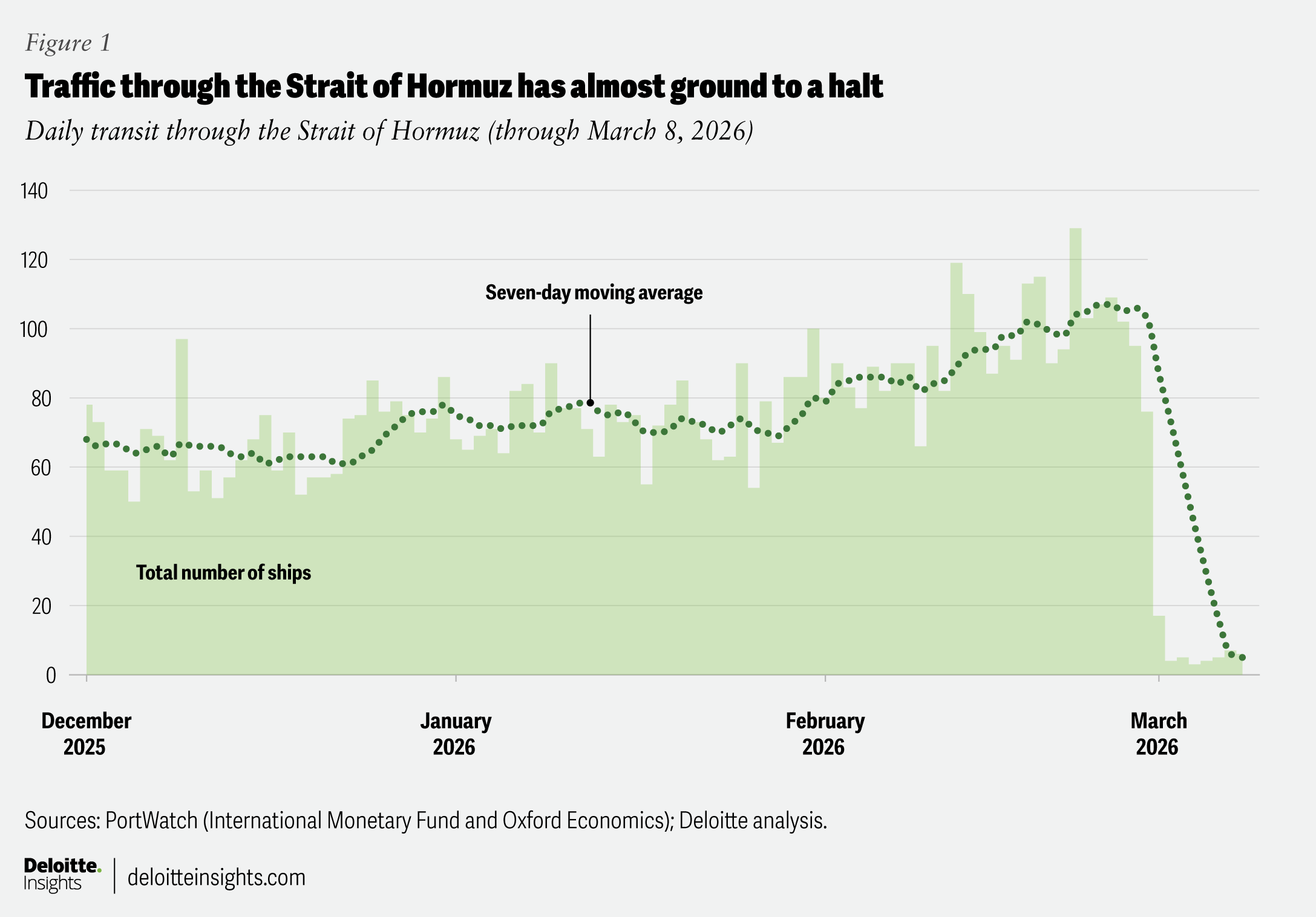

About 20.0 mbpd of crude and petroleum products and 112 bcm of LNG transited the Strait of Hormuz in 2025; roughly three-quarters of oil flows are effectively blocked given alternate-route capacity of only ~3.5–5.5 mbpd and no viable LNG alternatives. Energy market moves have been large: Brent was up 39% from Feb. 27 to Mar. 12, 2026 (briefly above $110/bbl), Dutch TTF gas futures +59%, and Middle East urea futures +34%; 10-year Treasury yields rose ~31 bps over the same period. Expect higher and more volatile energy-driven inflation, upward pressure on yields and borrowing costs, disrupted fertilizer and food supply chains, and fiscal/defense implications for importers and Gulf economies.

The immediate market consequence is not just higher spot energy prices but a durable reshaping of logistics and term structures: shipping reroutes lengthen voyage days and push up time-charter and insurance rates while storage economics become attractive where contango exists. That creates tradable separations between near-term physical tightness and longer-dated paper, and favors flexible holders of floating or onshore storage and owners of LNG tonnage that can redeploy cargoes to higher-paying markets.

Second-order winners are those that capture margin from dislocation rather than directional commodity exposure: reinsurers and specialty marine insurers that can reprice risk, owners/operators of LNG carriers and FSRUs who command premium rates, and select non-Middle East fertilizer and ammonia producers able to arbitrage regional shortages. Losers include supply-chain intensive manufacturers in import-dependent Asian markets, airports and hub carriers facing demand loss plus higher jet fuel bills, and commodity-sensitive refiners or chemical plants whose feedstock availability becomes intermittent.

Key catalysts and time horizons: insurance and freight rate repricing can tighten within days-weeks; physical storage saturation and reroute-led supply shortfalls crystallize over 1–3 months; fiscal/defense procurement responses and capex reallocation in the Gulf play out over 6–24 months. A credible diplomatic de-escalation or rapid military reopening of shipping lanes would be the dominant reversal; conversely, spillover attacks on alternate chokepoints (Red Sea, Bab el-Mandeb) or a colder-than-normal winter would materially extend the shock and the premium embedded across markets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.70