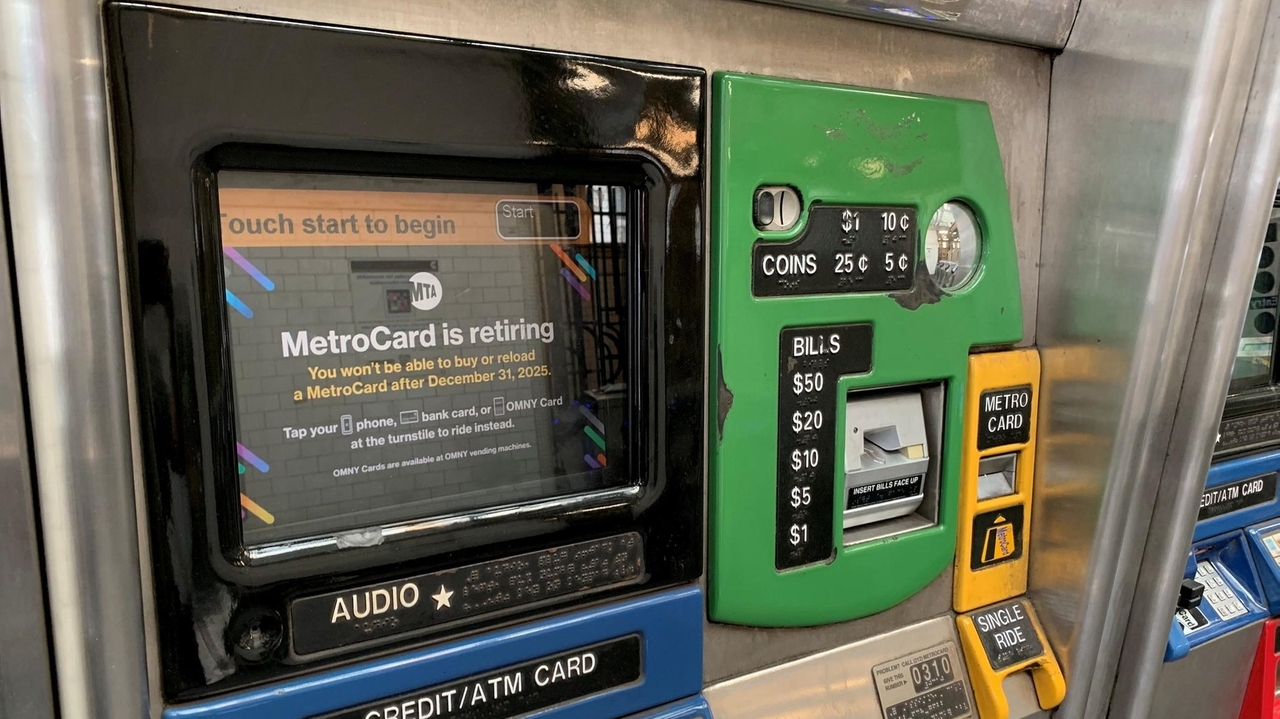

The MTA is phasing out the MetroCard as New York City switches to the OMNY contactless fare system, with Dec. 31 the last day to buy or refill MetroCards and current cards accepted until a later final acceptance date. More than 90% of rides already use contactless payments; the MTA estimates the conversion will save at least $20 million annually. OMNY requires tapping a phone, contactless card, or a physical OMNY card (sold at select retailers) and implements a weekly fare cap (free rides after 12 rides or $35 within seven days if using the same payment method). The shift increases contactless payment adoption (implicating card networks and payment processors), reduces cash handling, and centralizes trip/account data (with attendant privacy considerations).

Market structure: The shift to OMNY accelerates secular contactless volume (MTA: >90% today) and converts a legacy cash/card issuance cost ($20M/year saving for MTA) into recurring electronic transactions that favor device makers (AAPL), card networks (V/MA) and retail distributors (CVS/Walgreens). The 7‑day cap (12 rides or $35) and same‑device requirement increase wallet stickiness and marginless incremental transaction volume for networks; expect low single‑digit EPS tailwinds for large networks over 12–36 months from incremental TPV. Risk assessment: Primary tail risks are a major OMNY outage or cyberattack (single event >12 hours could force temporary fare freezes and regulatory scrutiny) and higher fraud/chargeback trends that compress issuer economics by mid‑single-digit basis points. Time horizons: immediate (days) for operational glitches, short (1–6 months) for adoption/merchant foot traffic signals, long (12–36 months) for measurable revenue migration to wallets; hidden dependency: the weekly cap requires consistent device/card use — fragmentation among multiple cards blunts capture. Trade implications: Favor AAPL and payment networks — allocate conviction size to AAPL (1–2% overweight) and split 1–2% between V and MA to capture TPV growth over 6–18 months; small tactical buy of CVS (0.5%) for incremental retail distribution of OMNY cards. Use options to leverize timing: buy AAPL 6‑month call spreads (5–10% OTM) sized to risk 0.5% of portfolio; consider V 6‑9 month 10% OTM calls for optionality if weekly volume metrics accelerate. Contrarian angles: Markets underprice regulatory/privacy backlash risk (data monetization/regulatory limits could cap network upside) and may overestimate MTA savings vis‑à‑vis pension/liability pressures — muni credit impact is negligible unless savings scale above low‑double‑digit millions. Historical parallel: London’s contactless rollout increased network volumes but also produced intermittent fraud spikes; monitor fraud metrics and OMNY outage frequency as triggers to reduce exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment