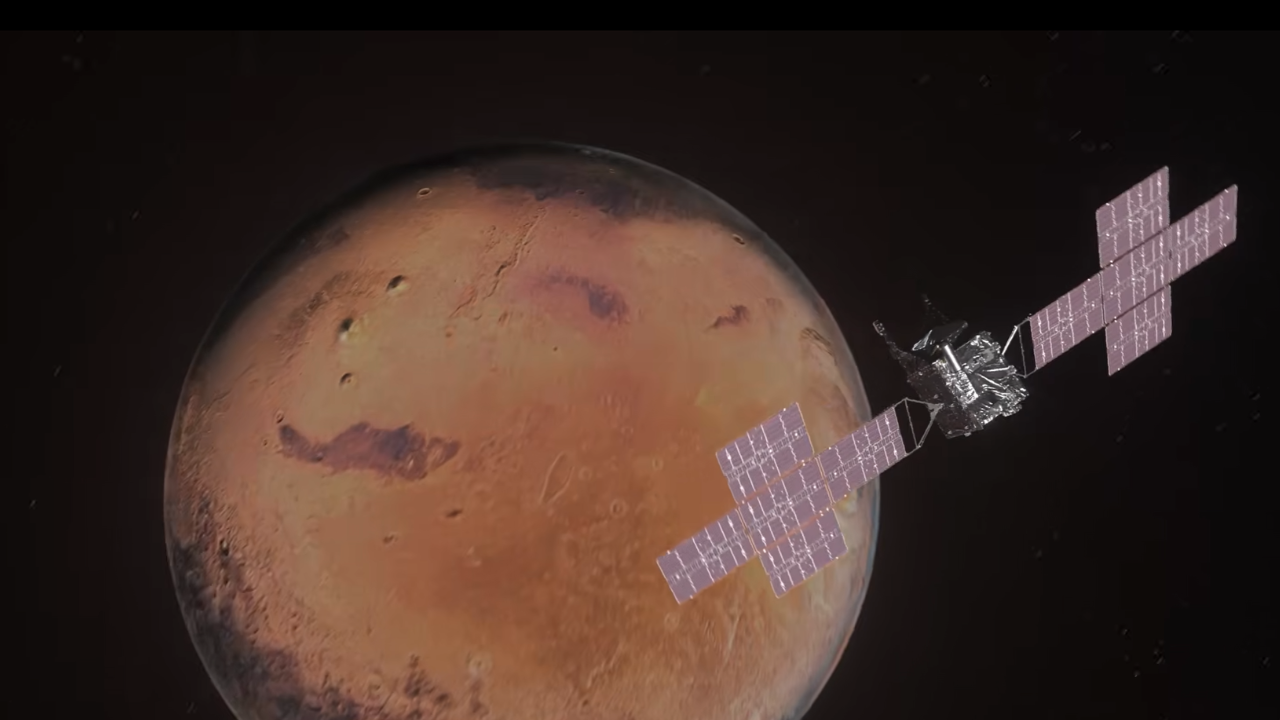

NASA’s Psyche spacecraft completed a Mars gravity assist on Friday, passing within about 2,800 miles (4,500 kilometers) of the planet at roughly 12,333 mph (19,848 kph). The flyby provided an estimated 2-km-per-second change in velocity relative to the sun, conserving fuel and keeping the mission on track to reach asteroid 16 Psyche in July 2029. The article is informational rather than market-moving.

The marketable takeaway is not the flyby itself, but that Psyche just de-risked a multi-year deep-space program without consuming scarce onboard propulsion budget. That matters because the hidden bottleneck in long-duration space missions is often not launch capability, but delta-v margin; any mission that preserves fuel while preserving schedule materially improves program survivability and lowers probability of expensive replans. In other words, this is a validation event for solar-electric plus gravity-assist architecture, which should incrementally support confidence in future small spacecraft and interplanetary infrastructure missions. Second-order, the beneficiaries are less the mission operator than the enabling stack: high-reliability avionics, deep-space comms, solar array, guidance/navigation/control, and electric propulsion suppliers. A successful maneuver also creates a near-term proof point for firms selling mission assurance and trajectory optimization software, because every avoided propellant kilogram can translate into either more science payload, lower launch mass, or a wider target envelope. The competitive implication is that low-thrust spacecraft architectures become relatively more attractive versus brute-force chemical propulsion for missions with long timelines, especially when launch costs remain high. The contrarian risk is that investors may over-interpret one clean trajectory correction as a broad commercialization inflection for asteroid-mining or deep-space logistics. The real monetization window is still years away, and the addressable market depends on repeatable, higher-cadence missions rather than one flagship success. Over the next 6-24 months, the key catalyst is whether this raises win rates for adjacent NASA/commercial contracts; the main reversal would be any navigation or propulsion failure elsewhere that re-prices mission risk and cools procurement appetite. For VOYG specifically, the near-term effect is sentiment-driven rather than fundamental, but it can still matter if the company is exposed to deep-space subsystems or software positioning. The stock should be treated as a catalyst trade, not a secular rerating, unless management can tie this mission class to backlog conversion or margin expansion. If not, the move is likely to fade once the novelty premium dissipates.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.15

Ticker Sentiment