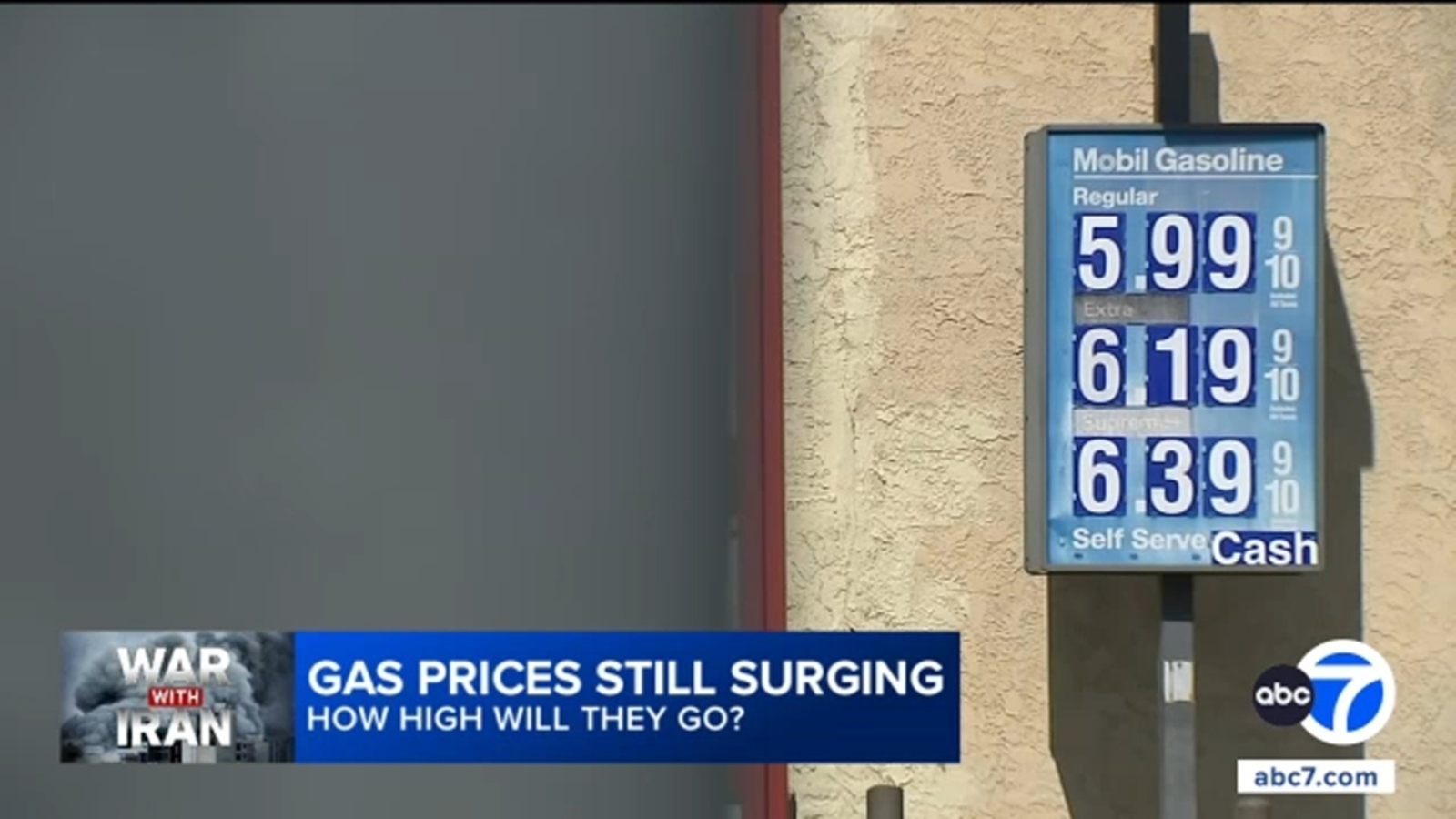

Markets moved sharply lower as the war with Iran entered week two: the Dow fell ~720 points while the S&P 500 and Nasdaq slipped about 1.3% and 1.2%, respectively, amid oil trading near $120/barrel. Gasoline averages jumped to $3.47 nationwide (from $2.99 a week ago) and $5.15 in Southern California (up >$0.53), with some pump prices exceeding $8; the Strait of Hormuz has been closed and producers are curtailing output, raising risks for transportation costs, airlines and broader inflationary pressure.

Shock to marine chokepoints and rapid fuel-price repricing is acting like a negative shock to discretionary real incomes with a short latency: expect measurable demand destruction in travel, restaurants, and non-essential retail within 4–12 weeks as consumers reallocate wallet share to transport and food-at-home. That transfer compresses margins for thinly‑hedged service firms while simultaneously fattening near-term cash flow for commodity owners and refiners; the asymmetry is that producers capture incremental margin immediately, whereas consumer-facing businesses see a lagged revenue hit and then a plasticity-driven volume decline.

Logistics and transport will bifurcate — asset owners with contractual fuel surcharges or long-term shipping charters (major container lines, integrated parcel carriers) can pass costs; spot-exposed trucking, LTL, and independent rideshare fleets cannot. Shipping reroutes around the Cape add 10–20% transit time and push time‑charter and bunker demand; expect a 20–40% run-up in short-term dry bulk/OK/TC indices if the Strait closure persists beyond 30 days, which in turn feeds higher input costs for manufacturers with just-in-time inventories.

Key catalysts: short-term escalation (days–weeks) increases a risk premium that will show up as higher oil volatility and wider refining cracks; a coordinated SPR release or credible diplomatic de‑escalation can erase much of the premium within 30–90 days. Contrarian point: the market currently prices a prolonged supply blackout, but U.S. shale can incrementally respond within 3–6 months—so trades longer than that should price in slower normalization rather than permanent structural loss of supply.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately negative

Sentiment Score

-0.65

Ticker Sentiment