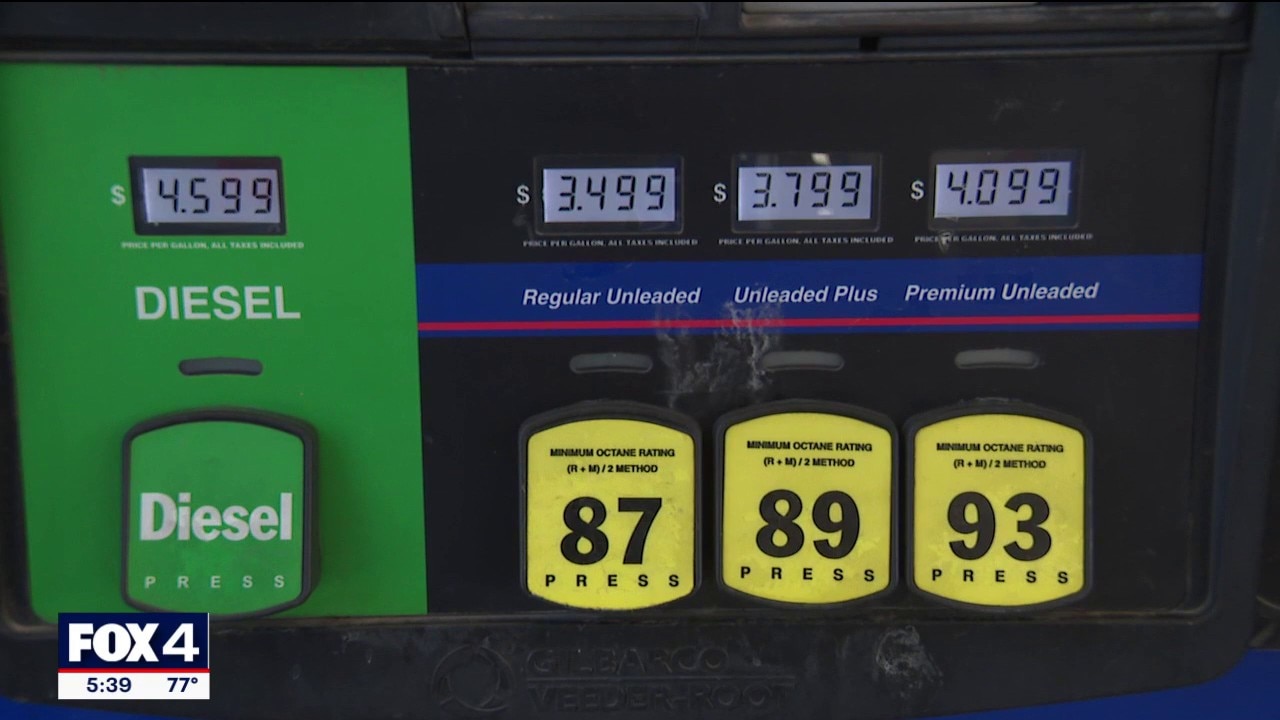

Oil prices have risen to over $100/barrel as Iran exerts pressure on the Strait of Hormuz; U.S. average gasoline is $3.63/gal (up ~$0.60 since Feb 28) and Texas is $3.28/gal (up $0.20 w/w, ~+$0.60 y/y). U.S. Energy Secretary says the Navy is not yet ready to escort tankers, raising supply-disruption risk. Higher oil/diesel costs threaten input-price inflation across farming (tractors, fertilizer), plastics, construction materials and transport, implying broader upward pressure on consumer and export prices.

Energy producers with low lifting costs and flexible capital programs are set to capture outsized cash flow in the near term, while high-cost producers and end-users absorb input-driven margin compression. Expect midstream tollers and storage owners to benefit from volatility and seasonally higher shipping premia; conversely, diesel-intensive sectors (trucking, bulk ag logistics, regional airlines) will see margins compress before any retail price passthrough completes.

Second-order inflation transmission will show up in industrial inputs and food CPI with a lag: fertilizer and petrochemical chains reprice on energy-led input moves, and packers/food processors face feedstock jumps that are hard to hedge fully for more than a quarter. This feedthrough increases the probability of renewed consumer discretionary weakness and forces faster inventory re-pricing for importers, tightening margins into Q2/Q3.

Key catalysts to watch are rapid supply-side fixes (rebuilt shipping corridors, tactical production increases, or strategic stock releases) that can normalize spreads in weeks, versus structural responses (higher capex for US shale, alternative shipping routes) that play out over months to years. Tail risks include escalation that forces multi-month chokepoint closures or broad sanctions that shift trade flows permanently, which would re-rate assets differently across the curve.

A tactical tilting is warranted: favor liquid, short-dated exposure to energy upside while hedging for a political de-escalation snapback. Size positions to reflect asymmetric timing risk—near-term volatility is high but mean reversion is possible if diplomacy or supply responses materialize within 30-90 days.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.55